The 0.00% Yield

The Gotham Gal and I don't normally keep much cash in the bank. We like a portfolio of tax free municipal bonds for our cash that is not invested in venture deals, private companies, real estate, and the like.

But recently we closed a few transactions that resulted in some cash being wired into our bank account. I emailed the banker and asked him to move the cash to the brokerage account connected to our checking account and into a tax free money market.

A few days later I was thinking about whether to keep the cash in the tax free money market account or move it to our tax free bond portfolio. So I emailed the banker again and asked what the yield was in the tax free money market account. The answer I got surprised me:

Unfortunately, both the Tax-Free Money Market Sweep and Federal Money Market Fund in your brokerage account are currently yielding 0.00%.

Yup, that is right. 0.00%.

Needless to say the cash won't stay at the bank much longer.

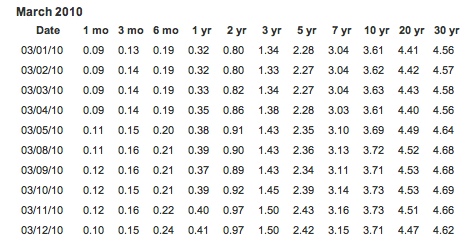

But I didn't leave it at that. I did some digging around. I looked at treasuries. Here are the current treasury yields:

You can see why a federal money market fund yields 0.00%. The treasuries the fund likely owns are yielding 10 to 25 basis points. And I guess that yield is totally gone after their fees are applied.

I've got emails out to a few other banks we do business with to find out what their money markets are paying. I'm curious if the 0.00% money market yield is standard across the market right now.

Regardless of whether or not my bank or any bank is taking advantage of its customers (and I am not sure they are), this zero interest rate environment is worth thinking about.

I was at dinner last night with friends and we got to talking about the stock market. Our friend asked me why I thought the market was doing so well (the S&P 500 is up 65% in the past year, from its post meltdown low). I told him in an environment where cash in the bank yields 0.00% two things happen. First, people chase yields elsewhere and the US stock market has been a big beneficiary of that. Second, you can borrow money at very low cost (not 0.00% though) and put it into the market.

That's why this "hyper low" rate environment is dangerous. Because it won't last and when rates start to go up, the market will stall or even decline. Many of the places people have gone to chase yields will not be great places to be.

So what to do when your bank is paying you 0.00%? Well as I said at the start of this post, we like a portfolio of highly rated (AA and AAA) municipal bonds. In this low rate environment, I like the stub end of a long term muni bond that has a year or two left on it. You pay a premium to its face value to buy it and when it pays off, you will get less than you paid for it. But in the interim you'll get a decent tax free yield and all in, including the loss on the purchase price, over the one or two year hold period you can get 2% to 2.5% tax free. I don't recommend trying to buy these bonds yourself. Find a good manager who has been doing it for years to do this for you.

And then wait for rates to rise. Because I am certain they will. And don't jump in quickly when they do. Because when rates rise, they tend to do that for a while. And of course, the money markets will start to pay interest again.

The take away from this post is that rates are at historical lows. You can't really go below 0.00% without having to pay someone to take your cash from you. It's a dangerous time. Don't chase yields. Find an acceptable place to put your money for a year or two at a low, but positive, yield. And then wait for rates to rise. Because they will and you don't want to be in the wrong place when that happens.

Comments (Archived):

You’re finally cottoning on to this? This has been an issue since late 2007.

i didn’t say it was a new issue. but it is a new issue for me personally. and it got me thinking about the ramifications of it.

Great advice, Fred. Thanks for sharing.*This is why following good, smart bloggers is great: you never know what you’re going to get.

I agree Reece. I don’t follow along because I am likely to need a VC or because I am part of that community per se. I follow because I learn about new technologies, companies, ways to value things, etc … good blogs like this one are just interesting … especially when you never know what you may get.

seems to be the best “risk free” method right now if you know when you need liquidity is to buy a treasury bond ladder with maturities at the times you might need the money liquid.

Yes. But look at that yield curve. Anything less than a couple years is paying a pittance

rates are ~0% in nominal terms. in real terms, meaning after we adjust for price inflation, they are negative. negative real rates are often a prelude to a run on the underlying currency. one of many signs.gold is, of course, where it’s at. this has already been proven and continues to be proven even more. oil and silver too. commodities in general.remember the economic crisis is being engineered as part of the central banking conspiracy to create their version of the new world order (almost all forms of cosmology agree that we are coming to an end of several major cycles of time, which is an opportunity for great transformation, and is typically accompanied by various cataclysms. the criminals want to use this to create their totalitarian one world government, but really it is an opportunity to create a renaissance, characterized most notably by peace, and probably lots of trends that we internet people see, like virtual currencies and game play. regardless of whether you believe in all this stuff the central bankers/powers that be do, they are motivated almost entirely by eschatological reasons). all the fiat currencies of the world are going to collapse so that they can introduce their world government with world currency as the “solution.” the SDR, a composite currency managed by the IMF, has already been proposed as a solution. this is literally exactly what hte conspiracy factualists have been ranting about (not because we can see the future, but because we can read what is being admitted). alternatively if htey can push the carbon scam through carbon credits may be the basis for the world currency as well.this stuff is admitted, the powers that be literally write books about it. read tragedy and hope by carroll quigley, bill clinton’s mentor.the central banking conspiracy can only work if the people are willing to bet on fear and ignorance, as ultimately, their agenda requires cooperation of the people.choice is yours.p.s. thanks boss for this post, i mean talk about gift wrapping an opportunity for me to drop bad news…..i owe you one boss

Good point about real rates kidBut as you know I don’t like gold and other commodities. They don’t yield anything so they are worthless to me. Just because others value them doesn’t work for me. They are subject to speculative bubbles and how do you really know what gold is worth?Give me cash flow, a risk of getting it in the future, and I can value thatIf you are worried about the US and the dollar (and you should be), I prefer the debt of other countries and their companies. Australia is one such country I like a lot. I also like India and Brazil

ultimately it is all about purchasing power. measure hte value of almost anything in terms of gold, then measure it in terms of US dollars, and chart this for the past 10 years. anyway you slice it, if you had your money sitting in low yield dollar denominated debt, you lost purchasing power over the past ten years. if you had it in gold, you gained purchasing power.the debt problems are creeping up in australia too. all fiat currencies are exposed to the whims of politicians who manage them, which is why politicians love them so much. it’s also why most of the world lives in poverty.

