The Hit Rate

This simple and short blog post by the folks at Correlation Ventures contains the key to venture capital returns – the hit rate.

In the Correlation post, they define “hit rate” as:

the percent of invested dollars generating a 10X or greater return

But “hit rate” could be something else. It could be the number of investments in your portfolio that return the fund. It could be the number of seed investments you make that turn into billion-dollar valued businesses. It could be the number of your seed and Series A investments that go public.

My point is that it doesn’t really matter than much how you define hit rate.

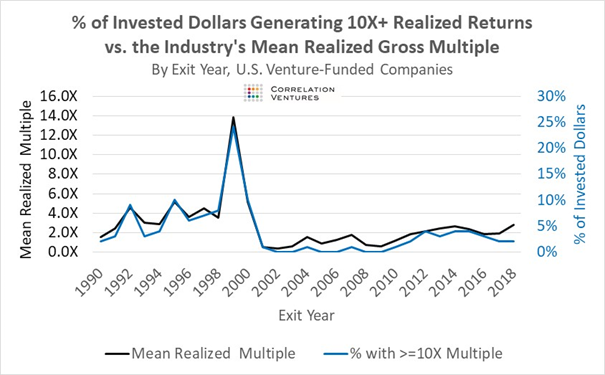

What is important is this chart from the Correlation post:

I guess they have a keen eye for correlation at Correlation Ventures. They certainly found it here.

Venture capital returns are highly correlated to a fund’s hit rate.

Or said differently, a fund’s hit rate determines their returns.

I think that is a pretty well-known fact these days with all of the obsession with billion-dollar valued companies, or “whales” as I like to call them.

We know that venture investments result in a power-law distribution of outcomes.

And so one or two companies will determine the returns in a given fund.

Sometimes that is not the case. In our 2004 fund it was five companies, but that is why that fund was so good.

The other interesting thing about that chart is why the hit rates and returns in the venture capital industry have not returned to pre-2000 levels.

I think that is all about the amount of capital in the business now. More capital means more businesses get funded. So even if you have more winners, you don’t see the hit rates move up. The numerator and the denominator have both grown in the hit rate calculations.

Before 2000, the venture capital business was a bit of a cottage industry.

In the last 15 years, VC has become an institutional asset class with the permanence and stature that brings seemingly endless amounts of capital to it.

And so the returns have stabilized in or around the 2-2.5x over ten years number, which produces high teens/low 20s IRRs, which is enough to sustain the sector.

The only thing that I think would take us back to mean multiples of 4x or better would be some sort of massive reduction in the amount of capital coming into the venture capital business. And I don’t see that happening any time soon.

But one thing about the VC business has not changed in all of the years in that chart, which is roughly how long I have been a partner in a venture firm, and that is that your big winners will determine your returns.

Same as it always was.

Comments (Archived):

Fred- this post risks having someone dub you “The Prince of Whales”. 🙂

This may be the second whale sighting at the bar. 🙂

“It could be the number of your seed and Series A investments that go public”You’re a big advocate of going public. IPO’s seem to have run out of momentum recently. Palantir is considered to be ‘postponed’. WeWork is not convincing the market. Is the acquisition sale the 10X out right now?

Our portfolio company Cloudflare went public last week. For the top 10% of our portfolio companies, I like IPOs

Sounds like the VC business has become (is becoming) more utility than exclusive exception for many businesses seeking and being funded since the early 2000’s. Does this denote lesser return expectations from most VC Fund portfolios, has this been the case recently and is that a potential expectation for the future? Interesting that very little escapes future commoditization it seems…

I used to work with entrepreneurs in an accelerator program (typically as part of an on-ramp to get angel funded) and currently volunteer with an organization that is a non-profit but growing like crazy (this is outside my day job). The skills and challenges around scaling feel very different from the skills and challenges I have been used to dealing with around “building” when I worked with these very early stage start-ups. It is exciting and scary. I wonder how much of this distribution has to do with the ability of folks to survive the crucible of this transition from building to scaling (and/or folks trying to scale when they need to build at the beginning).

Have you seen building for scale from the start at your organization? This is my preferred approach admitting it is more expensive and hard to sell at the exploration stage.

“The only thing that I think would take us back to mean multiples of 4x or better would be some sort of massive reduction in the amount of capital coming into the venture capital business.”That’s a good point for the industry as a whole, but if you’re an entrepreneur, you want to have more venture capital available as it increases your chances of getting funded. Of course, more money means less discrimination in where it gets invested, hence the returns are lower in the long term.Another positive here is that- if you’re a VC firm who has a good track record, you will look even better when compared to these dwindling return averages.

Also by David Coats:https://medium.com/correlat…

Yup.But can you help me with your math Fred?I was taught “The Rule of 72” – https://en.wikipedia.org/wi… – that the rate of return is equal to 72 divided by the number of years to double the investment. (Or, the number of years to double the investment is equal to 72 divided by the rate of return.)To wit, an investment generating 7.2% per year returns will double in 10 years (72/7.2=10). So how do you figure that funds that are 2X or even 2.5X are generating returns in the high teens/low 20s?(Btw, my understanding is that, on a broad Cambridge Associates industry wide type view, VC funds aas an asset class do generate 2X-2.5X or so — but that’s a poor showing, as the S&P500 has beat that for last decade.)

