The AVC comments has been experiencing a wave of comment spam that has largely been replies to legit comments. I appreciate the community for flagging it and our moderators for nuking it. Keeping the comments free from spam is important to me but not an easy chore.

One idea I have, which I don’t even know if is possible in Disqus, is the idea of limiting replies to longstanding community members who are registered with Disqus and have high reputation scores.

What this will do is eliminate the reply spam, but will also make it impossible for new commenters to reply. They will still be able to leave a comment.

When early stage investors make an equity (angel, seed, Srs A, Srs B) investment, they typically negotiate for something called a pro-rata right which gives them the right to maintain their ownership in the company by investing in future rounds on the same terms as new investors.

I have written about the pro-rata right a bunch here at AVC. I think it is one of the most important things that early stage investors get from their investments. Obviously the ownership an investor gets is the most important thing, but the ability to maintain it by making additional investments is also very valuable and can be the source of out-performance of an early stage portfolio (against whatever benchmark one might be using).

At USV, we value the pro-rata right and exercise it very frequently. We often will make five, six, or seven investments in a company between when we make our initial investment and when we make our final investment. We even have a follow-on fund called the Opportunity Fund, that allows us to take our pro-rata in companies that continue to raise privately and delay going public. Our Opportunity Fund will also make some investments in companies that aren’t currently in our portfolio. But a large part of our Opportunity Fund thesis is about maintaining ownership via our pro-rata rights.

In the last ten or so years, companies, lawyers, boards, management teams, founders, and in particular late stage investors have been disrespecting the pro-rata right by asking early stage VCs to cut back or waive their pro-rata rights in later stage financings. This can happen as early as Series B (and happens to angel and seed investors in Series A rounds), but it is even more common in the later stage rounds like Series C and beyond.

I think this is bad behavior as it disrepects the early and critical capital that angels, seed investors, and early stage VCs put into the business to allow it to get to where it is. If the company agrees to a pro-rata right in an early round, it really ought to commit to live up to that bargain. But increasingly nobody does that and it is a black mark on the sector in my view. We make commitments knowing that we don’t plan on living up to them. It is very unfortunate.

The reason this happens is that allocations get tight in later stage rounds, particularly where the company is doing well and everyone wants to get into the round. The new investors, including the investor that is leading the round, will almost always have a minimum amount of ownership they want to get to in the round and the math tends to work out that the only way to get there is to cut back the early investor’s pro-rata rights.

Sometimes the way the gap is filled is by creating secondary for founders, early employees, and early investors. That can work and is sometimes good for everyone involved. That “trick” has been the saving grace on this issue over the last few years.

But I believe we are at a crossroads on this issue and I am wondering if early stage investors need to put more teeth into our pro-rata rights to insure they are honored. What if a company that was unable to offer a full pro-rata right to an early stage investor in a later round was forced to go back and change the price of an earlier round to make it up to the early stage investor? Or what if an early stage investor got warrants at the new round price to make up for an inability to honor the pro-rata right?

These are just two suggestions I came up with in a few seconds of thinking about it. But I would really like to force early stage companies, their lawyers, and their boards to think clearly and carefully about the pro-rata right when granting it. The current practice seems like “we can give this because we always get away with not honoring it down the road” and frankly that sucks.

The most common caller on my Android phone is Scam Likely. I am sure that most of you are in a similar situation.

Last week we were driving and two calls came into The Gotham Gal’s phone which was bluetoothed into our car and she declined both. I asked her why she did that. She said they were likely robo calls. I told her that they looked to be legit numbers to me. Later on she found out that both calls were from people she knew, but for some reason those names were not showing up on the car dash and so she declined the calls.

That led to a discussion of why spam filtering for email has gotten so good and robocall filtering for phone calls is still not great. I brought up the great work the email industry has done over the last twenty years with email signing protocols like DKIM and SPF, and the email industry’s adoption of DMARC protocol which operationalizes DKIM and SPF. We decided that the telephony industry needs similar solutions.

Well, it turns out that the telephony industry is working on them.

Jeff Lawson, founder and CEO of Twilio, a company that was a USV portfolio company and which The Gotham Gal and I are still large shareholders in, is writing a series of blog posts about how the telephony industry can fix the robo call problem.

In Jeff’s first post in the series, he explains that the telephony industry is developing their own versions of DKIM and SPF and DMARC:

Some very smart people have been working on new ways of cryptographically signing calls – a digital signature – proving ownership of a phone number before the call is initiated. One example of this is a new protocol called STIR/SHAKEN, which the communications ecosystem is working on now. Before any authentication method can be impactful at scale, it needs to be adopted by a broad swath of the ecosystem. Twilio is fully committed to efforts to authenticate calls so the identity of callers can be proven, and it looks like STIR/SHAKEN is a good candidate to do just that.