That’s interesting, but as a couple recent crises make clear, 10 years is too short a span to be evaluating on. What’s that chart look like for 100 years?Also note that many people think gold bugs are crazy because people who use just one thing to explain everything are almost always crazy. High-growth economies are complicated and finicky; there are a lot of ways to wreck them besides printing money.

history is the ultimate argument for gold. all fiat currencies have historically ended in hyperinflation — all of them, invariably, not a single fiat currency has escaped. when the free market is left to its own recourse as to what to use as currency, gold has been the winner for the past 2,000 years, provided gold is accessible (in prison they use cigarettes). all recent currency crises — russia, east asia, south america, zimbabwe — have seen gold preserve its purchasing power. i would include links to support all this but disqus flags my posts with links, though if you research it you will find evidence to support what is presented in this comment.

What’s up with disqus flagging your posts with links? Have you pinged Daniel Ha?

i asked on twitter, but did not hear back….no worries, i assume they got a ton of issues….i may setup another disqus identity to try to circumvent

Hey 10 years is a long time compared to my life time. Admit that trends look different over various time spans but a ten year period is a significant life fraction.Agree about the one size fits all solution. We’re all trying to find and nourish that which we value most, with the precious time we have.

This is a perfectly reasonable and sound approach. PPP (purchasing power parity) is a financial concept that has been used for years to set, explore and discover “fair” currency exchange rates.Perhaps the most interesting applications of PPP are in the Chinese currency exchange rate analysis.PPP requires you to price the purchase of a fairly broad, but otherwise very simple basket of goods and services in each currency and then to simply compare the total cost.In this way, currencies — in particular currencies which are otherwise not convertible — can be made to be convertible and comparable in a fair manner.The conclusion when applied to the Chinese currency is that the Chinese are world — no make that universe — class currency manipulators.

I agree Fred. The US banks may be giving only 0% return, but you can easily make around 12% return in India today if you invest in many commercial properties. In addition you make on the appreciation of the property in few years by the time construction has finished. At that time you can decide to either rent and collect cash or reinvest in another development project to repeat the same process.. Given the growth the country is going through the long term demand for commercial real estate is very promising..

Fred, last year I put a large sum of cash assets in FXA, a CurrencyShares ETF for the Australian Dollar. The yield was above 3% at the time, and it was a decent inflation hedge against the dollar. Since then it’s up nearly 40%, which has been an positive side effect, one that I expected, but not at that magnitude. It’s hard to see where it’s going next, but most people are not predicting a huge recovery for the US dollar in the near term, so I am still holding.

Great point. There’s plenty of ways to fight inflation and foreign currencies in commodity producing countries is a great way. Others include TIPS, baskets of commodities (gold, oil, etc), shorting long-term treasuries (not for the beginner). We recently posted up Howard Marks (Oaktree Capital, really respected investor) recommended ways to play inflation and it’s all around good advice: http://www.marketfolly.com/…

Couple of points: – A lot of the big guys (Soros, Paulson, have been piling into gold). That sword cuts both ways once their inflows stop. – Silver is both precious and industrial. Gold only precious. So silver is better hedge IF economy also improves. – The best hedge against a weak dollar? The US stock market. 40% of S&P 500 revenues come from international (the highest percentage ever). This will only benefit from a weaker dollar (hence the inverse correlation this past year on the stock mkt and the weak dollar). – Example: here’s the Zimbabwe stock market during their hyperinflation escapade: http://poppypundit.files.wo…

Sources of yield in the US stock market: – MLPs with consistent cash flow regardless of economy. Examples: KMP (6.4% yield), EEP (7.6% yield). Many hedge funds hedge out the market risk on these by shorting SPY against them (or ES futures), capturing the yield. – Closed end funds for municipal bonds that trade at a discount to NAV. Example: TYW (10% discount to NAV, 7% yield). The key is to buy these when the discount to NAV is statistically significantly lower than the average discount. But you still get (more or less) the long-term risk-reward of muni bonds.

“MLPs with consistent cash flow regardless of economy. Examples: KMP (6.4% yield), EEP (7.6% yield). Many hedge funds hedge out the market risk on these by shorting SPY against them (or ES futures), capturing the yield.”That is an interesting strategy.

not a bad thing to look at BUT 1) there is a special tax treatment – consult your advisors 2) they are more equity-like than cash-like, and there is no such thing as a perfect hedge 3) they’re not small caps but not huge either and liquidity could be an issue in an adverse environment (ie post-Lehman, or if tax treatment changes). A valuable tool to have in your box, but for a small portion of your assets. (Never forget those auction-rate preferred folks who thought they were very clever and had a great high yielding liquid cash substitute)

MLPs do add some time to your tax prep, unfortunately. I don’t own any currently, but I owned two last year, so I’ll have to deal with them for taxes this year.Re hedging, a more precise way to hedge an MLP portfolio would be to buy puts on the MLPs themselves, if they have options traded on them. Permitting myself a relevant plug, Portfolio Armor shows investors the least expensive way to get the level of protection they want on their MLPs, their other stocks, or their ETFs.

the chart is a bit misleading, we need to see it relative to the devaluation in the zim dollar. a flight out of the dollar ultimately means a decline in all dollar-denominated assets in real terms, which means all dollar-denominated assets will fall in purchasing power. put another way, the stock market may rise, and perhaps sharply, but consumer goods will rise even more sharply, especially since the US imports everything and produces nothing (except war and debt).i do like silver a lot and agree it could do better than gold. there are also more and more stories of fools’ gold, i.e. gold plated ingots that are actually tungsten on the inside. oil and commodities are a good hedge against such concerns, although i’m not sure how legit they are.

Hey the US produces eccentrics like ourselves with amazing efficiency. No one else can compare. Eccentric folks are like cigarettes in prison, we should be the new currency 😉

“but consumer goods will rise even more sharply, especially since the US imports everything and produces nothing (except war and debt).”You know, I disagree with your interpretation of just about every fact you’ve mentioned in these comments. But at the very least you get some props for knowing facts. But this kind of demagoguery just hurts that. It’s unfortunate. It lowers your otherwise high level of debate.

instead of saying you disagree, why not explain why you disagree? perhaps you will convince me. i seek the truth.i look down upon a society that tolerates war and ostracizes those who make true efforts to establish peace, especially when it is as obvious as is the case with 9/11 truth. you may find my behavior to be unfortunate, but not as unfortunate as i find a world that worships at the altar of lies, theft, and war.

Well of course.. you losing some of your credibility here (IMO) does not compare to tragedies like war. But it’s still unfortunate.As for my disagreement.. Debating on the internet is just futile. I have enough stress in my life, reading commentary (like this blog and others) is my chance to sit back and “enjoy the morning paper.”No debate, just discussion for me.

of course. the truth is you can’t debate what i say. you’re just offended, because deep down, you know i’m right, and what i’m saying reminds you that you’re an ignorant citizen who is tolerant of the problem, and derelict in your duty as a citizen to be responsible for participating in solving the problem. that is exactly my intent: to remind you of your ignorance. because that’s the real problem.

Thanks for the shared link and conditions on hedging capital investments.

