Fewer And Larger

Those are the two words that come to mind when I looked at the Q4 2018 PWC/CB Insights Money Tree Report.

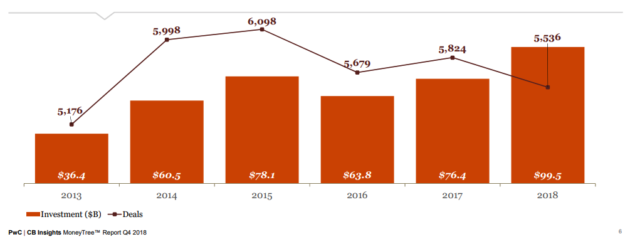

2018 saw the venture capital business moving to larger and larger deals. There were roughly 200 deals around the globe in 2018 where $100mm or more was raised.

And yet the number of total transactions declined slightly from 2017.

This trend is much more obvious if you look at the six years from 2013 to 2018. Total deal activity has increased less than 10% while total capital investment has almost tripled.

These trends are unsustainable. It is certainly attractive to de-risk by moving upstream to invest in more mature companies, larger rounds, etc. But if we don’t reseed our fields there won’t be as many of those mature companies in the future.

And that is why USV remains a small fund/firm which allows us to invest in Seed, Srs A, and Srs B rounds. It may not be fashionable to do that right now, but I am certain that it is and will continue to be profitable.

Comments (Archived):

It’s a lot harder to be an early stage investor, as you need to do more of your own homework instead of waiting for others to do it for you in the later stages when the success signs are more obviously visible. Of course with more risk upfront come more rewards on the multiples.

Yuppp. People really dislike risk. Don’t understand it. Uncomfortable with it. Can’t rationalize it. Can’t message it in a way that can get comfortable with it. So they back away. I just love going against the herd

I think from what you have done in the past you are almost certainly more suited for the risk than the average angel investor. That probably would be a good selling point for you when you are trying to convince someone to take your money. I am not looking for investment obviously but that would work with me (and I have used it successfully on others in a different context).I am reminded of things that I am more comfortable with than the average person. With those things I can wrap my head around the risk in a ‘seat of the pants’ way which makes me very comfortable with the process and how to bail or correct if I need to. But someone who is not me, well, the same thing will seem daunting because they don’t have all the answers in their brain and can’t formulate a way to avoid disaster on the fly. And no you can’t get the answers by reading or asking someone else. Doing that you lose nuance which is important in making decisions that have a high probability of being correct.

What makes risk such an incredible opportunity is that most people fail to see risk in events where day-to-day volatility is low (e.g. receiving a paycheck at a Fortune 500 company) and weight too much risk in events that have high day-to-day volatility (e.g. being an independent contractor in your profession).This failure makes most people fragile to adverse events and you anti-fragile. Put another way, most people trade known upside for unknown downside. You (and I) prefer the opposite.

I am you.I look around.I see almost zero competition.If Blockchain is a major new trend in tech, you are golden.If the major innovation wave comes in energy or bio, you are copper.

You sound like Ozymandias 😉

Par for the course. Cycle of life.Better to be b2c or b2b? Better to be centralized or distributed? Better to go wide or deep?It all depends, and it all changes over time.What we’re *really* seeing is, where it’s easier to be average at a given moment in time (that’s where the herd migrates).

