The Power Of Passed Links (continued)

Ben Straley left the comment that inspired my initial post on this topic. And last night, he left another comment that is a blog post in its own right. So here it is in its entirety. I hope you find it as useful as I do.

The following are a few more data points and comments I want to add to the discussion:

1. Recap of a Hitwise study published on DMNews – Visits from Facebook are greater than visits from Google on a few major sites across several verticals. Are sharing and “social discovery” more important sources of traffic than search in certain verticals? Is this a harbinger of things to come across a larger swath of Web sites?

2. The average % of traffic from passed links varies considerably by vertical. We suspect some of this is due to the demographics of the audience on a given site. Also, the content found in some verticals is just much more likely to get passed along than in others. For example, we see % of traffic from shared links on games sites well into the 25-40% range. Sites/campaigns that promote strong offers also receive a significant % of their traffic from shared links – in the 20-30% range. In contrast, B2B sites with more static content receive a far lesser benefit from shared links – somewhere in the 3-7% range.

3. This is closely related to point 2 above. Content matters most of all. If you’ve got good content and make it easy for people to link to it, it will be shared and attract a lot of visitors. We’ve seen this work over and over. We tracked the pass-along of links pointing to two campaigns running concurrently for the same product (different micro-sites). One of them had a good offer but so-so content while the other campaign had great (funny) content with no offer. The % of unique visitors generated by the pass-along of links to the good offer was under 10% while the traffic from the pass-along of the links to the good content was over 40%. The campaign with good content also got significantly more traffic overall. What data like this suggests is that the prediction you make in your deck about dollars shifting from media to content is a really good one in my opinion. As marketers compete for the attention and interest of their audience, the best way to do this is through content that’s delivered to them via their social graph. This already happens if the content’s good. There just isn’t enough of it.

4. We haven’t looked at this yet but I’m extremely curious to know what ,if any, correlation there is between the number (or %) of visitors from passed links and the number (or %) of visitors from organic search 30-60 days later or however long it takes for the search bots to update their indices. It stands to reason there’s a positive correlation between the two metrics but we haven’t done the number crunching yet. Could traffic from shared links be an early indicator of improved SEO performance given the proliferation of back links?

5. The strawman you’ve built above is a good stab at an analytical framework for estimating the absolute value of shared links. I think it makes sense to take it a few steps further. If I’m an online marketer paying an eCPM/eCPC/eCPA for some % of traffic to my site and conversions (if I’m doing direct response), then I’m probably also encouraging people to pass-along links via Twitter, Facebook, Digg, etc. While the reach of the latter set of activities is no doubt lower than what I can reasonably expect to obtain from a paid media campaign, I should also expect that the eCPC/eCPA for shared links is much, much lower due to consistently higher click-through and conversion rates for these links. So, as I think about how to optimize the performance of my campaign, I need to be thinking about how I should be shifting dollars within as well as across these very different but complementary sets of activities. Also, my paid media can stimulate pass-along which should be factored into my calculations of the true ROI of my advertising campaign. We’re still pulling the data on this which I’ll share as soon as we have it.

6. In most cases where traffic and conversions from shared links are high, we see a HUGE amount of activity driven initially by vertically-oriented blogs and community forums before it goes “mass social” by making its way up to Facebook for example. In calculating true value of shared links, it’s important to factor in the niche sites and communities in your vertical. The numbers might be relatively small but their significance huge. In one case, we saw a niche site send several hundred visitors to a marketer’s campaign micro-site in a 2-week period. This placed that referring site well down the list of top-referrers (something like #25). Not very interesting. But using our sharing tracking and measurement technology, our customer watched as the visitors from that niche site drove well over fourteen thousand additional visitors to the campaign micro-site via links shared in email, IM, on blogs, forums, and, of course, Facebook etc. Niche sites matter.

7. Meteor Solutions hasn’t been in business long enough to have longitudinal data to do trend analysis yet. However, we do see sites/campaigns that cater to a younger audience receive a higher percentage of their traffic from shared links. (See my comment about games sites above) When I take a step back and look at my own behavior, I also have a hard time denying the fact that my media consumption habits and behaviors have changed in the last 18-24 months. I’m getting more and more of my information from the people I’m connected to through email, IM, RSS, Facebook, and Twitter. Also, the nature of the searching I’m doing now is much more targeted and specific. I won’t search as much for content or something that’s happening now because I’ve probably already received the link from someone I know or follow. The links that are relevant to me and timely find their way to me these days with remarkable efficiency.

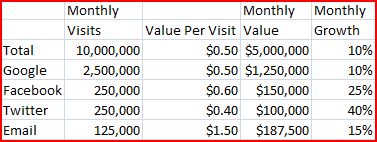

8. The most popular mode of sharing we see is email (25% of visits from passed links come from links shared through email), followed by blogs (18% of visits from passed links come from links shared through blogs), video sharing sites (14% of visits from passed links come from links shared through video sharing sites like YouTube), and forums/message boards (11% of visits from passed links come from links shared through forums and message boards). Social networks account for around 9% of the traffic from shared links. I pulled these stats from our Meteor Tracker data which does not yet contain a representative sample of sites of varying sizes across all verticals. It isn’t yet representative of the Web as a whole

![Reblog this post [with Zemanta]](http://img.zemanta.com/reblog_b.png?x-id=100f6286-13de-4a17-bb56-579d1c93b8c8)

![Reblog this post [with Zemanta]](http://img.zemanta.com/reblog_b.png?x-id=0b607c11-381a-46b2-a140-129837e5ac8c)

![Reblog this post [with Zemanta]](http://img.zemanta.com/reblog_b.png?x-id=e0ee65b1-05f7-45e6-8137-89059e50e8fc)

![Reblog this post [with Zemanta]](http://img.zemanta.com/reblog_b.png?x-id=7d516714-87ae-44fc-9006-67cdb5de7135)

![Reblog this post [with Zemanta]](http://img.zemanta.com/reblog_b.png?x-id=1f719446-8a5f-428d-ab04-bf66aad04b72)

![Reblog this post [with Zemanta]](http://img.zemanta.com/reblog_b.png?x-id=9abdb776-6555-4c11-84af-89dedc4d05f7)

![Reblog this post [with Zemanta]](http://img.zemanta.com/reblog_b.png?x-id=5e1508d1-0494-479a-adab-5d450779dffe)

![Reblog this post [with Zemanta]](http://img.zemanta.com/reblog_b.png?x-id=9b258ae9-56b6-45c5-aeb2-9998ae545b3d)

![Reblog this post [with Zemanta]](http://img.zemanta.com/reblog_b.png?x-id=a87bb1dc-11a3-4071-abcf-49922e0f8d39)