“The best hedge against a weak dollar? The US stock market. 40% of S&P 500 revenues come from international (the highest percentage ever). This will only benefit from a weaker dollar (hence the inverse correlation this past year on the stock mkt and the weak dollar).”I can see a lot of folks who have been on the sidelines getting hurt by following this advice now, a year into the huge, liquidity-fueled recovery rally.

ok… how many other people looked up the word ‘eschatological’?Thanks for that one Kid.

hahahaha….i thought about defining it in the comment but i got lazy…..let me correct that now: here is the merriam-webster definiation of eschatology –1 : a branch of theology concerned with the final events in the history of the world or of humankind2 : a belief concerning death, the end of the world, or the ultimate destiny of humankind; specifically : any of various Christian doctrines concerning the Second Coming, the resurrection of the dead, or the Last Judgmentjust to clarify i did not intend for my comment to be pro or anti any religion, i am simply stating a common kook perspective on the beliefs of central bankers/powers that be.

nice.Hey KM if disqus doesn’t fix your linking, start a new profile. Their comment silo can’t last (they may even write a new web standard, I’m a fan of disqus just not silos of data), an inter operable comment standard will fulfill our community needs. Speaking of which, time to suggest one on the open web foundation group… can login with openid (and connect comments to that id) + keep a local cookie to avoid relogging in.

*raises his hand*

KM gold is this comment!I wasn’t disappointed by the comment I expected, pro.

I don’t see the collaboration of bankers and other leveraged speculators as some great assemblage of formal conspirators. That view, IMnsHO, grants the whole messy process far too much credit for cohesive, intelligent, centralized planning.I’ll grant you there are some futile formal conspiracy efforts by the less aware elites. The smarter money crowd understands that the new accelerated media ecology environment offers them the chance to amplify their traditional divide and conquer methodology of mass economic propaganda. He who controls the language controls the debate.Organically accelerated, network based economies, empower endless possibilities for new social economic cooperation. They also accelerate that vast, unspoken, statistical, conspiracy of greed and corruption long practiced by armies of speculators and defectors. By the way, for me, speculators ≠ investor.Don’t get me wrong, I am not speaking here of some smug, superior, moral fiber that allows me to look down my nose at those cretinous speculators and defectors. We are all PINK(driven by the biological prime directive of survival, self interest and control), that is just a fact of life built into the wetware, it is the penny in the curency of human affairs. It is time we accepted responsibility over our own evolutionary biological constraints. As Dirty Harry put it, a species has to know it’s own limitations. We need to get on with constructing social structures that come to grips with the fact that PINK is our fundamental building block.That being the case, the challenge is implementing some clever social networking methodologies that effectively drilling down to enforce a distributive, organic, array of PINK checks and balances. The disservices of this approach is the need to keeping the BORG effect at bay. Walking the razors edge, we are the BORG, and we, and only we, will decide how to assimilate ourselves.The manufacture of such network embedded organic memes cannot be left to commercial chance or commercial elites it must be proactively bottom up, periphery in. I am OK with the manufacture of consent, we need some form of social consent and it needs to be manufactured, my only concern is who gets to be on the manufacturing team!

Study 9/11, tell me who you think is responsible, and then tell me whether you think there is some conspiracy or not. Sent via BlackBerry from T-Mobile

As I said in my post!I’ll grant you there are some futile formal conspiracy efforts by the less aware elites.Let me retract “futile” and replace it with “long term futile”Yes something really smells about 911.What it is I’m not exactly sure.(Buffalo Springfield)My wild guess – something to do with central bankers.

so if the powers that be can plan 9/11, and if 9/11 was a “success” in the sense that it got them the war and control they wanted, then that means they can basically plan the world, which includes the world economy.the answer to how some group can be so intelligent and capable is a bit mysterious. in all seriousness, i think we need to go off planet and study aliens, lol, so ridiculous, i know. but folks who do their research in full will know where i am coming from.

Did you see that all the cabs yesterday for an hour or two weren’t taking credit cards? Their network went down, I was told by 2 cabbies. Thought of your experiment.

Venmo baby!!!

amen brother!

The way I see it the yield you get determines the value of the money. The last 10 years in this country wealth hasn’t stayed because we’ve been working with low-quality money.

Some of the credit unions pay a little better. ICU for example has a decent rate on its CDs and savings accounts. http://icu.org/index.cfm?pi… And they’re insured up to $600k.But I’m mostly in highly rated double tax free municipal bonds too, for the same reasons you mention.

My ING Direct savings account gives me around 1.2% now. It’s not awesome, but it’s FDIC-insured, and relatively easy to deal with.

This environment is actually helping some banks strengthen their balance sheets. Their cost of funds is the lowest in history. They can borrow funds from depositors are record lows. Likewise they borrow from the fed (the discount rate is at .75 I think) at cheap rates as well. They can also lend those same funds at a much higher rate.As you mentioned, borrowing money (for some) is very cheap. I’d love to find out how much of the stock market growth of the recent year is magnified by leverage.By the way – do you try to use interest rate immunization techniques?Greetings from Peru,Marco

A very interesting post there Fred, we have the same problem here in the UK. How to keep your assets in line with inflation. I think property is probably a safe bet in the longer term despite the issues in this market at the moment.

Land has real intrinsic value, great point Stephen. How about a fund that’s based on real estate (so you can liquidate easier).

I guess you could build up a tax free portfolio of companies who specialise in land acquisition and development?

Over a 20 year period, real estate has always bridged the shoulders between “triumph and disaster”. It will remain so in this instance.

Fred, there are banks that offer “decent” interest rates (~3%) if you put money into their bank and do 2 things:(1) Have at least 1 EFT debit or credit per month on the account(2) Use their debit card 10 times per monthIf you don’t qualify for both of these in a month, you still get some interest, but small. However, considering your previous post about not carrying cash (and I’m not quite there yet, but it’s pretty rare that I have more than 50 bucks in my pocket), if I can get 3% monthly on my money and simply use a debit card instead of cash, it’s a no brainer. I do believe most of these accounts limit the 3% to the first $25K, but that’s still better than a poke in the eye, and “easier” for the lay person than muni bonds (although I like your bond suggestion and am going to look into that).Do you see any downsides to these new fangled bank offers?

that’s interesting scott. i’d not seen that. i’ll look into this. i don’tknow enough to comment intelligently yet

ok – here’s a link to a promotional blurb for the one my wife and I signed up for:https://www.providentsmartc…Look forward to your feedback/comments

Groovy Scott, great find and share!

Money market funds are going to be out of business. They have expenses, but nothing safe to invest in at a positive interest rate. Meanwhile, you can get > 1% FDIC insured in a savings account, a bit more in a CD, from your local insolvent cash-hungry bank propped up by the government – see bankrate.com. Intermediation lives!