I don’t know so much about the average part, but the herd has definitely moved downstream. But, that is where the grass is growing.I disagree with PMarcA’s ‘ internet will take 50 years to mature ‘ statements. Its mature now. The next wave will be in energy, or bio or sensor level automation (which may trigger innovations in energy & bio).As I have said before, Blockchain could be the piece that really makes sensor level / IoT automation go…… but a long time ago, a technical lead at Bucyrus ( I will save you the googling: https://en.wikipedia.org/wi… ) told my wife:’ Honestly, you are going to really have trouble getting rid of drivers. All you can trust the AI to do is to shut things down when the truck is outside of its parameters. ‘The truck he was talking about is this one (CAT bought Bucyrus in 2011 + my wife has had & still has quite a cool career going): https://en.wikipedia.org/wi…Driverless cars? Ahhhhhhhhhhhh, don’t think so.IoT that does more things than a Kill Switch? Ahhhhhhhhhhh, don’t think so.Also, if tech is back in a heavy capital cost of product phase – like when building Fairchild Semi required massive amounts of startup capital just to build the first fab plant – then the initial deals will likely get bigger and the number of funding events smaller.That statement fits innovation waves in energy & bio, not so much SaaS.Those big bets are not an open + tools sweet spot.That would worry me, if I was Fred.

IMHO, there’s more, much more: The key word is information, and, of course, IoT, more in automation, SaaS, etc. all need more in information.Doing well with information is all of fundamental, topical, valuable, urgent, and neglected.Topical? We’re awash in data collected, transmitted, stored, valuable uses, and means of processing.Neglected? We are nearly always from not very good to incompetent and just hopeless to do well with manipulating, exploiting data to get powerful, valuable information.Here’s a core explanatory point: Manipulations of data are necessarily mathematically something, understood or not, powerful and valuable or not. For more powerful, valuable manipulations, proceed mathematically, in particular, with what is by far the most valuable means of thinking in all of civilization, mathematical proof.So, the core reason for the neglect is that only a very tiny fraction of the population is good at the math and how to apply it to say how to manipulate the data to create more powerful, valuable information.Simple.Did I mention, not very good to incompetent and just hopeless to do well with manipulating, exploiting data to get powerful, valuable information?So there’s not much competition. Moreover, Sand Hill Road can evaluate a marketing plan or a sales organization, even programming skills, but has no, none, nada, not even as much as zip, zilch, zero, ability to evaluate work in math and doesn’t care. So, big need, essentially no competition, big bucks.As in the book and movie The Big Short, nearly everyone was really slow to see the disaster coming to the mortgage backed bond market and associated derivatives from the end of the initial teaser rates on home loans. All that was needed was just to LOOK, and they REFUSED to do that and even REFUSED to pay attention to details from a few people who did LOOK. And when plenty of people caught on to the short opportunity, it was fairly easy to know what to do.In comparison, for the math, it’s much harder and takes much longer: Need about four years for each of (1) a severe pure math undergraduate math major, (2) a pure/applied math Ph.D., (3) abilities with the relevant computing, and (4) some experience making applications, So, if people were to believe me now, I wouldn’t have much competition for at least 16 years.But no one will believe me short of my being worth $10+ billion and, say, holding a big party on a 200′ yacht in Long Island Sound. Back to it!

As a company trying to raise a smaller amount – this is painfully obvious. Thanks to firms like USV who still support the “little guys.” Now being profitable doesn’t even count unless it reaches $2MM with 10x growth..In the years before large VC and PE investments, most companies had to start little and grow. Now you had blockchain companies raising millions before a product was developed. Will the trend ever go small again? I don’t see how to go backwards with such large raises of capital in the funds.

When the returns get spanked. Musical chairs only lasts for so long.

Isn’t there a sports analogy for this kind of like ‘getting psyched out by the other teams bravdo?’. Also Ali vs. Frazier and boxing.It seems even in Fred’s post (and DJL’s reply) people are getting freaked out by simply observing the largess of others in the game. Large scary numbers.Having gone through a number of business cycles and observing people in business with ‘big balls’ and their failure (and some success of course) I can only imagine what it must be like for a younger person today and all the large numbers visibility some companies have. As always, blame the messengers for this (and the PR firms).

