More S1 Fun

We are now seeing a wave of longtime private companies coming public and with that we are getting data on usage, financial performance, and a host of other issues that is very useful market data.

I spent some time looking at Pinterest’s S1 today. They filed it a week or two ago.

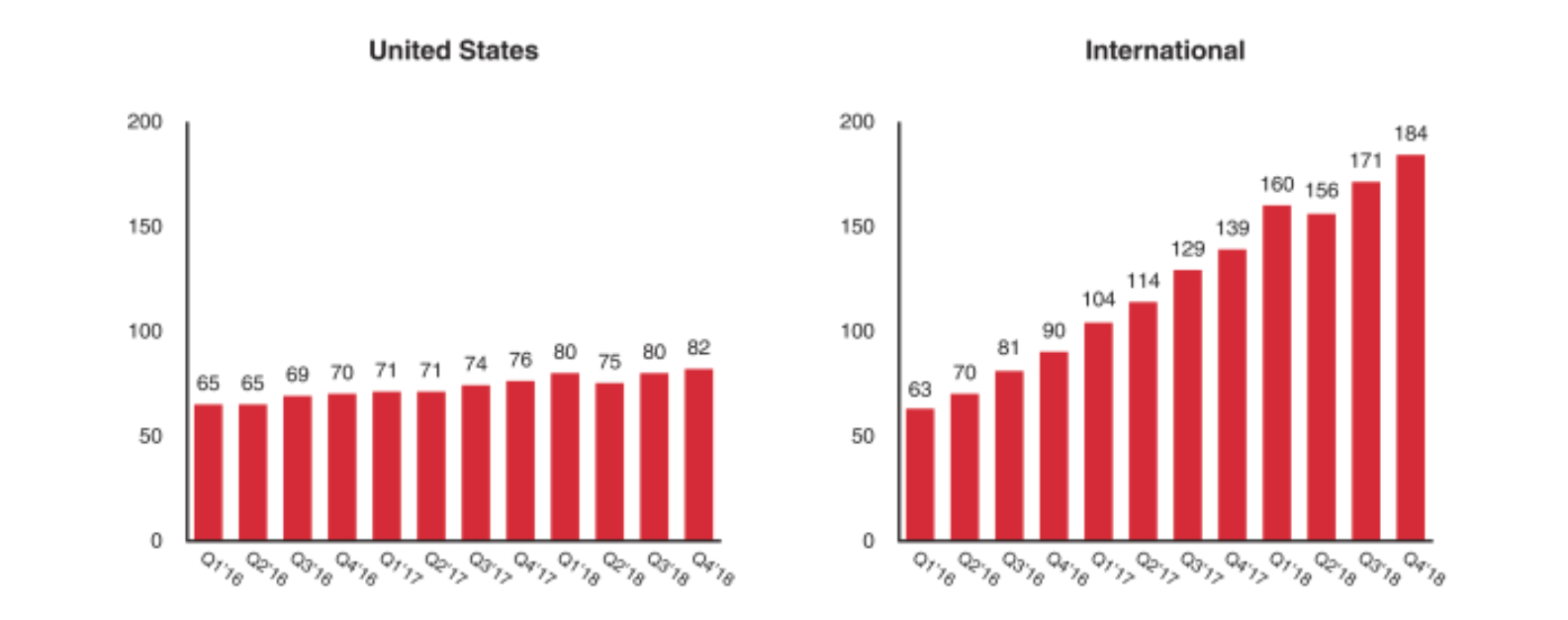

I found this chart of user growth quite interesting:

That shows monthly active users in the US and International over the last few years on a quarterly basis.

Pinterest is rapidly growing its user base outside of the US but usage in the US has stalled out.