I had the same question, but you beat me to it as I was “checking my math”….

The rule of 72 applies to compound interest. While Fred is referring to Internal rate of Return (IRR). Compound interest assumes a one time initial investment, and one time final cash outflow. While IRR accounts for multiple cash inflows and outflows at different times within that same overall time period.Cash-over-cash multiple is probably a better way to look at VC fund performance, but the industry seem to want to also compare IRRs which can be misleading (or “managed”) based on inflow/outflow timing. In the end, what matters is the cash-over-cash multiple over the mentioned 10 year period.See the attached piece -https://www.forbes.com/site…@JLM:disqus

Yes I understand and agree with your points. But doesn’t all that further my argument, not refute it?

I did not refute anything. I was responding to your question -“To wit, an investment generating 7.2% per year returns will double in 10 years (72/7.2=10). So how do you figure that funds that are 2X or even 2.5X are generating returns in the high teens/low 20s?”Fred said he is referring to IRR when he mentioned high teens/low 20s. The rule of 72 does not apply to IRR with multiple cash flows.Like I said, IRR can be a misleading number. Cash-over-Cash multiple is a better gauge of fund performance.

Um, ok. But I’ve been an LP in dozens of VC funds over the last 20 years and I respectfully submit, that still doesn’t address my question. How can a fund that delivers “2-2.5X” also have “returns” in the “high teens and low 20s”…? (If it matters, I think my disconnect from Fred’s conclusion is the “ten years” part. I have never invested in a VC fund that was so cashed out in 10 years that one could reasonably conclude what the return was. 15 years, 17 years, more accurate. For example, Fred mentions his 2004 vintage fund. That fund is sufficiently harvested that final determinations can be made. That was true a couple years ago, soonest, so maybe 12-13 years. But USV’s 2008 fund is still in late mid life…)

Good point. The timing of all the cash flows is important. If you invest $100M a year over ten years and get $2.5B on the back end that is an IRR of ~ 19%. But, if you have to tie up capital in a low yield, liquid investment to support these later cash flows then that is a hit to the actual IRR in terms of opportunity cost.

.The difference between Simple Return and IRR is important. Both are useful.It is appaling that they would be confused — OK not appaling but troubling.I agree more with you than you do with yourself.JLMwww.themusingsofthebigredca…

Girish is correct in his reply below. I like to model VC funds with 20% per year inflows in the first five years and 20%*X outflows in the second five years, with X being the fund return multiple.

Given that the big winners are so much bigger than the rest, obviously ROI from the big winners essentially determines the ROI of the fund. No magic or great insight here.The consideration of “hit rate” is just embarrassingly brain-dead; the several different definitions do confirm that. Obviously the single most important metric is fund ROI, but no definition of hit rate can accurately approximate ROI because a “hit” doesn’t include how big the hit is. Even if define the hits as “10X” or unicorns, or whatever, still don’t know how big the hit is: Hits of $1 billion, $10 billion, $100 billion, and $500 billion have very different effects on ROI, the best single measure.Hit rate is good when comparing VC projects with US national security high technology projects: Since the national security projects don’t easily result in ROI figures, can define a hit as a project that was as successful as initially planned. With this definition, it appears that VC is WAY behind US national security. E.g, while VC can think of some mobile app as high risk, no one believed that Keyhole, GPS, the F-117 stealth, the first US nuclear powered submarines, laser guided bombs, the SR-71, or Sosus wouldn’t work. The US national security hit rate is TERRIFIC.A HUGE difference is that US national security strongly exploits secret sauce while VC just looks to match up routine technology with fleeting market opportunities, that is, with essentially no secret sauce advantage. That situation is because VC refuses to evaluate secret sauce and, actually, at present, is incompetent to do so or even to direct an evaluation. DoD, NSF, and NIH problem sponsors are terrific at getting really good evaluations of secret sauce. VCs are general partners of limited partners who think essentially like commercial bankers; thus the VCs are forced to act much like commercial bankers.If VC wants more 10+ X returns, then fine: Easy. Routine. Low risk. Piece of cake. Just match up market needs with new, correct, significant technology, proprietary secret sauce, difficult to duplicate or equal, that is powerful and valuable in business because it gives the first good or much better solution to some big problems — the dream would be a one pill taken once cure for any cancer. So, pair off the market needs with powerful solutions with technology secret sauce.But so far there’s no chance of this because the limited partners apparently are much like the managers of the Michigan State Pension Fund as depicted in the movie The Big Short; when they want to evaluate something in business, they go first to accountants and maybe to Standard and Poors. Bummer.Technology in business? Yup, when I was Director of Operations Research at FedEx some 0-1 integer linear programming set partitioning could have saved FedEx ~15% of fleet direct operating cost — not trivial stuff. I’d already saved the company with some rush, 6 weeks, software for scheduling the fleet. The ~15% was to be my second act! I got a Ph.D. instead! FedEx COULD have had the 15% — they blew it.

