There are many ways to invest successfully. Public stocks, bonds, private equity, real estate, venture capital, etc. And within each category, there are so many different investment opportunities.

In public stocks, there are something like 5,000 listed stocks in the US. In venture capital, there were something like 30,000 companies that raised venture capital in 2019.

How do you make sense out of all of that opportunity?

I’ve always been a fan of knowing what you are looking for and ignoring everything else. We call that thesis based investing at USV, but it is actually more than that.

We can say that we are looking to back trusted brands that increase access to capital, wellness, and knowledge, and we do. But we do more than that. In each of those sectors, we go deeper and identify specific areas within them that we want to target. We call those “deep dives.” We identify areas we want to focus on and areas we don’t want to focus on.

All of this is a relentless effort to figure out what we are looking for and then go out and find it. It is not a static thing. It is a dynamic thing. A pandemic comes along and rocks our world. Time to revisit the thesis and the deep dives. When the pandemic ends, and it will, we will factor that into our thinking too.

In a world with so much opportunity, it pays to ignore the vast majority of it and focus on a tiny bit of it. That may seem counterintuitive, but I am certain that it is the right thing to do.

Yesterday morning we got the news that Pfizer’s mRNA Covid vaccine developed in partnership with BioNTech saw 90% efficacy in phase three clinical trials. While this is terrific news, Wall Street saw it as bad news for companies that are doing well during this pandemic (Zoom, Peloton, e-commerce, etc).

This is a chart of Jim Cramer’s Covid 100 index:

Wall Street believes the end of the Covid pandemic is in sight and is rotating out of this group. I see that as terrific news, even though I am a large holder of a name or two in that index.

I cannot wait until I can start meeting entrepreneurs again in person. I cannot wait until USV can meet together in person. I cannot wait until I can see live music, movies, theater, etc, etc. These things cannot come soon enough for me.

But I also wonder how many of the habits we acquired during this pandemic (which is NOT over yet), will stick when we can go back to doing all of these things we long to do.

Here are some questions to ponder:

1/ Will our use of Zoom to meet decline materially when the pandemic is over?

2/ Will we get back on planes and resume our business travel like we did before the pandemic?

3/ Will we go back to the spin studio even though we learned to love a spin class on our Peloton?

4/ Will we rush back to stores and abandon our e-commerce habits?

5/ Will we all go back to the office five days a week?

I think the answer is yes to a degree, but almost certainly not totally. We have created new habits in this awful year and they are not going to go away so quickly, or ever.

I don’t know if that means the Covid 100 index is a buying opportunity or it needs to go down some more. I will leave that to Jim Cramer.

I do know that the way we work and live and entertain ourselves has changed materially and forever in this pandemic and things won’t be exactly the same when it is over.

There was a good Twitter discussion of this issue over the weekend between some folks who work in the VC sector. I think it is worth sharing more broadly.

As many of you know, Special Purpose Acquisition Companies (SPACs) are all the rage on wall street right now. SPACs are publicly traded “shell companies” that raise capital in an IPO process and then use that capital to merge with a privately held business.

SPACs have been around for at least thirty years and I have always thought of them as a “liquidity path of last resort” for our portfolio companies. The thinking was that if you could not go public in a traditional IPO, and if you could not find a traditional M&A buyer, then you would consider a SPAC.

But my thinking on SPACs has changed in this latest SPAC frenzy. I now see them as part of the continued “assault” on the traditional IPO process and largely a good thing.

For most of my career as a VC, the IPO has been the holy grail. Our very best portfolio companies would be offered an opportunity to go public by the top investment banks on wall street. And I have been involved in several dozen IPOs in my career.

The terms of an IPO are fairly locked down and are largely a great business for the top wall street banks and their buy side clients. I don’t take as much offense to this situation as others in the VC business have. I have viewed it as a mutually beneficial relationship between the top banks, VC firms, and the founders and CEOs who lead our portfolio companies.

However, in the last few years, competition has emerged for IPOs. On the left has come direct listings. And on the right, we have SPACs. Now founders and CEOs and Boards have a plethora of options for moving from a privately held business to a publicly held business.

Competition and choice is good. That is deeply held belief of mine across all aspects of life and business. And so the deluge of SPAC money coming to market right now is a good thing for the founders and CEOs who lead our portfolio companies. It offers them a wider array of options for going public than they had before. I am certain that will be a good thing for the tech sector and the VC sector.