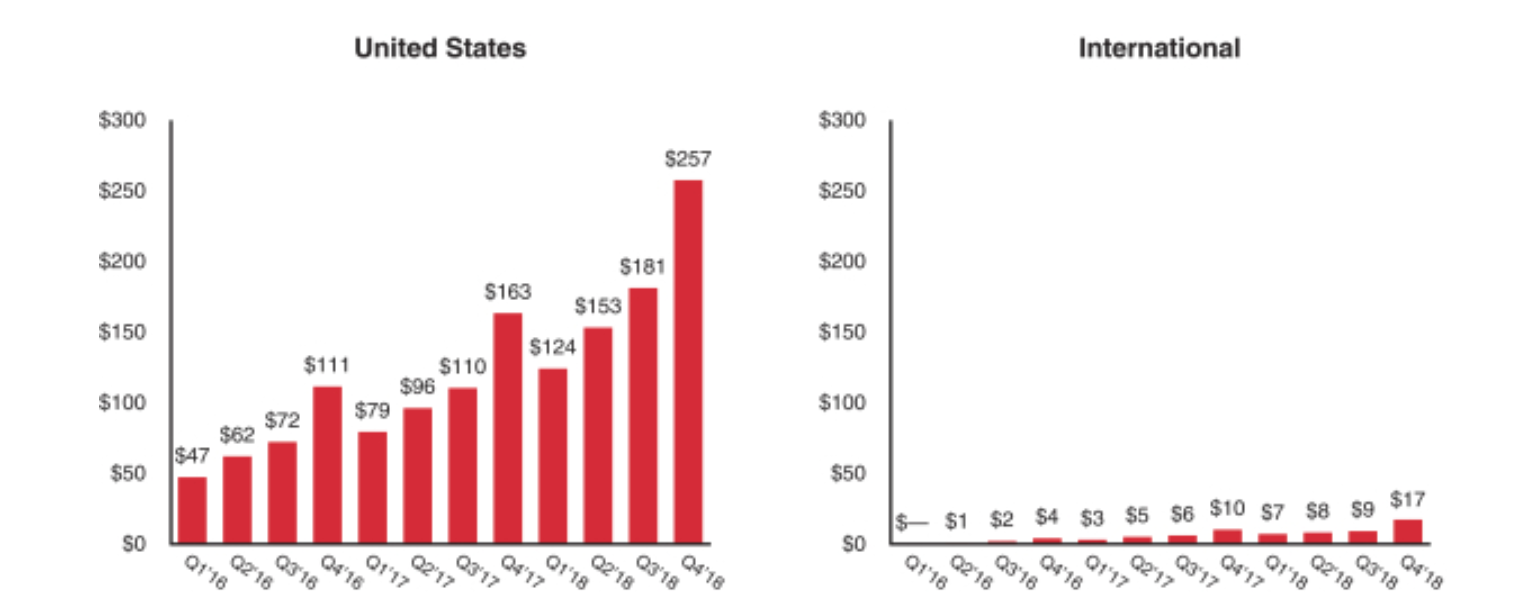

This chart, also from the S1, shows revenue growth in the US and Internationally:

So what you can see is that Pinterest has been growing its US revenues rapidly but not its US user base. And on the other hand, Pinterest has been growing its International user base but its International revenue is still nascent.

So the question is whether Pinterest will be able to monetize its rapidly expanding international user base.

That is the kind of insight you can get from reading these S1s. I find them fascinating and try to read them when they come out.

I don’t plan to buy Lyft or Pinterest when they come public. That’s not really my thing. And I don’t have an opinion on whether they are attractive investments or not. But I do think we can learn a lot about these businesses from reading S1s and that can help us with the investments we do have.

Comments (Archived):

“And I don’t have an opinion on whether they are attractive investments or not”- oh, please. of course you do. you live and breath this, you have an opinion on them whether you want to or not!

I should have added “for public consumption” to that statement

yup. i thought about adding that you just chose not to share it – but thought a tad aggressive.

Fred – at a Macro level (not necessarily for Pinterest) / Investor level – rapidly growing US revenues with marginal traffic; fast international traffic with modest revenue. Is that exciting? Or scary or both??On the domestic side – if the traffic has slowed but the revenues are cranking, are you okay with that? You could argue Pinterest and even Twitter would be in these camps per se. Even Facebook is in this camp to some degree.On the international side – we know that international traffic (at least for the next 3-5, 10 years) will be worth some sort of fraction compared to domestic traffic, particularly with respect to advertising based businesses … do you like seeing that traffic growth with the potential to one day figure out that revenue source, or its nice but its far from being meaningful amount of revenue that its not bad but its not really driving results for a while that its hard to put too much weight there.Thoughts on the above from the perspective of an investor like yourself. And you don’t have to comment on specific examples if you don’t want to but it would be good to understand how you see these things.