Yes, there are problems. Most of them require direct deposit of a paycheck, and a certain number of transactions, usually more than 1; more like 6 to 12. There are various penalties if you don’t comply. These bank offers also often require same-state residency. Too many hoops.

Fred,I am assuming this is for the “safe” portion of your portfolio? And since you don’t keep it in cash, is liquidity an issue?While I do not recommend film investments for everyone (you have to know the market very well) some such investments are yielding 20% to 30%.Even if you trade some risk for security in a safer film investment, you could assume a 10% to 15% return. (For example, last in first out with a minimum guarantee backed by an L/C payable in 2 years with a 12% return).The good deals are few and far between, but assuming you could get a good one, why would an investor chase 0.00 or borrow money to get into the stock market when the capital markets look to be volatile if not frozen (with a lower case f) for the foreseeable future?And aside from film, are there any sectors that you can comment on that yield low double digits? And what is the risk look like there?Thanks, Phil

this is for the “safe” portion of our portfolioi think of film as risky, like venture, private company, and real estateand i don’t know anything about film, so i stay away from it

I don’t know anything about film except a little from what I read, but the industry looks fascinating.I would guess film is like venture investing. You find teams you believe in and trust, and back their projects.But the way film production works is pretty amazing. All these specialists come together like a free lance army and work for a couple of years (months for low budget/fast) to produce a film. The networks of the best crews/directors/producers are the value drivers.

It wouldn’t be an investment, exactly, but contributing some “fuel” to this film project on RocketHub might be an interesting learning experience with respect to film distribution.

there are also a bunch of great film projects to fund on http://kickstarter.com

I am biased in favor of RocketHub, partly because it was co-founded by a member of your comment community, and partly because Kickstarter rejected an idea of mine, as I mentioned in a post on my old blog, “Sex beats Stocks”.

You’d think that these circumstances (and the similar issue in realty/property investing right now) might open up a few more angels’ wallets, but looking for a seed round right now, I’m seeing less activity rather than more, and plenty of conservatism in the angel investing space 🙁

If you are looking for angel money for a seed round go find folks with substantial oil income. The US oil patch is flush w/ $$$. A crappy hotel room in Odessa, TX costs $200/night. Ever been to Odessa?Current oil prices are ballooning oil patch incomes.

The thing you have to worry about right now Fred is the fact that if you are parking your money into a bank that is giving yields higher than 0, they are probably weak and desperate for deposits.A great example of this kind of behavior is Ally Bank (formerly GMAC).

that’s right. chasing yields is dangerous

With FDIC insurance at $250K per account and the ability to package accounts with very minimal ownership identification differences, the world is your oyster. Just don’t rub up against $250K in any discrete account.

That’s exactly what I was going to write. FDIC insurance means you’re good to go, even if some of these banks are being aggressive in their chasing deposits. Just keep it under the threshold. Good stuff.The low interest rate environment are the major reasons that so many have piled into the stockmarket over the course of the past year. Willing to take on that risk to capture yield/gains versus paltry savings/moneymarket rates.

well, the market rate seems more like 1.25% at bankrate.com, not 0 but not great either. You are FDIC insured up to $250,000. Beyond that, post-Lehman the Feds seem unlikely to let depositors lose money and planting thoughts about runs on banks.also, credit has been a little screwball last couple of years, so if you really know what you’re doing it can pay to chase yield like it can pay to pick stocks, but the optionality runs the wrong way, capped upside, 100% downside.

Fred, I wish you concerned yourself more with how wrong it is that rates are where they are. Anyone preaching the gospel of entrepreneurism should be calling out to Audit the Fed.We don’t need another bubble, there’s plenty of fat creative destruction that should come from feasting on all these old bloated protected industries.

the interesting thing is that the fed doesn’t control the yield curvethe market doesthe fact that there are buyers of treasuries at these yields is astonishing

?The Fed fund rate drives this on one end (and should be far higher now)… on the Buy side we have “the fear,” every piece of bad news brings more “please protect me” investors to the Treasury table… you would argue Obama admin isn’t applying “the fear” at world class levels?We ought to let Volcker run roughshod over the whole thing, and pay him based on how hard the banks squeal.Technology needs to grow some nuts, and start remaking everything. It can’t happen if we side side with the protectorate. Hell we should be radically advocating web based government, success defined by how many public employees we can fire.Example: If you want to take down cable, political donations, and congressional testimony is not the answer. The noble capitalist is looking at pure competitive plays – weird shit like HAV (blimps) to bring satellite spectrum back into the lead.

i agree about the role of capitalism. we are eager to play a role inreshaping the world of finance.

i’m doing my part morgan…..working on a conspiracy commercial and going to air it through saysme.tv! lol, i love your company, way too much fun for a guy like me 🙂 and the people at your company have been very helpful and supportive, have to give props for that. keep up the great work!

At this instant in time, the country desperately needs cheap money though the actual supply of debt is a myth.A more important issue is that if we are to be ruled by an administration which is going to mandate touchy-feely policies (green energy), they should at the very least ensure the damn products are being made in America and that the owners of the companies are American.We have weird policies, funded by debt held by foreigners and allow the same bunch of foreigners to produce the mandated products and to own the means of production.Solar Power is being dominated by the Chinese and we are funding the projects and the manufacture of the products by the companies owned by the Chinese.Huh?I at least want our folks to be shrewd. Is that too much to ask?

If we’re just shrewd, we’ll end up like Germany at best. The problem is we are not homogeneous. We are actually a far flung scatter shot of like minded clusters. We’re better served by a Euro model. If our states are the ones handling our taxes, regulations, and safety net like in Europe, we will have tons of pressure on the Fed to keep monetary policy tight. CA will be Greece, and they will have to cut the labor union off at the knees.I really think Fred’s investment class out to be gearing up to take down SEIU / AFSCME. A 20% savings on public employee salaries is $278B – and that’s not including pensions. 2012 elections should be all about GOV2.0 – and tech should be funding whoever is most ready to automate government and thin out their middle management – like the private sector over the past ten years.It’s hard for me to take solar seriously, we’d do just as well to let the photo sensor market continue to drive the tech until it actually makes sense.