“Why do the Yankees always win? You can’t take your eyes off the pin stripes” – Frank Abignale (Catch Me if You Can – Movie)”The Yankees win because they have Mickey Mantle. Your gonna get caught (fail) – its a mathematical fact” – CarlI think this is simple math that Fred has talked about many times. VC firms cannot grow their headcount to make the fund increase. So you have fewer people to invest greater amounts of capital. Hence bigger deals with generally less risk. Plus, all of the super successful tech VC firms always get early access to the best, most funded deals. Cracking in from the outside gets harder and harder. People “launching” with $10 or $20 MM more common because they were already “in the club.”

I would say it was Ali’s “rope a dope” strategy.

Let me tell you a story about a guy who was a builder who wanted to build a casino in Atlantic City in the 1980’s. The guys name was Jack Blumenfeld. He had built some nice housing in the city and development.Anyway we did a proposal for him for a new Casino. He called it ‘Carnival Club’ (I have told this story before here at AVC). It was going to be a playground for not only adults but for children.I looked at what we were doing for him and said immediately ‘Oh you aren’t going to do this ‘Carnival Club’ this is just what you are proposing. So you will get money and attract interest and not be compared as another ‘me to’ Casino’. (The gist, not the words as always). He said ‘Exactly… exactly what we are doing’. Was the hook that grabbed them.The point is I think it’s like anything else in selling. If someone is going to hold something against you (that you feel they shouldn’t) then it’s up to you to make it more appealing to them so they will give you what you want. This is not to say you should lie etc that is not what I am saying. However if the investment firms don’t want your small thing you are doing then maybe hook them with something that will make it seem like the big oppty that they are looking for.That said I find it hard to believe that there are not a ton of firms that want to take on a small investment that are unknowns.

This is effective but the epitome of short term thinking.Did Jack get funded? Did he get the casino built?SPAC’s are the same thing. We are raising $ to buy businesses in this area. But 50% of them don’t do that.It works but its hard to do twice.

I don’t think it matters if Jack got funded or not. The fact is Jack got an audience and got consideration. That is the important thing. Without that the idea goes nowhere. Kind of like looks with a woman or money with a man. Does not seal the deal but gets you in the ring for the fight. Can it be overcome? Sure but why?Look at Wework (now has some issues). Better to be thought a fool than to open your mouth and remove all doubt. Wework is a playground (coincidentally) for startups. Imagine where they’d be if they pitched it as ‘just a better Regus’. If they fail at least they are in the game.SPAC’s are the same thing. We are raising $ to buy businesses in this area. But 50% of them don’t do that.Talk more about that if you can. That sounds interesting.

.WeWork is getting into Never-Never Land.JLMwww.themusingsofthebigredca…

With business metrics like Community EBITDA, how could you not throw all of your money in the WeWork basket?

Exactly. Investment firms make investments that fit a certain criteria. This criteria is often defined in restrictive language (e.g. value-add, exponential growth, vertically integrated). What I’ve seen this to mean is that the investors will ignore investment opportunities described with synonyms of their key words so it’s up to you to appropriately represent your company in their language to the best of your ability.

Get profitable and go to a bank.

HA! Welcome to Dodd Frank. They want your first born, 5 years of financial statements and personal financial guarantees. Then there is nothing available for “Series A”. Not a viable option in Tech.

Personal guarantees are a joke.

India National language Hindi – English. Move before the world truly is a village not like your reinventing the wheelhttps://www.bloomberg.com/n…

people should do what they are great at.often that intersects with synergistic markets.i agree with you in general and also believe that you need to follow your gut.

But if what your great at either doesn’t work anymore or has moved along it doesn’t make sense to do what your great at. This is where it gets really really really hard

oh so very true.that is why a while back i rejected ‘do what you love’ with ‘do what you are great at’ which is an interesting discussion in its own right.but this idea of relevance is really an important one we all face especially as our histories and experiences get deeper and broader and the future more unpredictable.i’ve used meditation and especially the concept of beginners mind to help me get in the moment and to be open, then get more flexible at dealing with how experience and wisdom relate to a new unfolding reality.addressed that here:Beginner’s Mind—a tool for calibrating relevance in daily life http://arnoldwaldstein.com/…also for me, this reshuffling of focus to get myself ready to add value insuring that my mental and physical capacity is tuned to be open and ready, has honed my personal strengths.it appears to be working for me.i’m hearing yes a lot more often and running after new experiences to stretch myself professionally even at this point in my career.addressed that in part here:Thoughts I’m taking into 2019 http://arnoldwaldstein.com/…enjoy new york. cold and breezy and beautiful here today.

