If you are in or around the Brooklyn Navy Yard and want to get to the East River Ferry, you can have a self driving car take you there.

I did that yesterday:

It’s sort of like a van. There are six passenger seats in the vehicle rand I saw four of them lined up waiting for passengers next to the main gate off Flushing and Cumberland.

There is a driver in the front seat but the van drives itself. That takes some of the excitement factor down a notch. But it increases the comfort factor. I assume the driver can take control of the vehicle and drive it manually if necessary.

It makes a ton of sense that autonomous vehicles would start out in places like the Navy Yard where there is not a lot of vehicle traffic and the map is fairly simple.

If you want a taste of the future go over to the Navy Yard and get a ride. It’s free.

And while you are there check out the amazing new Dock 72 building next to the East River Ferry stop. They are leasing it up now and there are some great office spaces still available there. They have smaller offices for startups. Link here.

A friend of mine told me a story this morning about a time that he said he had the money when he did not and then he went out and found it.

It reminds me of Mark McCormack’s What They Don’t Teach You At Harvard Business School where he tells story after story of signing big deals that he had no ability to pay for and then going out and funding them.

Mark and my friend both knew they could get the money even though they did not actually have it.

When I was in college I needed a job and I found one programming in Fortran. I didn’t know Fortran. I had some cursory knowledge of Basic.

I went for the interview anyway and when they asked me if I knew Fortran, I said “yeah, I’ve done some Fortran programming” and then asked them if I could take the source code home for the weekend.

So they printed out the source code on a dot matrix printer on folds after folds of large format printer paper. I took that pile of paper home and opened it up.

It turned out that the postdoc who had written the Fortran program had literally commented every single line of code.

On one line was the code and on the next line was a comment that said something like “this tells the laser to move to the right by the amount entered.”

I smiled and knew that I could maintain that Fortran program and in the process teach myself the language. And that is what I did and partially paid my way through MIT too.

I am not advocating lying but that is what I did and that is what my friend did. But we lied with the self-confidence that we could pull it off.

There is a fine line between self-confidence and recklessness and I have been able to project the former without landing on the latter in my career. I think you need at least a little bit of the former in business. Without it, you won’t be able to go for it when you need to go for it. And if you don’t go for it, you won’t get it.

In a perfect world, everything about a potential investment will be confidence inducing. The team will be great and reference well. The market will be huge. The technology will be well developed. The price and terms will be attractive.

But the world is not perfect. There will always be things about a potential investment that create heartburn. A term that I have heard used over the years to describe these imperfections is “hair on a deal” as in “there is a lot of hair on that deal.”

A little hair is OK if everything else lines up. A lot of hair is not OK and can be a deal killer.

The news that WeWork has postponed their IPO plans for now is an example of when too much hair gets in the way of a deal.

There are a lot of things to like about WeWork. They have popularized a new form of work space, a new business model for it, and have they have built a global brand around shared workspaces.

I expect the company will eventually get public.

But right now there is too much hair on that deal and all the work they did over the last few weeks to clean it up was not enough, at least for now.

So the lesson for entrepreneurs is that you really need to have your house in order when you go out and raise capital. The more eyebrows you raise with investors, the worse it gets. And hair can get in the way of an otherwise financeable opportunity.

You might ask “why do we need yet another blockchain?” and you would be right to ask that.

The answer is that Dapper has built several games on Ethereum, one of them a top-three smart contract this year (CryptoKitties) and they have found it challenging to build the games they want to create on that platform. They looked around at all of the other options and could not find a blockchain that addressed all of their issues. So they are building Flow.

Flow’s technical architecture balances three priorities: Scaling with Full Composability: Flow improves throughput without breaking up the network shared state. This preserves a developer-friendly environment for applications, making it much easier to write secure and composable code. Speed and Efficiency: Flow is capable of handling the transaction volume needed to support modern consumer applications while consuming a tiny fraction of the computing resources needed by current networks. Decentralized Participation: The security of a decentralized system is directly related to the number of independent participants working to secure the network. Flow supports large numbers of participants with a range of technical and financial commitments, resulting in a system that’s cheap to join while being costly to subvert.

If you are building a game, a collectibles experience, or some other mainstream consumer decentralized application, you should check out Flow. You can do that here.

And if you want to engage with Flow and the Flow community, you can do that here.

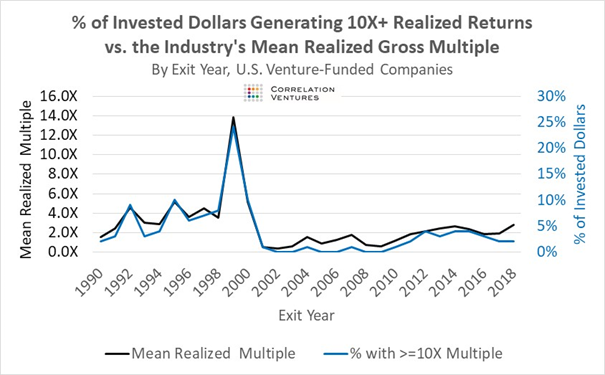

In the Correlation post, they define “hit rate” as:

the percent of invested dollars generating a 10X or greater return

But “hit rate” could be something else. It could be the number of investments in your portfolio that return the fund. It could be the number of seed investments you make that turn into billion-dollar valued businesses. It could be the number of your seed and Series A investments that go public.