Lot of info in there and not sure I understand exactly what you are saying.In great measure the US will sink or swim together. Make no mistake that the Obama administration is not going to cut California, Michigan and Illinois loose — unlike Germany which will allow the European Union to fold before they come to the aid of Greece.Allowing these particular three States to float off into the ether would be electoral political suicide. Not going to happen.Why did anybody think that Germany which has averaged about 3 wars per century with its neighbors would make a good “teammate” when things got frothy. Their solution for Greece — hey, go sell a couple of islands, you Greeks!Along the same lines, this administration is not going to do anything to diminish the political clout of the unions — witness their support of UAW in effect making a union into a sovereign nation in the GM deal. So don’t look for the administration to do what is really required — hit the reset button on the value and delivery mechanism of modestly skilled labor. Again, not very good politics.Tech is not going to act in a responsible electoral manner when the centers of technology are in California, NY, Boston, Chicago — hell, even Raleigh and Austin are weirdly liberal in their own manner. Tech talks well but is a reliable funding source for Democratic politics.While I agree that solar/wind/thermal are all neat little political toys, the real problem is that they steal attention from things like off shore drilling and nuclear power. Hell, nuke cannot even get a seat at the table and the administration has delayed off shore drilling by at least 3 more years with its recent announcement rejecting the Bush era lease competitions. They need to “study” it a bit more.As you well know, weird Austin has committed about 15% of your electrical future to a single unproven and 3 x overpriced solar plant while passing on doubling down on its stake in the S Tx Nuke. The numbers make any financially astute observer want to puke.

i would bet on a big comeback for nuclear. there aren’t better options in the short term

I am big on nuclear, locally and globally. http://democracyforum.blogs…

The beauty of nuclear is that it can be driven solely by government loan guarantees (a la Southern Co deal) rather than requiring real cash. Even partial gov’t financial enhancement will work.The design and construction generates lots of high quality tech and construction jobs to say nothing of the manufacturing demand created by the process elements themselves.When finished it leaves a huge demand for operating jobs.Lastly it diminishes the demand for imported oil either directly of by supplanting national demand.It improves air quality and has an generally untapped thermal asset in its heat exchange.It is truly the low hanging fruit for the American economy on every possible plane. It is politically irresponsible not to be building nuclear right now.Two per state minimum.

are you honestly going to dispute morgan’s point that those who advocate entrpereneurialism should be supporting the audit the fed movement. please.

i don’t get excited by the idea of auditing the fed

Hmm…. why not? I’d actually love to see a full post on this one.

The bureaucratic nightmare part of it may be a turnoff.As you’re well aware, rationale capital banking, and US banking have become two disparate things. Fixing it is like trying to use my old TI-99 as a smart phone. Better to just move on. Wish I knew what form the next big monetary shift was going to take, but my magic 8-ball’s answer icosahedron (that’s for Kid’s eschatology) sides have become all rounded 🙂

It isn’t hard to remove banking from investment. Toss bundling. To receive FDIC insurance: require loans actually be held on books. Overnight, all the “talent” will get out of banking. It will become a boring mundane low paying conservative operation – and it will lead to more local banking.Yes this will increase the cost of credit. But as we’ve seen liquidity doesn’t provide credit. Forget subsidizing home ownership. We need to be a nation of renters. Mobility is the new American watchword.What’s more there are whole new ways of providing credit – stuff that Fred should love to get in on.Remove the premise of Federally backed investing and everything gets a lot more interesting.I didn’t sign up to be an entrepreneur so I could work in aid of American Corporatism. Fred shouldn’t either.

why don’t we just build the new way instead of trying to change the old wayit never works anyway

Problems — big modern complex problems — are always best solved by “shorting” but not immediately eliminating the legacy system and then creating a new and better system.The old system is comfortable and familiar and the new system is going to have some start up bugs.A perfect example of this is when the draft ended and the Army became an “all volunteer” enterprise. The Army still continued to have 3 years of draftees working their way through the system while building the volunteer force.The all volunteer force initially had some problems and it took a couple of years to get the pay scales and recruiting just right. Now it works like a champ.When the volunteer force took root, the Army allowed many draftees to shorten their service requirement but not before the new volunteer Army had taken root.On the other side of the change, the Army was greatly improved and was able to fight better.This is exactly the problem with the health care debate — the new program mandates the immediate destruction of the “old” system — worse still it depends intellectually on the “demonization” of many institutions, persons that consumers are not prepared to demonize — while blithely lying that you “can keep your own doctor”.If the new way is so good, it will crush the old way based upon its realized efficiencies and qualities. Big IF!

i’d like to see a parallel path in health care for sure

The biggest problem with the larger issue of “health care” is that it has constituent sub-issues of health insurance reform, expansion of health care coverage, health care delivery reform and health care financial reform.These are not the same issues by any measure. Unfortunately, the current effort is trying to deal with all of them simultaneously in the face of huge amounts of misinformation, conflict and partisanship.This is tantamount to trying to replace the engine in a car driving down the road while simultaneously debating whether it should be a gasoline, diesel or electric engine of either English or metric measurement. Stopping the car until the debate is resolved is unfortunately not a viable option. Worse nobody trusts anybody on the other side. We have had more cordial communication with our enemies during wartime.If we had everybody at the table who has skin in the game and better statesmanship/leadership, we could pick some low hanging fruit.Who would oppose the standardization of health insurance contracts across state lines?Who would oppose the deductibility of insurance premiums for those who purchase their own health insurance? After all your employer is buying your insurance with before tax dollars.Who would oppose the conversion of the dispute resolution mechanism from state based litigation to nationwide binding arbitration? Check your brokerage account agreement — the securities industry has been doing it for decades.Who would oppose the production of more doctors annually with many doctors becoming more general GPs? Put more doctors in clinics with a more advanced nursing professional and get these folks out into the hinterlands where they would not compete with urban medical professionals who believe they are entitled to become millionaires. Get the AMAs thumb off the medical school accreditation process and turn on the tap.

i suspect that is where we may end up after this effort fails

I’ve been doing an informal survey for a business idea checking HSA vs PPO. In every state, no matter what kind of buyer (age, family size, pre-existing), in every instance the HSA provides the same level of coverage (or better) while saving $1500+ per year.Meaning, all other things being equal: maximum out of pocket cost for the HSA is always less than a PPO.I’ve read every argument against them I can find trying to figure out why Pelosi Obama has been against the HSA – finally it hit me – it is the unions.PPO gold plated health care is the only thing unions have to brag about to non-union shops, and once an employee gets $5K+ socked away in an HSA, it is almost impossible to get them to want a PPO.5 years ago, Indiana’s public employees got a HSA choice, and 4% signed up. In 5 years, 70% have chosen it. HSA users are using 67% less doctor visits and spending 35% less.That Obama hasn’t made HSA fundamental to his plan is the proof anyone needs (Fred) he voted the wrong way in 2008.

What a brilliant, insightful and well researched comment. It adds to the knowledge base of this discussion.I suspect the fundamental issue is one of control. The Pelosi/Obama wing of the Communist party wants to have their fingers wrapped around the Nation’s steering wheel while the HSA approach requires a bit of independent thinking by the sheeple — ooops, meant people.I am a huge fan of HSAs but I must say that most folks with employer provided health insurance are quite content to let someone else do their thinking.It is sad.