Focus on what you are great at = focus on adding the most value to other person = focus on helping the customer/client the mostVersus:Focus on what you love = focus on adding the most value to your own life = can only help others in a limited wayYou’ve made the movie star to human being move. Pretty rare.Bravo.

.If you are planning a trip to the pay window, make sure there is a market for what you love, are great at.I loved building sleek tall buildings. Market moved away from it. Numbers were tight.Pivoted to renovating 1900-1920s mid rises. I was in for half of a new building and getting 85% of new building rents.ROI was 2X new buildings at the fat part of the market rate rents.At first I wanted that groundbreaking, grand opening ego enriching mojo, but I learned to love the numbers.I rechanneled my instincts.Business is not a psychiatrists couch. You don’t get to do what “feels” like fun. You have to adult some of this stuff.Pay window — it is a powerful force of attraction. Do not fight it.JLMwww.thmusingsofthebigredcar…

‘You have to adult some of this stuff.’Sounds like a snippet of father to son/daughter lingo.Agree +1000.

.Favorite Son has spit the bit on investment banking, starting a political consulting firm in Charlotte. Where did that come from?My Perfect Daughter, co-founder of Weezie Towels in NYC/Savannah.www.weezietowels.comYeah, they may have both heard that a time or two.Very proud of the little assassins. Both fairly adult.JLMwww.themusingsofthebigredca…

“Liz and Lindsey have spent an unhealthy amount of time thinking about towels, so that you can finally own towels you love.”Love it. Congrats to her.

https://uploads.disquscdn.c…Second generation “towel time” heiress, My Perfect Granddaughter.”Tell me what I need to do to put you in a set of monogrammed bath sheets?” If only she could talk. She’s one in two more days.JLMwww.themusingsofthebigredca…

Political consulting? Steely.

.Kid will be in Congress in 5 years.Knows the issues better than me.IBanker work ethic.Has Beto charisma.Worked on the McCain campaign.He’s 33.JLMwww.themusingsofthebigredca…

You can [also] learn to love something you’re good at hence the expression a labor of love. [Conversely,] you may not ever be good enough at something you love [to earn money it]. There’s a certain amount of that in successful relationships.I like to tell people that I want to be a professional tennis player when I grow up. In the mean time, I need to make money.[edits in brackets]

That is not where I am going with this for me but each to their own obviously.

I realize I left out a portion of my comment that may be relevant to my response and your response, which I added above in brackets. Maybe I haven’t read enough of your writing but, per your responses to me, I have consistently misread you.

.Before one follows their gut, they have to grade it.Sometimes, one’s gut reactions suck and you have to train yourself out of following it and rely more upon coldhearted, detailed analysis.Perfectly fine to get a second opinion from your gut, but as a sole source, that hungry bastard can lead you astray.Don’t get me wrong, there are plenty of things in life that you can follow the “signals” — boy comes to pick your daughter up in an El Camino with an ice chest, tatted up, nose piercing, shaved head, a ring on every finger, and unemployed? Pass.JLMwww.themusingsofthebigredca…

“Moving upstream to invest in more mature companies, larger rounds” is an ordinary evolution in the VC (whether wise or not is debatable). What is extraordinary is the effect of Softbank et. al. skewing the data with monster rounds. If you strip out just Softbank, then total deals would go down slightly but total dollars would drop precipitously. Your overall premise likely still holds, but this would provide a more insightful base for discussion.

Bet against the big funds, they seem a bit odd don’t they?