My point is that it doesn’t really matter than much how you define hit rate.

What is important is this chart from the Correlation post:

I guess they have a keen eye for correlation at Correlation Ventures. They certainly found it here.

Venture capital returns are highly correlated to a fund’s hit rate.

Or said differently, a fund’s hit rate determines their returns.

I think that is a pretty well-known fact these days with all of the obsession with billion-dollar valued companies, or “whales” as I like to call them.

We know that venture investments result in a power-law distribution of outcomes.

And so one or two companies will determine the returns in a given fund.

Sometimes that is not the case. In our 2004 fund it was five companies, but that is why that fund was so good.

The other interesting thing about that chart is why the hit rates and returns in the venture capital industry have not returned to pre-2000 levels.

I think that is all about the amount of capital in the business now. More capital means more businesses get funded. So even if you have more winners, you don’t see the hit rates move up. The numerator and the denominator have both grown in the hit rate calculations.

Before 2000, the venture capital business was a bit of a cottage industry.

In the last 15 years, VC has become an institutional asset class with the permanence and stature that brings seemingly endless amounts of capital to it.

And so the returns have stabilized in or around the 2-2.5x over ten years number, which produces high teens/low 20s IRRs, which is enough to sustain the sector.

The only thing that I think would take us back to mean multiples of 4x or better would be some sort of massive reduction in the amount of capital coming into the venture capital business. And I don’t see that happening any time soon.

But one thing about the VC business has not changed in all of the years in that chart, which is roughly how long I have been a partner in a venture firm, and that is that your big winners will determine your returns.

USV recently invested in a company called Patch Homes and they are announcing that financing today along with some other important information on their business.

What I’d like to talk about is the bigger idea behind Patch and some other startups out there which is the ability to break up your home equity into pieces and sell some of it while holding onto most of it. I call this fractionalizing home equity.

In the existing home finance world, the only thing you can do with your home equity is borrow against it. And many homeowners do this. It is a big market and helps a lot of homeowners out. But once you borrow against your home equity you have larger monthly mortgage payments to make and many can’t afford to do that. And you need a certain credit score to be able to access the home equity loan market.

What Patch offers instead is to take a piece of your home equity (currently limited to $250k maximum) and sell the upside on it to a investment fund. Note that I said upside. This is effectively a call option on the equity not a full transfer of that equity. That makes things a lot simpler in many of the scenarios that could arise.

There are some great use cases for a partial sale of home equity. One example I like a lot is a family whose children are heading to college and soon will be out of the home. They plan to sell the home when all the kids are gone but don’t want to do that until then. They could sell some of their home equity, help pay for college, and then sell the house after all of the kids have graduated. There are plenty of examples like that where you are in a situation in life where you plan to sell but not just yet and you don’t want to add to your debt load and/or your monthly payments.

And that is why having more home finance options is great. It expands access to capital and that is a core part of the current USV thesis. And we are excited to be working with Patch to help them do that.

We were having breakfast in lower Manhattan that morning before a board meeting. It was the CEO, another board member and me. We were sitting outside in a sidewalk cafe in lower Soho and the plane flew right over us, at a height that was clearly not normal, and banked and slammed right into the first tower.

The CEO knew right away it was a terrorist act and we quickly settled up and headed over to the company’s offices. We told everyone to go home that could go home, and then waited to see how many people would arrive at work. Once we had sent everyone home who could go home, we got everyone who could not go home and started walking uptown to our house in Chelsea. We invited everyone in to our home and went out and got sandwiches and made a buffet lunch.

Nobody did anything but watch TV and call their loved ones, if they could get a call out on the overloaded cell networks.

By evening everyone had made plans for the night or figured out how to get home.

It was a horrible day, one that I certainly will never forget, and one that changed everything in many ways.

But when I look back at it, the ability to take everyone in, feed them, and provide some community and comfort, made that day a lot easier for me and my family. I am grateful for that.

Today Apple is going to announce three new iPhones.

One of them should be a small form factor like the old SE.

Apple discontinued the iPhone SE at the tail end of 2018 and has stated that the next iOS update will not run on the old SE hardware.

I have a number of friends and family members who have the old SE, love the small form factor, and do not want a larger phone in their pockets, purses, and hands.

As a result, these people have been holding onto phones that have gotten a bit old and badly in need of an upgrade.

But more importantly in my view, if Apple wants to tightly control the hardware that iOS can run on (which obviously they do), then they should put a wide enough variety of hardware into the market to support their user base.

It is unlikely that any of my friends and family members are going to move to Android, where there is a wide variety of hardware form factors to choose from. The iOS lockin is very powerful.

So Apple doesn’t need to do this so much for business reasons. But I do think they should do this for other reasons.