The difference is that .Mil and Intel seek ROM, Return on Mission, not ROI. Ironically, taking this approach actually results in superior ROI. This is the approach we are pursuing at Methuselah Fund. What’s missing in the private sphere for ROM investing is post seed investment for exactly the reasons you mention above re standard VC “it has to be about the money” tactic. We are exploring Reg A+ as an alternative path…

.MIL ROI?? How ’bout:(1) Have DARPA still running the Internet and getting a penny a packet!(2) Have the USAF getting a penny for each use of GPS!Soon own the world and everything in it!(3) Essentially all the commercial airliners use high bypass turbofan engines originally developed for the USAF C5A — have the USAF license that technology!Uh, burning the fuel gives kinetic energy as 1/2mv^2 but what want to move the plane is momentum of mv. So are buying 1/2 mv^2 but want only mv. So use the 1/2mv^2 to drive a fan that generates mv; get v lower but m higher and, net get more momentum. Warning: Only works subsonic.Much, MUCH better: Have AT&T get a penny per transistor! Now we are up to a few billion transistors per $100 processor!Do pretty well: Have Princeton (Tukey) and IBM (Cooley) license the fast Fourier transform, maybe just for uses in the oil patch!

I wonder if 2.0 to 2.5x will cut it in the long run for the asset class as currently constructed. Someone can check my math but a 2x return over 10 years is ~7% annualized return? The S&P 500 in the current bull market has returned > 13% annualized with dividends reinvested over the last 10 years. A little over 10% over the last 50 years.https://dqydj.com/sp-500-re…From my understanding VC investments are still a relatively small percentage of total investment in pensions, endowment funds etc. Beyond straight returns perhaps there is a diversification benefit to a larger portfolio that will help sustain as well.

See the comment above about that.

Thank you Fred. Really enjoy the blog.

.When talking about “return on investment” there is no substitute for actually calculating ROI.There are a few financial rules of thumb — talking about you Rule of 72 — but this rule is arithmetically sound though it feels a little like chicken entrails.There is “maths” behind it.This hit rate approach makes for interesting first cup of coffee after a hard night sort of jabber, but it is more confusing than just putting a pencil to the real numbers.I think the world has gotten it that in the VC ROI mish mash a few good deals carry all the dross. So, no wisdom in the second kick of that mule.Great Sunday to all brunchers. Tip generously. It is easier to calculate 30% than 15%.JLMwww.themusingsofthebigredca…

Here, 30% tips would give you fast ROI if you are a regular, in the form of prime service. Normal, which is suggested in the tab, is 10%.Great Sunday to you, señor Jeff. Glad that Humberto decided to stay fishing.

Where have you been Señor Brass ?

Have to remember, he’s just coming out of winter down there, and as we head into fall he is just coming into spring!In particular, as we enter an AI winter, he’s just been in one!Also have to remember it might be a little confusing to have the clocks and time zones like ours but the seasons all wrong!

Yes, it has been a very dry winter, the bloom just passed so we are ready to enter spring. This is the best season here in Santiago because the windy days clear the air, which during the winter is quite polluted.GMT -3 right now.As for AI, and the AI winter 🙂 I am doing some research and experiments with natural language processing and image recognition, nothing too deep, only benchmarking the most performant libraries to see what type of real world tasks can be achieved in the context of personal spatial awareness.How are you and things up there? Projects, cat, etc? 🙂

Good luck with the AI tools: To me it’s amazing they work at all. Since at least to some extent the tools do work, maybe you can find a good application.I moved, same time zone. I’m finishing up moving.The startup is fine, just needs me to get the moving done. Then gather some data, do some routine things, e.g., static IP address and domain name, and do an alpha test!

Hello Girish, I have been busy working (for others) here in Santiago, which have changed my daily navigation patterns a bit. Following AVC in lurk mode mostly. This cycle is almost done so I hope to visit more regularly. How are you?

Ah, Ok. Good to see you, even if infrequently.

In other words, VC – like all financials services markets – is ruled by the Law of Unaligned Interest: the client who doesn’t need you is the one that is most valuable.It’s why finance a$$hole$ are so prevalent.

Here’s my q. If 2-2.5x is the norm, how does that compare to PE funds. And if PE funds are better or the same, wouldn’t that dictate over time cash from allocators flows from VC back into PE? Would think VC funds have much higher incidence of <1.0 returns than PE funds and not sure how many more incidences of > 3,4,5x. Seems to me over time less cash should be allocated to this asset class if only delivering those returns

Great point. I think VC returns are approaching PE returns. As long as they are similar, allocators might keep putting money into both

https://www.correlationvc.c…An overly conservative approach to venture?

This is my second example today, of a tightly edited write up on the meat of a business model/problem statement. +100 and stored for posterity. There is an entire semester’s worth of education in this single post. Well done Fred and thank you for your transparency.The first example was BalajiS posting a screenshot of the original bitcoin hypothesis/email on twitter. It was and is a simple problem statement – boy have the “experts” made a mess out of it. https://uploads.disquscdn.c…

Question:why do you think the two lines have begun to separate this past year? Is the avg of the 10X+ bucket higher? Would be interesting to see the avg of the 10X+ bucket over time.