All of that said, I do think SPACs have positives and negatives relative to IPOs and Direct Listings. What is right for your company will depend on the circumstances you find yourself in, including whether or not you need to raise primary capital, whether or not you need a lot of secondary liquidity, whether or not your “story” will be exciting to public market investors right out of the gate, how quickly you need to transact, and a host of other factors.

It is also the case that a number of VC firms and growth investors are raising their own SPACs. That too reflects the changing dynamics of the investment business and how fund managers like USV access capital and deploy it. I have always been a traditionalist when it comes to raising capital and deploying it. I like the small VC firm model, a close and long standing relationship with our investors (called LPs), and the rhythm of raising funds and sending the money back again and again. But I appreciate that others don’t see things that way and they may be on to something important with the VC SPAC model. We will see. I like that people are experimenting with the model. It will be revealing to all of us in time.

I wrote a blog post in September of last year arguing that gross margins and operating margins really matter when valuing companies. I argued that “software companies with software margins” are better businesses than tech companies that are not really software companies but a tech-enabled version of some other business.

But gross margins, in particular, can be tricky to compare. In some cases, a software business is in the middle of the revenue flow, takes the revenue, and then passes on a lot of it, and is left with what looks like a low margin, but is in fact a high margin.

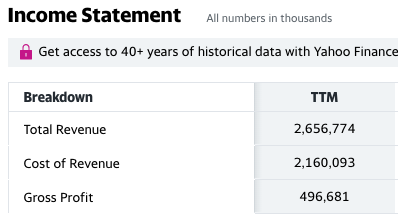

So Adyen operated in the last twelve months with an 18.7% gross margin. Many would think that was a “very low margin business.” But the truth is Adyen is simply passing through that $2.1bn of revenue to financial institutions in the form of interchange and other fees. They do very little with that money.

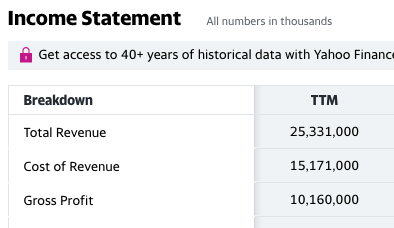

So Macy’s operated at a 40.1% gross margin over the last twelve months, more than double what Adyen operated at.

That $15bn cost of revenue on Macy’s Income Statement is the cost of purchasing everything you might find in a Macy’s store, the inventory costs associated with that, and the cost and effort of displaying all of that inventory in the stores.

So while it is the case that Macy’s has more than double the gross margin of Adyen, I believe Adyen has a much more attractive business from a margin perspective than Macy’s.

That is because Macy’s expends enormous amounts of working capital and operating expense and effort in its $15bn cost of revenue where Adyen expends very little working capital and operating expense and effort in its $2.1bn cost of revenue.

The trick, I think, is to wrap your head around the cost of revenue or cost of goods sold line item in the income statement and think about what is going on there. If it is very little to no effort, and largely just an accounting entry, then you may have a “low margin business” that is actually a high margin business. On the other hand, if it is a lot of work and capital investment to produce those margins, well then you have what you have and that is often a low margin business.

When bad news hits, I have seen traders sell quickly, get to cash, and then take some time to evaluate the situation before acting on the news. That is true of a company missing its quarter, a sudden management change, and many other forms of bad news. It is also the case when macro events hit the market.

So when a macro event hits the markets, all assets get sold in a “risk off” trade to increase liquidity and buy some time to figure out what is going on.

But soon enough, the market starts to sort through winners and losers. That’s when things stop correlating.

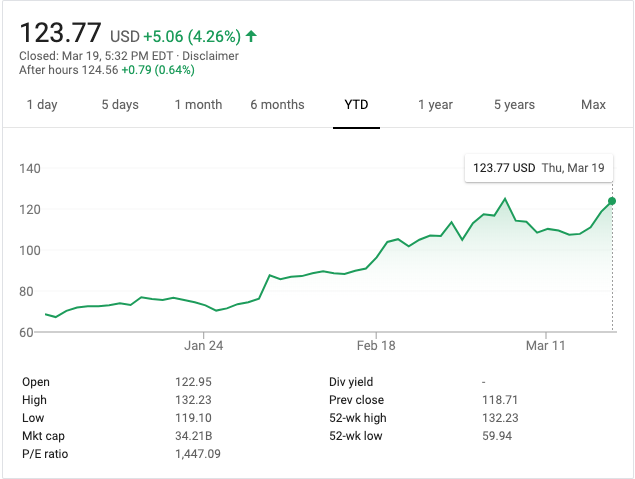

The obvious example is Zoom which is clearly a major beneficiary of this macro event we are in the middle of.