In Jeff’s next post, he will address the role that identity (of the caller and the recipient) and reputation will play in solving the robo call epidemic. I look forward to reading it.

I expect we will see IPOs from big names like Uber/Lyft/Slack, although I also expect those deals will get priced well below the lofty expectations they have in mind right now. Some of that will be because of weak equity markets in the US, but it is also true that most of the IPOs in 2018 also priced below the lofty “going in” expectations of founders, managers, boards, and their bankers. The public markets have been much more sanguine about value than the late stage private markets for a long time now.

When I see an IPO price range, I like to go look at the S1 that the issuer has filed with the SEC prior to the road show. Here is Lyft’s S1.

Here are the things I like to look for in a S1:

1/ The total shares outstanding. You can go to the table of contents of the S1 and look for the section called “Description Of Capital Stock”. In Lyft’s S1, it says there are ~240mm shares of Class A common stock plus some amount of Class B common that is not yet detailed. The Bloomberg article I linked to above says the company is going to sell 30.8mm shares at $62 to $68 per share. So there will be at least 270mm shares outstanding plus the Class B shares. The Bloomberg folks seem to be using a post deal share count of 288mm share so that is close enough. You get to fully diluted post deal valuation by multiplying the share count (288mm) by the range ($62/share to $68/share).

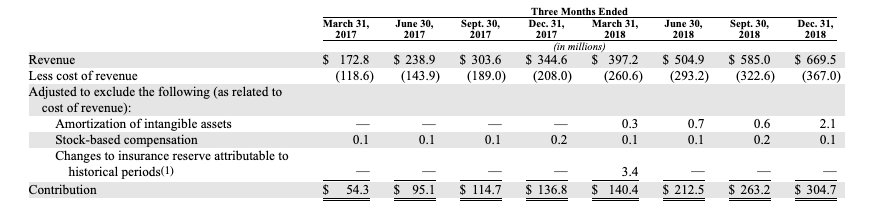

2/ Revenues and earnings/losses. You can go to the table of contents of the S1 and look for the section called “Selected Consolidated Financial And Other Data” and you will find the audited financial data. I like to find the quarterly numbers because that will give you a good idea of current growth rates. These are the numbers for Lyft:

As you can see the quarterly revenues are growing at roughly $80mm a quarter so a back of the envelope guess on revenues for 2019 are [$750mm, $830mm, $910mm, $990mm] for a total of ~$3.5bn, up from $2.1bn in 2018 (yoy growth of 65%).

You can also see that the contribution (net of cost of goods sold) has been about 45% over the past few quarters so if that ratio holds in 2019, there would be contribution of roughly $1.6bn in 2019.

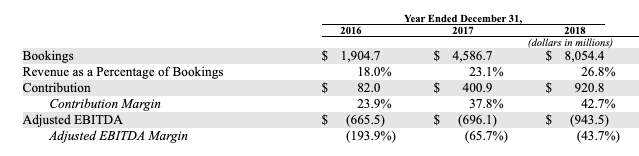

For the operating costs, you can look at the difference between contribution and EBITDA, which you can see here:

Lyft spent ~$1.85bn on opex in 2019 ($921mm of contribution plus $943mm of EBITDA losses). That number grew from $1.1bn in 2017. I would expect Lyft’s operating expenses to be at least $2.25bn to $2.5bn in 2019.

Which gets you to this possible P&L for 2019:

Revenues – $3.5bn

Gross Margin – $1.6bn

EBITDA (loss) – $600mm to $900mm

3/ Valuation Ratios:

At the mid-point of the offering range $18bn, the price to revenue multiple is roughly 5x (18/3.5) and the multiple of gross margin (what Lyft keeps after paying significant COGS) is roughly 11x (18/1.6).

4/ Time to cash flow breakeven. This is harder because you have to make some assumptions about growth rates beyond 2019 and opex growth rates. But if Lyft can grow revenues at 60% per annum for a few more years and keep opex growth rates to 25-30% per annum, then it could get profitable by sometime in 2021. This suggests that the $2bn it is raising may be sufficient to get profitable, but it will be close.

So what does this mean for other late stage high growth high flyers?

To me it says if you have company focused on a big opportunity (like transportation) that is growing at north of 60% per year it is worth in the range of 10-12x net revenues to wall street right now. Because Lyft only keeps about 45% of its revenues after very high COGS, that works out to be 5x revenues.