Thanks Morgan, I enjoy your rebellious but rationale views on this topic.Loans have to be held, so banks are required to have cash equivalent to all loans? I’m a big fan of that idea!There could be a new entity, not a bank but a risk investment structure that isn’t FDIC backed but works like current banks.A mobile nation does make sense to me, but the reality is that many people do choose to remain in one locale for their lives and make a big investment into that community. That’s not a bad thing, so ownership suits them (well some property taxes feel like renting…)

Have you ever seen net worth figures on renters vs homeowners? There’s a stunning disparity favoring owners. Even post-bubble, and for good reason. Home ownership is a forced savings program. Real estate is still a good investment (Like gold, nobodies going to manufacturer more land), and a mortgage is the only way most Americans invest on margin.A “nation of renters” would also mean that SOMEBODY owns that property and if you want to see how well that works, take a look at, well, all of human civilization up to the last 200 years (or even to the FDR era)

Shane, we got into this mess largely because our attitudes towards homeownership were not value neutral. Even now we are propping up real estate prices with FHA $8K tax credit etc. And that’s the effect – higher prices.We all know smart guys with dry powder who are knocking on the doors of banks offering 40 cents on the dollar and the banks are laughing! Why should they sell?That’s not the way it is supposed to work in a bank crisis. An FDIC insured bank crisis is supposed to be like stumbling into estate sale on a rainy day they forgot to advertise. Even when we’re cozy with fractional banking, it doesn’t mean we can’t expect a bank being unwound to actually have its foreclosed assets sold at auction. Why the hell not? Let the bankers starve. Instead we have banks, borrowing money at 0%, and sitting on capital just so they can get the magic Friday call and take over the bank fail down the street. No. We should keep it at level one. Let the guys with cash have the windfall payday. We want banking to be boring, transparent, and barely profitable only because the cost of credit is paying the bills – otherwise WHY allow the FDIC to stand behind it? FDIC written on the side of the building should mean nobody inside is making half a million dollars a year.Worse yet Shane, the cost of homes is still a rip off for the people who actually have the 20% down and proveable income. Why should they have to pay more? How insane is it that Fannie and Freddie are basically the entire home sales market? That’s not a service to Americans, that’s disgusting.Lastly, just cause I’m already spouting off – the tech industry ought to be telling Obama that we want any foreign student or worker who buys a house to get a green card. I know I’m daydreaming, but I bet 50K guys from India living in Detroit would do wonders for that market right now.

You have covered a lot of ground in your post and it is difficult to touch on every point but I would opine that like much of the debate about the virtues of home ownership, banking, the current situation and the recession — the basic disagreement or point of conflict is about what caused it and how it happened.We had pretty damn good systems that we allowed to spin out of control for purely political reasons.Allowing or compelling otherwise sound lenders to make loans to unqualified borrowers on unwise terms absent credible credit underwriting was a prescription for exactly the disaster that resulted.How does one lend thousands of dollars with no income verification? This is the intellectual and banking equivalent of telling an Airedale puppy that you have left it three bowls of food as you are leaving for the weekend and saying — Pace yourself, old boy!No sooner did we lend folks huge amounts of money with no credit underwriting than we allowed kids with mousse in their hair and MBAs to develop phantom securities which pretended to make chicken salad from chicken excrement. How does anyone take any portion of a less than investment grade credit and magically transform it into not just an investment grade security but a freakin’ AAA or AA security. Answer — the rating agencies wanted to get a date w/ the Prom Queen and they were prepared to do anything to do it.If the lousy loans were not enough; and, the fabrication of ridiculous securities by kids just 4 years out of school were not enough; and the rating agencies pulling their dresses over their heads were not enough; THEN INSURANCE COMPANIES WERE WILLING TO INSURE THIS ENTIRE PILE OF CRAP.I go to this length to simply state that the American banking industry will be OK when we get this series of linked errors out of the system and ensure it cannot be repeated. That will take some time and regulation. But it will work.

The problem with FDIC insurance is that it benefits and protects the depositor not the bank/lender.I agree completely that the banks have to have some more skin in the game but the more likely route is the Fed window rather than the FDIC.

lol, looks it’s vocabulary day here in fredland! thanks for sharing, mark!

yes i agree with morgan, i’d like to see a full post on this as well — if you truly believe it you’ll have no problem backing it up, right? in fact, i’d like to see ANY post on the federal reserve. do a site search for “federal reserve” on avc.com and you’ll see what i mean.of course you are not excited by the idea of auditing the fed because, up until now, you’ve benefited indirectly from their inflationary monetary policy, and so the incentive has been to remain ignorant of how the fed operates. so long as they’re giving you bubbles, it’s all good!but every scam comes to an end, and in this next round of doom and gloom, even folks in your social class get screwed. that’s how big the scam is. open your eyes and it’s plain to see, they’re not even hiding it anymore.

Auditing any financial enterprise which is involved in the granting of, the evalution of, the purchasing of or the manipulation of “credit” is not just a good idea, it is an essential and fundamental business discipline.This would be like going through life without the benefit of a medial physical or never setting foot on a scale.It is sheer nonsense not to audit the Fed or to force the Pentagon to balance their books and produce financial statements.Audits identify problems which honorable men can then fix. Audits create confidence in the principles and practices of complex financial undertakings.Audit every single element of the US gov’t which touches our money including Operation Rainbow/PUSH.

“Audit every single element of the US gov’t which touches our money including Operation Rainbow/PUSH.”LOL Jesse Jackson is a government entity now?

Fair play. I must admit that though Rev Jackson’s lips are permanently welded to the gov’t teat and at least one tenacle at all times is in the public purse, he is not formally an element of the government.It only seems that way.Let me modify my rant to say that gov’t money of all kinds should come with a requirement to audit their expenditure no less than a gov’t military contractor must prove up the cost of their expenditures.Operation Rainbow/PUSH has never — that’s right NEVER — been audited by the US gov’t and that’s just wrong.

I am all about auditing and transparency and all that.

Try some Brazilian bonds (now at investment grade).You may get 8.75% yearly + benefit from BRL appreciation. It is low risk and can be an alternative between 0% and venture capital.

What about moving the money into foreign or global accounts, do they pay any better?

It is higher. I made the same recommendation.

At the end of the day aren’t you just being compensated for currency and sovereignty risks?Fixed income has to actually be “fixed” income to make fair comparisons. If not, then you are just speculating in currency and political risk.

I wasn’t referring to sovereign bonds, -rather to straight deposits into regular accounts that yield a higher interest rate.