Agree.Been looking at Zoom.Been a user for a long time, and my buddy Bill Tai was their first seed investor.So interesting.Entered a crowded commoditized market. Dug deep and developed some difference making tech to drive it.Built a really kick ass product.Brilliant positioning aligning themselves with the massive change in decentralized remote work force with examples of huge successful companies using them.Execute and execute and execute.Great fundamentals.Really hope they have a strong offering.Learned a ton by looking at them.

Zoom is an incredible product. We run our business on it

What is it?

Videoconferencing app

Duh, of course. Have heard the ads but never used it.Hard to believe they could make a business out of something that is basically free. Must be multi user optimized….

great product.great business.

Compared Zoom to GoToMeeting recently. Use case is meetings and training for clients For people who are not tech savvy, GTM is much simpler.

each to their own of course.everyone used gtm forever then the majority of large projects i’m working on used zoom–and the evolution happened.the vast majority of my work touches the tech and environmental and game worlds. no issues cross any of them.

Not free. They compete with gotomeeting and webex. Worth paying for the ease of use for clients.

Zoom has some form or tier of freemium, right? I know because I’ve used it for calls with consulting and training clients, a few of whom suggested it to me. Has worked well for the times I’ve tried it. Only one issue I find is that it seems you cannot increase the font size in the text chat window. Maybe the feature is there in the paid version.

Have had lots of colleagues recommend zoom instead of Slack’s neutered version of ScreenHero they integrated for remote pair programming. It works great. Whenever I connect to a conference call meeting with folks at tech or tech adjacent firms (IDEO, Pivotal, etc.) they’re all using Zoom. Here in government we’re stuck with WebEx…

Similar to my experience and a true living example of network effect.I like to see great products and hard working teams win.It doesn’t always happen that way.Thanks for your comment.

The 50% revenue spike every Q4 really stands out to me. Is Pinterest really that seasonal as a destination? I don’t use it so don’t know, perhaps one of you does?

Seems very plausible to me, Pinterest is great for holiday design ideas and gift discovery

I’m curious on what constitutes an active user? Is it a consistent method across different companies ?

A long time ago, Fred posted on 30/30/10 for social networks. Of total signups, 30% use it once a month, 30% of that number use it once a week, 10% of that number use it every day. That means you need millions and millions of signups.

Thank you, this helps

I found this twitter bot which is quite useful for those interested in following S1 filings: https://twitter.com/newstoc…

Q1 2019 revenues will fall from Q4 2018’s ATH, and so is this listing an attractive proposition?

Pinterest gets a grade of useless, worthless flat F in graph drawing 101 showing that the computer nerds who clicked on Excel or whatever to draw the graphs didn’t understand anything about the data or the purpose of the graph. Instead they fell into the trap of colorful and up and to the right.What’s wrong? (1) The graphs do not mention that the data is on unique monthly users. (2) The vertical axes have no labels and no units. E.g., on one graph, one of the bars for one of the quarters has at the top 71. So, for that quarter there were 71 unique monthly users? That’s what the graph says, 71. They meant 7100, 71,000, 710,000, …, or some such? No telling. (3) This nonsense is bad enough one graph at a time, but when comparing graphs, as Fred did, we NEED to know that the scales and units, e.g., dollars, are the same across the separate graphs.Did I mention grade F?

@fredwilson:disqus International revenues nascent, yes. But also, revenues doubled in the final quarter of 2018, over each of previous two quarters. Could mean many things, but curious your take if any.

75%+ of Pinterest users are women – the largest markets (by growth) is India – if there were ever a case for diversity of opinions on a company, this is it!

My experience is Pinterest is used mostly by females.

I would wait for the options to come & short them. I don’t use either of these products, nor do I think anyone cares about the numbers generally. As bonds keep rising, it seems like the market is thinking the economy could start slowing down any day now, but then again I seem to be proven wrong all the time.

I also did an analysis of their S-1 and made a short Youtube video about it (link below). The tl;dr is that I feel their user base might have more spending power (thus higher LTV), but given current user growth and MAUs, the $12bn private valuation doesn’t seem to be in line with the public company multiples. This is just based on some quick back-of-the-envelope calculations though, would need to dig deeper to make a more qualified assessment.Here’s the link to the Youtube video:https://youtu.be/Dphtaws-0zE