Many late stage private companies are getting financed at valuation ratios in excess of this so they will have to grow into their eventual public market valuations. But that has been the case for quite a while now as the late stage private markets continue to pay higher prices for high growth companies than the public markets do.

Many people who follow tech know that Spotify has filed a complaint with the European Commission regarding the challenges that Spotify has doing business in the iOS app store.

I am very sympathetic to Spotify’s complaint. In my post last week on The Warren Breakup Plan, I wrote:

The mobile app stores, in particular, have always seemed to me to be a constraint on innovation vs a contributor to it.

Spotify has a huge user base and brings in billions of dollars of revenues every year but it has a challenging business model. Let’s say that 70cents of every dollar they bring in goes to labels and artists. That seems fair given that the artists are the ones producing the content we listen to on Spotify. But if they also have to share 30cents of every dollar with Apple, that really does not leave them much money to build and maintain their software, market to new users, pay for servers and bandwidth, and more.

You might say “well that’s what they signed up for” and you would be right except that their number one competitor is Apple. So their number one competitor does not pay the 30% app store fee, meaning that they have a competitive advantage.

We see this with our portfolio companies a fair bit too. Apple has complete control over what gets into their app stores and what does not. And the process can be arbitrary and frustrating. But that is how it works and our portfolio companies are reluctant to make any noises publicly for fear of making their situation with Apple even worse.

I am not a fan of Warren’s idea of breaking up companies like Apple.

I like my partner Albert’s ideas better which he expressed in a tweet last week:

A better set of policies to restore competition in the digital age would be (1) consumer right to API access (2) consumer right to side load apps (3) restored ability for small companies to go public / sensible regulation of crypto currencies. https://t.co/4bOFTnZ5NK

If it was the law of the land that any company could side load any application onto the iPhone or any iOS device, including third party app stores, we would have a much more competitive market with a lot more innovation, and Spotify would not have to go to the European Commission to deal with this nonsense.

While we wait for the blockchain/crypto technology to scale to the point where it can be the foundation of mainstream consumer applications (games, social media, e-commerce, etc), there is a sector where scalability is a little less important and where blockchain/crypto is starting to show some real signs of life.

In the crypto space, it is called Decentralized Finance, or DeFi for short. It includes, of course, all of the ICO activity largely built on top of Ethereum and the ERC-20 token. But it also includes thinks like Maker which is both a stable coin and a collateralized lending sytem. The collateral for the loans is what stablizes the Maker stablecoin. We also are seeing other lending offerings develop in the DeFi world and we are seeing things like hedging, shorting, derivatives, and more, all built on a decentralized platform where there are no intermediaries, no clearinghouses, and the need for trusted third parties is much less, sometimes not at all.

This makes sense for a number of reasons. While the transaction requirements of financial services applications are not trivial, they are also not as demanding as mainstream consumer applications where millions of users are transacting with each other and the system in real-time.

It is also the case that, unlike many of the new architectures that emerged over the years (mainframe, mini, client-server, web), the blockchain/crypto space has always had money at its core and making money, transacting in money, and everyting that goes along with that has been an early use case and for most people, the driving use case for this technology.

All technologies need early use cases. I do not think DeFi will be the only thing that blockchain/crypto is good for. I think we will see blockchains scale in the next few years to allow mainstream consumer applcations to be built.

But until then, DeFi is a good place to hang out. It uses all of the same technologies, architectures, and value systems that we have come to know and love in crypto. You can learn to build applications, use applications, and generally come up to speed on the sector while serving real customers, building a business, and, hopefully, making money.

Startups are generally not funded by just one investor. They are usually funded by a collection of investors; the angel syndicate, followed by the seed syndicate, followed by the VC syndicate.

This gives the founder the opportunity to gain insights and advice from a group of people versus just one.

I was sitting next to a VC last night who brought up the age old question – operator vs investor? She is a successful early stage investor who has never been an operator.

My answer to her question was “both.”

Yes it is fantastic to have people in the syndicate who have been or maybe still are operators. They will be able to help you with all sorts of management issues.

But it is equally important to have the investor mindset in your syndicate. Investors tend to be very attuned to financial issues like burn rate, when to raise, from whom, etc. They also understand market positioning, strategy, and similar stuff very well.

While you are at it building a diverse investor syndicate, try to get women, minorities, and other forms of diversity into your syndicate.

Treat building an investor syndicate like building a management team. What you want is a lot of differing strengths not a bunch of the same strengths.

I get asked frequently whether it is better to back the team or the product (the “jockey or the horse”).