Probably an inartful use of the term on my part. I am referring to the risks that are unique to a particular country as it relates to its tax, withholding and banking laws. All in addition to the inherent currency exchange risks.Years ago I used to invest in Mexican cetes and tesobonos which were impacted by the peso exhange rate and the fact that they were otherwise in Mexico.I used to do this through the Laredo National Bank on the US side and they were quite expert on the matter. It would have been very difficult in those days to have found any reputable and trustworthy outlets for such an investment but I was lucky to know some folks at LNB.Rates were 45%, so I felt adequately compensated for the risks. Today with much lower rates of return, I would not feel adequately compensated for what I perceive to be other risks.

Bloomberg reported that banks we saved with our money made $56 billion last year taking our deposits at less than 1% interest, borrowing at zero from the Fed, and then buying treasuries at 4%. So in essence they are taking our money, paying us no money, then buying bonds that we have to pay back at interest to the banks. This has to end. In hindsight I think letting the big banks fail last year even if it caused a mini-depression would of been the best way for real reform. Instead we keep getting fleeced. Normally people don;t seek help unless they are really sick. I agree with your move Fred. Your mattress or coffee can in the cupboard might be safer than a bank anyway. lol

“banks we saved with our money made $56 billion last year taking our deposits at less than 1% interest, borrowing at zero from the Fed, and then buying treasuries at 4%. So in essence they are taking our money”That’s just not right.

It wasn’t simply a choice between saving them or letting them fail. We could have saved them but made it sting, and limited their ability to profit from regulatory capture during the recovery. If our Treasury Department were run by men like John Hussman or Andy Beal, the obscenity of too-big-to-fail bankers gorging themselves at the public trough last year would never have happened.

At the end of the day, this Lost Japanese Decade approach simply rebuilt the balance sheets of banks “slowly” rather than on a single afternoon.The alternative was to allow toxic assets to flood the marketplace and put all banks in the soup. Now they were able to use the zero cost of funds to buy Treasuries and to use the spread to camouflage and heal their wounds.Time solves most financial problems particularly when interest rates can be manipulated to buy time.

Are they “camouflage and heal their wounds” or just executing a new form of lotting. Managing the rules to give themselves a risk free spread at our expense!

If you don’t like funding banks long-term investments with your short-term funds, take your money out of the bank and go buy the same 4% Treasuries for yourself at TreasuryDirect. What’s that, you can’t manage your own liquidity and you need the bank to do it for you? Well, there’s a price to pay for their services…

Someone who is “surprised” that money markets are yielding 0% turns around and then gives investing advice? 🙂

what i was surprised is that they are still yielding 0.00%i guess i should have been clear about thatseems like rates have risen elsewhere recently but not in money markets

Thanks for the advice. Makes me want to put money in more useful areas. The comments on the post really read like a longer article itself, today more so than others.

BTW I forgot REAL vs NOMINAL. I am curious if the Zero Yield was real or nominal. If nominal it could go negative due to inflation. This was a big beef I had during the Bush years. Many quarters GDP was positive but less than inflation so we actually had a hidden slow cooking recession during much of his Presidency.

We actually had a point where Treasury bills went negative on yield during the financial crisis as people/corporations were looking for places to keep their cash. After WAMU went down and rumors swirled around C and BAC even the “Fortress 5” didn’t sound like a safe place to have anything over the FDIC so into T-Bills it went: http://blogs.wsj.com/market…

For some considerable time period, WalMart’s credit was arithmetically superior to that of the US gov’t. Maybe still is? LOL

“I told him in an environment where cash in the bank yields 0.00% two things happen. First, people chase yields elsewhere and the US stock market has been a big beneficiary of that.”I’ve noticed this, in particular, with an oil royalty trust I own a few units of. This trust just distributes royalties from certain oil fields, so the biggest variable in the distributions is oil prices (tax rates, down times due to weather, etc., and production rates are other variables). When oil prices peaked at ~$147 per barrel, this trust traded for about $107, if memory serves. Now it’s at $96 and change, with oil in the low $80s. I tried to buy puts on it yesterday, but didn’t get filled at my bid price. I’ll try again Monday.

“we like a portfolio of highly rated (AA and AAA) municipal bonds.”How confident are you in those ratings today, given both the track record of ratings companies in recent years, and the parlous state of municipal and state budgets?

not veryi generally rely on our bond manager for his experience and knowledge andalso ask aroundi’ve heard the NYC sewer bonds are pretty solid

Are those revenue bonds? Are they now considered more attractive than G.O. bonds in general?

i’ll find out

Great, thanks.

yea, I’m with you – I worry about our state, the great state of NY, defaulting on their bond commitments. Even the revenue backed bonds don’t fill me with great confidence. G.O’s are scaring everyone, but read the fine print on some revenue backed bonds and you’ll see there are significant potential “outs”

Any state which would seriously consider managing its cash flow by failing to pay entitlements or tax refunds on time is capable of talking itself into doing anything.Remember that when both Russia and China became communist they reneged on all of their sovereign debt.I collect late 19th and early 20th century Chinese bonds for their quality engraved artwork. I sit in my study with walls covered with beautifully framed bonds issued in four languages with most of their payment coupons intact. Wonderful artwork.The Swiss have tried for years to get the Chinese to honor their commitments and who knows when enough bondholders are dead and buried and the Chinese truly need to access international capital markets, maybe they will.I will be ready when they do.I would bet anything that California, Illinois and Michigan will default on their debts. After all, didn’t GM do the same thing and the US gov’t came to their aid?

Interest rates and credit markets seem like too much of a mystery. This is the reason my partners and I started BondSquawk.com…so we can leverage the powers of the web to help shed some light on the issue. We will love to hear from all of you on any suggestions of topics to cover.

ProShares UltraShort 20+ Year (TBT) is an ETF that moves inversely with US Treasury bond prices. In other words, if interest rates rise then you make money. I think it’s getting harder (although not impossible) to envision a future in which we won’t have substantially higher interest rates. Might be a worthy add to portfolios if you’re concerned about this.BTW, watched I.O.U.S.A. this week (http://www.iousathemovie.com/). If you want to have the crap scared out of you about the impending issues with the debt that’s the movie to watch.

agreed, IOUSA is a great movie for people who like bad news — thanks for sharing jon

What’s interesting to me is how risk averse your long portfolio is compared to a non-wealthy person. I think most people understand this but never really absorb how those better off protect their wealth. Discipline.

we take a lot of risk in our venture and private company investments.so we like to take very little risk with our “cash”

Take a look at RiverSource Ameriprise old fashioned annuity quasi-retirement contracts. Not a very flashy product to be sure but yielding very nice returns.The beauty of these type annuities (not variable annuities, mind you) is the ability to pile on at the original contract rate for years into the future.These are great vehicles for funding long term trust funds (e.g. children’s trusts, etc.).I have some old ones that I can add $$$ to which are yielding 5-9% guaranteed and one that is yielding 11% but is closed to additional $$$ right now (and likely forever).If you are interested in a bit of sovereign risk, consider cetes and tesobonos. While Mexico has not yet been granted statehood — inevitable in my view —, you might be interested in looking into the historic precedent presented by the illustrious “Brady Bonds” when Nick Brady, et al, Sec Treas rescued Mexico with more effort, set Wall Street up for a killing and then went back to WS and fed at the trough with his brethren.Teaching point being that nothing new has been happening on WS for decades.Keep this thought in mind as we see how Mr Obama and Mr Geitner decide how to deal with the impending bankruptcies of California, Illinois, Michigan and Alabama.