Zoom sold off with the market over the last week and a half but has rebounded nicely and year to date is up something like 75%.

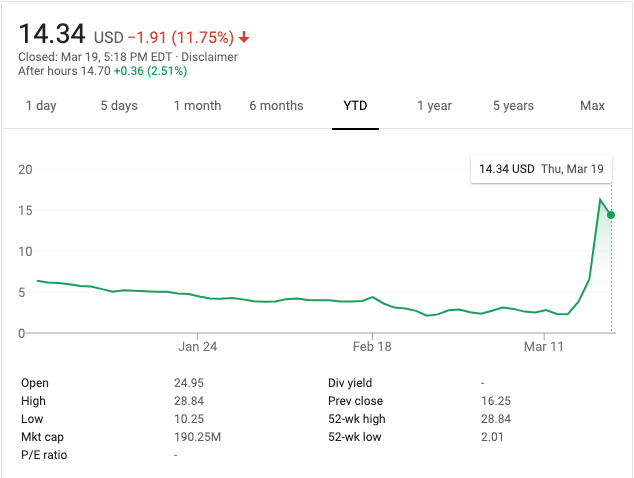

Blue Apron, which the market had left for dead, is another example of a business that will likely do well in this macro environment, or at least it seems that the market thinks so.

Contrast that chart with Bookings, one of the largest (the largest?) online travel businesses, and you can see the lack of correlation.

I believe this downturn will see a greater number of winners and losers than most of the downturns I have lived through. That is because we are already into a pretty meaningful transition from an industrial/physical economy to a knowledge/digital economy and the very nature of this macro event is accelerating that transition in many ways. We just won’t go back to doing some things the same way.

I do plan to go out to my favorite restaurants as soon as I can. But I also plan to fly even less for business when this thing is over. Some things will return to normal. Others won’t.

And that is what the market will sort out over the course of this downturn and is already busy sorting out.

Which takes me, naturally, to crypto. Crypto, to true believers like me, was supposed to be a place to go for safety. We can trust crypto when we can’t trust banks or governments, right?

Wrong.

Bitcoin crashed harder than anything in the first few days of the market selloff. It was down 60% over five days from March 7th to March 12th. But since then it has recovered nicely and is now only down about 30%.

Howard’s guest was right. In panics, all assets are correlated because the market needs to deleverage. Margin loans get called. Leveraged bets go bad. Weak hands fold. And in crypto that happened faster and more furiously than any other asset class. That’s because the market infrastructure is less mature, there are places (largely outside of the US) where you could (and maybe still can) get 100x leverage on a crypto trade, and because these markets are not as liquid and other markets.

But now that the deleveraging has happened, we can look at what crypto has to offer.

Bitcoin is “hard money.” There is a fixed supply of it. 21mm bitcoins to be exact, some of which are gone and are never coming back.

Contrast that to what the central banks are doing right now. The printing presses are melting down there is so much money being printed to stabilize the global economy.

So if you want to hedge your portfolio from that risk, where can you go? Actually a few places. But one of them is Bitcoin. And I suspect that will be where some smart money will go over the next few months, quarters, etc.

But that’s not all that crypto has to offer. The entire decentralized finance stack (fintech 2.0) is being built on Ethereum. And we are seeing decentralized bandwidth, storage, and other critical infrastructure being developed in a number of new protocols.

I’m not going to write an entire crypto thesis here. But my point is that crypto won’t be correlated with the overall market for long. It’s doesn’t even appear to be a week in.

The post I wrote yesterday generated a lot of discussion. I followed it on Twitter and engaged with much of it there.

One of the best things about writing is all of the feedback you get. It helps to sharpen your arguments and also makes you rethink them too.

Here are some of the takeaways:

Some readers interpreted the post as arguing for only investing in high gross margin businesses. I don’t believe that is the right takeaway. The better takeaway is that high margin businesses are often less dependent on capital markets because they can internally generate cash more easily. That is not the case with low margin businesses. So how you value and how you finance low margin businesses becomes very important. They can’t be valued too highly or you risk a financing crisis.