It is not that simple in my view.

When I think about the big wins we have had over the years, they almost all exhibited a combination of a large market, a great product, and a talented founding team.

Some investors feel that the team doesn’t matter. They believe that you can replace the team if everything else works out. But I don’t think everything else works out if you don’t have a talented founding team.

Some investors feel that product doesn’t matter. They believe that you can pivot into something else if you have a talented founding team. While that is certainly the case, pivots are expensive in terms of capital, time, and focus. I would not choose to go through one given the choice.

And large market is critical. You can build a nice business in a small market, but you can’t build a big business in a small market.

My point is you really need all three, market, product, and team, to get the big wins that the venture capital model requires.

And in terms of finding the best opportunities, I would start with large markets, go searching for teams working in them, and writing checks only when you find talented teams working in large markets who have built excellent products.

Many people in startup land believe that the answer to the challenges around forcing departing employees to exercise vested options is to simply extend the option exercise period to the maximum (ten years) allowed by the IRS.

It certainly is one of the techniques that are available to companies and one that a number of our portfolio companies have adopted. Another option, and one that I prefer, is for a market to develop around financing these option exercises (and the taxes owed) when employees depart.

However, if you are thinking about extending the option exercise period for departing employees, you should understand that it will cost your company something.

Here is why:

Options are worth more than the spread between the strike price (the exercise price) and what the stock is actually worth. They have additional value related to the potential for the stock price to appreciate more over the life of the term of the option.

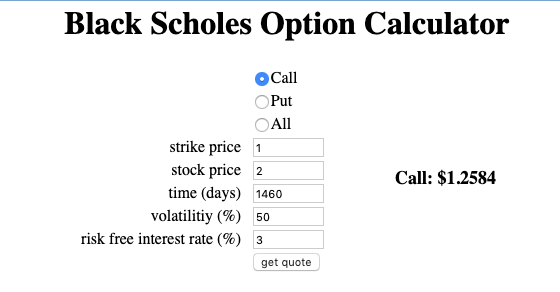

There is a formula that options traders (and companies that issue options) use to value options. It is called the Black-Scholes formula.

If you click on that link, you will quickly realize that the math used in the Black-Scholes formula can be complicated. But fortunately, there is a neat little web app that I frequently use to estimate the value of an option. It is here.

So let’s say that your company is issuing options at $1/share (your 409a) but your most recent financing was done at $2/share. Then a four year stock option is worth roughly $1.25/share.

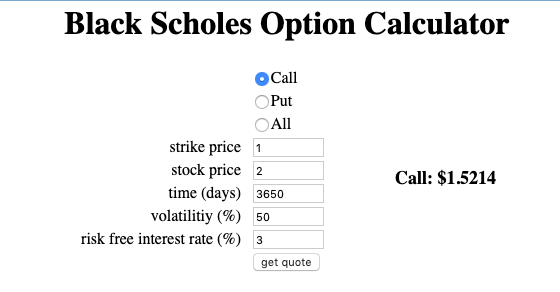

If, on the other hand, you offer a ten year option exercise period to your employees, the value of the option rises to $1.52/share, reflecting the longer period of time that the stock could appreciate over.

That is a 20% increase in the cost of issuing stock options. You could mitigate that by reducing the number of options you issue to incoming employees by 20% but that might make your equity comp offers less attractive to the “market” because incoming employees won’t value the longer exercise periods appropriately.

Stock based compensation costs are real costs even though many in startup land think of options as “free” because they don’t cost cash. The accounting profession has attempted to estimate these costs and companies do put stock based compensation costs on their income statements. If you go with ten year exercise periods instead of four year exercise periods, expect those expenses to go up significantly. Twenty percent is just the amount in my example. It could be larger, possibly as high as fifty percent (or more) if your exercise price is a lot closer to the current value of your stock.

This extra value of a ten year stock option versus a four year option is known as “overhang” by investors. It is the cost of carrying a group of people who have a call option on your stock but don’t have to pay for it for a long period of time. Generally speaking investors don’t like a lot of overhang in a stock.

All of that said, employees are the ones who create value for shareholders. They need to be compensated for that. And I am a fan of both cash compensation and stock based compensation. I like to see the employees of our portfolio companies well compensated in stock. That has a cost and everyone should be well aware of what it is. Longer exercise periods increase that cost. I would rather put more stock in the hands of the employees of our portfolio companies than give them longer exercise periods. But regardless of where one comes out on that tradeoff, it is important to recognize that it is a tradeoff. There are no free lunches, not even in stock option exercise periods.