I find the more intellectually stimulating implication of Fred’s typically interesting post to be the more fundamental question as to what one should be doing right now — lending money to banks/financial institutions or borrowing money from banks/financial institutions.I believe now is the time to borrow as much as you can at the lowest fixed rates you can find and sit on it until you can repay it with hyperinflated dollars at some future date.[Ooops, I guess I may have revealed the Treasury’s strategy, now isn’t that right?]In some ways the application of additional debt — gobs of debt in my view — to an otherwise orderly balance sheet is simply “pre-paying” a future inflation dividend.You get and distribute dollars today and can repay with quarters in the future. There is even a huge tax efficiency as the proceeds of borrowings are not “income” and therefore you are positioned to avoid Mr Obama’s latest round of taxes for all you top 1%-ers.Here’s the other big payoff — if you can swing the debt, now is a great time to have liquidity as bargains galore are continuing to appear. Now is the time to buy all the big expensive toys and to buy good businesses which will otherwise disappear in the future.A bit of a contrarian view but a movie I have personally sat through before.

just did that in a big way JLMbut i don’t feel comfortable advising people to borrowthat’s what got us into this mess

Please take my comment purely as “musing” — thinking out loud. I would never expect you to give such advice as it requires a trained ear to understand the implications.Nonetheless the question remains — why would prudent business persons not borrow gobs of money when money is so cheap to rent and when it can be deployed in enterprises which will undoubtedly outstrip the rate of inflation?Money — equity capital or debt capital — is just a commodity w/ a price tag but one which can be repaid with inflated dollars at some time in the future.Much more courage is required to buy low than to sell high.That is also the power of age, wisdom and experience. I pray for such a crisis about every 15 years and dear God please let me be liquid when it comes. I have not been disappointed yet.

If offshore banking is an option, you will find much higher rates than in the U.S.

One should not discount that equities can in fact be a “bond” if the underlying company has no debt. The company’s cash flows are the coupon payment, it’s not a contractual payment, but it takes on all the characteristics of a coupon nonetheless. Companies paying out large dividends with little to no debt are basically paying a bond coupon to the equity holders.Low coupon bonds during inflationary periods can be virtually worthless. I think some historical perspective is in order:The following table shows the inflation-adjusted value of $1,000,000 invested in thethree asset classes, before personal income taxes. Treasury Bills Government Bonds S&P 5001930–1954 $760,000 $1,220,000 $4,600,0001933–1954 $730,000 $840,000 $9,500,000Careful with those bonds, you might find that after inflation they are actually worth less than when you purchased them.

Talking from the trenches.

It is indeed a dangerous time, and a wise time to not chase yields. Taking debt is certainly a way to try and grow your wealth, although i have a feeling the next decade is going to be more about navigating land mines to simply maintain real wealth rather than grow it.I saw some comments about people finding great deals here and there for interest rates.. keep in mind, no matter how great you are at finding deals, you cannot avoid the risk/reward curve. Those promotions are likely either limited in scale allowed, or coming from institutions you should steer the hell clear of. About a month before they collapsed, I noticed Washington Mutual branches were all of a sudden offering 5% interest on new deposits. If something seems too good to be true, it almost certainly is.The real question IMHO is what is the safest way to hold cash?

Great post. What are your portfolio companies doing with their excess cash post fundraising? I bet they are facing the same dilemma in their corporate coffers that you are in your personal accounts.

i recommend very short term treasuries. they don’t pay any yield (see theyield curve i posted) but they are safe. and preservation of principal isthe most important think for a startup’s cash balance

Fred:Given the way sovereign / state debt default risk is rising, I wonder if municipal bonds, even highly rated ones, will remain as good a risk balancer in the way you use them in your investment portfolio. One of our well respected pundits reckons that a basket of high dividend yield blue chips would work better in the current environment:http://www.finance30.com/pr…The writer (Bill Wright) is a former senior finance executive who has spent 25 years managing finance and investments in financial institutions, insurance companies and corporates.

Definitely good advice. It’s a little scary to see a yield of 0% on your money!

What do you think about investing in a TIPS ETF (IPE)?

My desire is for more concise explanations of what’s going on. While it can be tough to do politically, that is what gives me the best experience as a user.

“And then wait for rates to rise. Because I am certain they will. “you’ll be waiting a long, long time. rates are not going up for a long time…but say they do, the ‘cost of waiting’ will still be incredibly high. grabbing 3.50% on the 10 year means you are earning 3.50% more per year than in money market. if rates stay low, after 2yrs, you’re 7% behind, 3yrs, over 10% behind…. if short term rates then finally rise, they’d need to average ~5% for the next 7 years for you to just *break even* over those 10yrs. now THAT is taking a risk.you’d better be right that short-term rates not only rise, but that they will rise high and quick. likley you’ll be in hole that you’ll never fully climb out of – that is, grabbing 3.50% TODAY would have been the right call.

i’m talking about your cash balancess, not your entire net worth

That’s why some believe the Treasury bond bubble is the biggest bubble of all. I don’t think the Treasury bond bubble will hurt like the housing bubble, but the Treasury bond bubble is enormous and not discussed much

Yup

Great summary – and just what the government wants you to do!By driving rates to zero, the Fed is attempting to encourage transactional activity in the marketplace. You’ve identified one option – invest in ‘riskier’ options like term bonds – but there are many others.Preferably, from the Fed’s point of view, you will spend that money instead of saving it. Given our economy is some 70% consumer based consumption is the key and a lower promised return on your investments makes spending now more attractive.Unfortunately, at the same time the more politicized part of our government is creating so much uncertainty consumers don’t want to spend their nest egg today as they are uncertain whether they can rebuild it in a reasonable period of time.Uncertainty over job security and uncertainty over wealth (primarily stemming from a nonfunctioning mortgage market) is keeping the economy in stasis mode.But, hey, at least you are investing out the curve!Thanks for the economic stimulus and keep it coming!

perhaps….though i view it from the perspective of the US dollar, meaning i don’t think the US dollar is done declining….so where will purchasing power go? the dollar index recently rallied from 75 to 80, meaning the USD rose against pretty much every currency, save the australian dollar, which was about neutral. gold and silver also rose against the dollar during this time as well. so to me, the case for them is still strong. though gold has now attracted speculators, so i think in this next leg up, the market will be more volatile, IMHO.