Bill Gurley tweeted his blog post from 2011 that “all revenue is not created equal.” That is a great way of saying what I was trying to say.

Apple and Amazon were put forth as great lower margin businesses. Amazon is a roughly 25% gross margin business and trades at a little over 3x revenues. Apple is a roughly 40% gross margin business and trades closer to 4x revenues. I think that emphasizes the point that revenue multiples ought to reflect gross margins.

Many people argued that operating margins and growth rates should be the two numbers that matter most in valuing a business. I totally agree. But it is hard to have 40% operating margins if you have 40% gross margins. The truth is that operating margins will be highly dependent on gross margins. But there will be edge cases where that is less true.

I got a lot of people saying “isn’t this totally obvious?”. To which I say “it should be but clearly it is not.”

The most important takeaway for me is that the public markets are showing us in tech/startup/VC land that the economic fundamentals of a business, even those that are driving massive disruption in their markets, really does matter and that we need to pay attention to them when we finance these companies.

Public market investors have become less willing to leave their comfort zones, and it’s manifesting most obviously in the IPO market. Novel disruption has fallen out of favor, with many preferring more time-tested models like enterprise SaaS and biotech. Peloton yesterday raised over $1.1 billion in its IPO, pricing at the top of its $26-$29 range, but its shares then got crushed (although still valued well above the last private mark). Its CEO talked to Axios yesterday about the falling stock price. Endeavor, the live events and artist representation firm led by Ari Emanuel, last night canceled an IPO that originally was to raise over $600 million, before it was later downsized. WeWork… well, you know the story there. Yes, all three companies have dual-class shares. Yes, all three were highly valued by venture capital or private equity investors. Yes, all three were unprofitable for the first half of 2019. Those characteristics are also true of Datadog and Ping Identity, both of which had successful IPOs this month and continue to trade above offering. The trio’s real similarity was that each had a very complicated story. Peloton is a high-end hardware and SaaS business that produces original media content, sells apparel, and runs its own delivery logistics. Endeavor began life representing movie stars and Donald Trump, but later expanded into a massive live events business that includes the UFC and Professional Bull Riders. Plus, it’s got a streaming platform. WeWork… again, it’s different. All of this comes against the backdrop of Uber, which also had a very complicated story and an IPO that emboldened short-sellers. Up next: A lot of biotech startup IPOs, but no high-growth, complicated tech unicorns. “We’re about to get a bit of a break from those sorts of deals, which I think is good for everyone,” a top Wall Street banker told me this morning. Private markets follow public markets, so don’t be surprised to see some valuation and/or deal size pullback for these “hard to comp” companies. Particularly if SoftBank fails to raise Vision Fund 2. Goodbye to egregious governance terms. Dual-class will survive, but WeWork laid a third rail for others to avoid. U.S. IPOs have still outperformed the S&P 500 in 2019, although the gap has shrunk significantly this month. Or, put another way: The sky isn’t falling, but it’s gotten a lot darker. And, for some, downright stormy.

While all of this is true, I think it is a lot simpler than that.

The public markets are a lot different than the private markets.

Financial transactions in the private markets are controlled by the issuers, happen when the issuers want them to happen, and are generally auctions, particularly in the late stage markets.

Public market investors can buy and sell stocks every day based on what is attractive to them and what is not. If they feel like they missed out on something, they can get into it immediately.

For this reason, valuations in the private markets, particularly the late-stage private markets, can sometimes be irrational. Public market valuations, certainly after a stock has traded for a material amount of time and lockups have come off, are much more rational.

For the last five or six years, I have been writing here that I very much want to see the wave of highly valued and highly heralded companies that were started in the last decade come public. I have wanted to see how these companies trade because it will help us in the private markets better understand how to finance and value businesses.

And now we are seeing that.

And what we are seeing, for the most part, is that margins matter. Both gross margins and operating margins.

If you look at the class of companies that have come public in the last twelve months, many of the stocks that have performed the best are software companies with software margins. One notable exception to that is Beyond Meat.

Zoom – 81% gross margin

Cloudflare (a USV portfolio company) – 77% gross margin

Datadog – 75% gross margin

If you look at the same list, many of the stocks that have struggled are companies that have low gross margins.

Uber – 46% gross margin

Lyft – 39% gross margin

Peloton – 42% gross margin

Some other notable numbers:

WeWork gross margins – 20%

Spotify (down almost 30% in the last two months) gross margins – 26%

I believe that we have seen a narrative in the late stage private markets that as software is eating the world (real estate, music, exercise, transportation), every company should be valued as a software company at 10x revenues or more.