Shameless self-promotion here, but I took a deeper look at this trends back in Octoberhttp://www.ianhathaway.org/…And just today, added this (time to exit taking longer; well known already but details it)http://www.ianhathaway.org/…

Ian Hathaway:The following is a question?Your shame-less plug article you wrote on “Early-Stage Valuation MultiplesAre coming way down”. What does it mean. Dated October 30, 2018 actually thought before realizing the date if you referenced Axios Kia Kokalitcheva Pro Rata Jan 9, 2019 article.We now wonder if your article was being referenced but not credited. We just found the similarities strange.Ian great article getting ahead of the herd. We are providing proper source and credit where is due. To you!Just must have been the reports from PwC-CBInsights and Crunchbase of 2018 VC investment activity which is promoting many blogs to visit the data and topic.Captain Obvious!#UNEQUIVOCALLYUNAPOLOGETICALLYINDEPENDENT

The future is West. Why not bring on an Israeli or Chinese associate ?

I see a parallel with the rest of the buy side. Happened with mutual funds first, hedge funds, PE, now VC. Size is the enemy of performance, but not of revenue when you’re charging 2&20. The problem for LPs is that the GP starts investing for the 2 instead of the 20.Kudos to USV for staying small and continuing, I think, to invest for the 20. You do right by your LPs, and you also foster a healthier startup ecosystem and plant the seeds for a healthier overall economy.

Fred is lucky in the sense that he had a bad experience with his first firm (growing to large I think 25 people?) which he has said led to a deliberate plan for USV to not get large and (to him) unmanageable.

Many/most institutional LPs, and I qualify here, see team size as a sign of stability and depth ie goodness. In reality, that more often leads to too many cooks in the kitchen and infighting. Plus you dilute the impact of the real moneymakers by giving them a smaller share of the capital base and make them worry about managing people. You also pervert your funnel by relying on the younger folks to “screen” deals.No, smaller is better. Harder, but better.

Most ‘smaller’ businesses are getting trounced by the large business (other than niche of course) but also with professional firms law/accounting/physician. And to your point you get wet behind the ears newly hired vetting deals (or handling clients). But that is the direction of business and I am not seeing any way that it will be different. Also with healthcare.But let’s take it a step further. What ever amount of money you are deploying now as an LP, let’s say you now have 10 or 20x as much to deploy. Then what do you do? You most likely don’t have the time or staff (and good staff) to go with a bunch of USV’s, do you? You will end up ‘satisficing’ because you have to. Right?Also to your point (and Fred’s) this:you also foster a healthier startup ecosystem and plant the seeds for a healthier overall economyThat is a nice goal but honestly is it really your business to take a hit on return because of that (which is a shared problem and not your specific problem).If I have an investment advisor who I want to earn money for me I quite frankly don’t care about anything other than the money that I will make now and certainly not take a hit on returns because of some shared responsibility. I am sure it’s easy for people to say the right thing and appear to be sensitive to other things and correct but honestly that’s easy when it’s not coming out of your pocket. And you will never get the ‘group’ of investors to share that view (as a group) either.

Returns are hard to predict, positive externalities, like fostering a healthier economy, I think less so. But that’s another topic and more of a philosophical one.Your comment that big business is eating small may be true at the global level over the relatively short term, but not for skill-based industries. If you’re supplying a commodity product or service, sure there are economies of scale. If you’re a designer or a plastic surgeon or an engineer or a chef or composer or investor, bigger is not better. When being best matters, not just being cheapest, small is good.Investing $50bn is much harder than investing $1bn as you point out. So why would you expect that to not hold true for USV vs Softbank?