And that narrative is now falling apart.

If the product is software and thus can produce software gross margins (75% or greater), then it should be valued as a software company.

If the product is something else and cannot produce software gross margins then it needs to be valued like other similar businesses with similar margins, but maybe at some premium to recognize the leverage it can get through software.

But we have not been doing it that way in the late-stage private markets for the last five years.

I think we may start now that the public markets are showing us how.

I am continuing my mini series on reading S1s (IPO documents). We are enjoying an IPO bonanza this year, so we might as well use it for some good and learn something.

When a company files for an IPO, I like to think if there is a publicly traded company that looks a lot like that company and if so, I lik to run some numbers comparing the two.

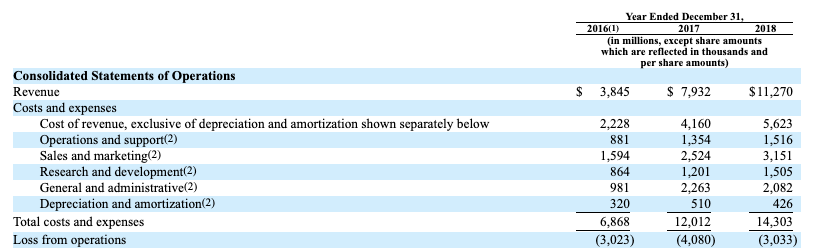

Well we have that exact situation with Uber filing to go public last week. Here is Uber’s S1.

Here are Uber’s profit and loss numbers from their S1:

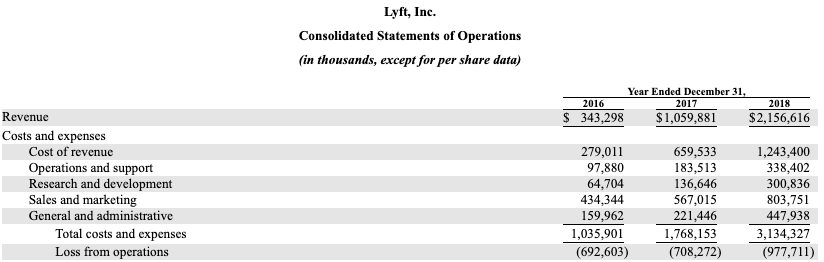

We can compare this to Lyft’s profit and loss from my prior blog post:

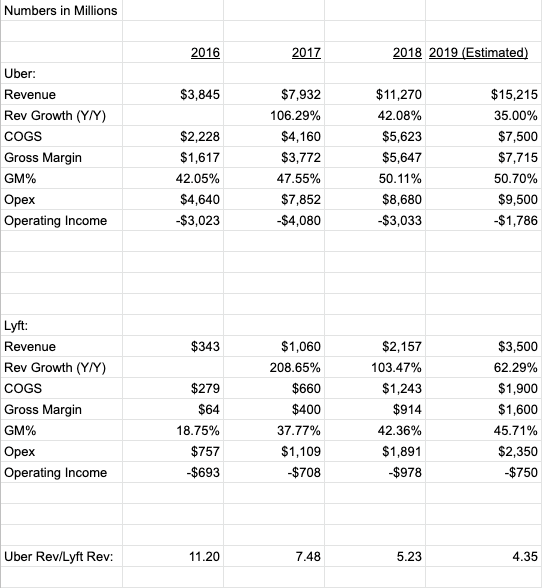

I put all of these numbers into a spreadsheet and added some estimates for 2019 that are nothing more than back of envelope guesstimates.

What you can see from this is that Uber is 4-5x larger than Lyft, growing a lot more slowly, has slightly better gross margins, and both are still losing a lot of money but both are moving towards getting profitable on operations in a few years.

Finally lets look at market valuations. Lyft is currently trading at a market cap of $17bn. If you say that Uber is 4-5x larger than Lyft, then Uber ought to be worth in the range of $70bn to $85bn.

There are other factors that will be in play when Uber eventually prices their IPO and trades. Uber owns minority interests in a number of other ridesharing businesses that could be worth as much as $10bn of additional value. On the other hand, Lyft is growing more quickly than Uber.

Ultimately we will see how the market values Uber. But from this analysis, and the public market comparables from Lyft, we can see that Uber should be worth quite a bit when it goes public.