Not saying bigger is better usually it’s not better. I am saying they are getting eaten alive by big. That is what I am saying.I am a small landlord (as one thing I do among many things; diversification). I am no JLM (a commenter at AVC) with thousands of units. No question I am a good landlord vs a big player. Better for the tenant and what matters to them. Not in terms of scale and profitability given no leverage at all.Investing $50bn is much harder than investing $1bn as you point out. So why would you expect that to not hold true for USV vs Softbank?Not my area of expertise. However I think it’s hard to avoid that most success in VC seems to come from taking a large amount of calculated gambles. You have to understand that to most of us just watching from the outside lot’s of the investments look truly foolish by traditional business evaluation. I say that as someone who has made money every single year since graduating college (a long long time ago) and can’t afford to be wrong or make any mistakes because my money is on the line. However if I could afford to lose money and I could afford to take gambles (with other people’s money) no question I would take on more risk in terms of ideas.

The same thing goes for creative or engineering teams.

damn jms, you stole my thunder 🙂 was about to make the same point. The biggest funds might be closer to $100- $200 million per partner (so $2-4 million revenue) vs $25-100 million for partner AUM for funds likes fred (and even smaller ones – which equals $500k-2M). Obviously the expense has to cover salaries, travel, office, legal etc so its not like the partner gets the whole bit, but it is staggering to think the difference and incentives partners have to manage more money.One point, however, is also that LPs are obviously investing a lot more money into VC as an asset class. While there are time lag effects, if $96 billion is invested per year over a decade, roughly $96 billion a year must be invested in VC funds over the same decade. Additonally, more corporate dollars and investment companies (Fidelity etc) distort the number somewhat.I guess the point is that LPs probably don’t mind that much because they need to (or believe) simply deploy more money into VC as an asset class. PE is something like $3-4 trillion as an asset class globally and VC is around $500 billion as an asset class (rough numbers, and also VC is often / usually classified as a subclass of the total amount in PE).Last factor is a good portion (maybe even most of the increase?) is coming from companies raising series C,D, E rounds at multi billion dollar valuations like UBER, LYFT, PALINATR, etc, which would have gone public just a decade ago. So much of those dollars are now captured.Biggest point is its not actually that surprising all this is happening, hopefully i helped illustrate other dynamics that make it so

.LPs are investing more into the asset class because the funds they have under management are growing.If you are the Texas Teachers Retirement System, every month more $$$ flows into the system.That means if you have a 2.5% VC asset allocation, then you have more money to invest.Simple math.With money flowing out of the stock market, alternative investment opportunities will get some spotlight time.JLMwww.themusingsofthebigredca…

A longer duration decline in public equities will cause institutional funds to rebalance and pull money from PE (includes VC). This should cause a price correction across from Seed-D.

yep definitely larger pension funds leads them to puttiing more into vc

I would point to investment bank consolidation in the late 90s/early 00s as a cause here. The hurdle to IPO is much higher because Goldman doesn’t care about a $10M IPO, so capital must be raised in the private markets as you point out.LPs are, of course, happy to oblige. Investors as a group are almost always backward looking and prone to a host of other behavioral mistakes. Were it not for the huge portion of funding going to a small number of later stage companies, I’d say LPs over-allocating to VC would be great for the country/economy long term even if, as expected, most of those investments don’t work out. Plus, retail investors miss out on the opportunity to invest in high growth small cap companies.Trying to figure out the long term ramifications is far too hard for me. I’ll punt on that for someone smarter and leave it at small is good.

I’m curious how things would look if Softbank were taken out of the picture. My sense is that the trend probably remains, but is far less pronounced.

Probably, but the trend is your friend.internet is a mature market.

CONTRIBUTORS:It appears that the savvy investors are not so savvy when reading the tea leafs.One of the many reason for the concentration of larger funding and lesser funding is smaller bets is one company SOFTBANK! Period.The herd is just intimating the leader. When you are never leading you are always following and being dictated too.The tea leafs read there is a bubble a coming. When no one knows. But when it does come there will be many new haircuts to show your co-workers, family and friends.Captain Obvious!#UNEQUIVOCALLYUNAPOLOGETICALLYINDEPENDENT

And then people will starting making tea out of hair.

Do you think USV still resembles a boutique?I recall you liked to say that.