Funding Friday: Still Standing

I backed a documentary project this morning about two 80-year-olds pursuing their lifelong dreams to be stand-up comedians.

I think people of any age should chase their dreams and I can’t wait to watch this film.

I backed a documentary project this morning about two 80-year-olds pursuing their lifelong dreams to be stand-up comedians.

I think people of any age should chase their dreams and I can’t wait to watch this film.

I am heartened to see both sides of the political aisle in the US came together yesterday to agree to move forward on a $1 Trillion Infrastructure Bill.

There are parts of the bill that I don’t like (asking blockchain smart contracts to send 1099s to the IRS seems nuts to me) and parts that were taken out that I think are critical (like building a nationwide EV charging network).

But perfect is the enemy of the good. We have not had a functioning legislative branch at the federal level in the US in a long time. I am hopeful that a bipartisan victory on infrastructure will pave the way towards other bipartisan efforts and the right and left will start talking to each other, respecting each other, and governing again.

I have spent my adult career making deals with people. I have learned that you can never get exactly what you want when you make deals. You must compromise so that both sides can feel that they won. And when you do that, there are many times when both sides do win. If you choose to sit on the sidelines, you almost always lose.

I am happy to see that our elected officials in Washington have decided to get back into the game again.

The two most used measures of a venture fund’s performance are the “cash on cash” return and the “internal rate of return” (IRR). One measures how much an investor got back divided by how much they put in (cash/cash). The other measures what the effective rate of return is on the investor’s money.

You might think these measures go hand in hand, but that is not the case.

I was reminded of that last week when I was reviewing USV’s second-quarter reports that we will send to our investors soon. Three of our most mature funds showcase how these numbers can behave differently.

Our 2008 vintage early-stage fund has generated about 5x cash on cash but only generated a 22.5% IRR.

Our first Opportunity Fund, raised two years later in 2010, has generated only 3.9x cash on cash but generated a 58.6% IRR.

And our second Opportunity Fund, raised in 2014, has generated 7.3x cash on cash but only 46.7% IRR.

Our Opportunity Funds invest in the later stage rounds of our top-performing portfolio companies plus a few later-stage investments in companies that are new to USV. The average holding period of these investments is materially shorter than our early-stage funds and so they typically produce higher IRRs for a given cash on cash performance. That explains why our 2010 Opportunity Fund has a lower cash on cash return but a much higher IRR than our 2008 early-stage fund.

But even for the same strategy, you can get materially different numbers. Our 2014 Opportunity Fund has a higher cash on cash return but a lower IRR than our 2010 Opportunity Fund. That is because our 2010 Opportunity Fund had a few very fast material exits and our 2014 Opportunity Fund had a more typical holding period for its material exits.

Venture capital funds do not take down the entire capital commitment upfront. They take it down over time, often over four or five years. And the money comes back over time as well. So the timing of the cash in and cash out has a very big impact on IRR, but zero impact on cash on cash.

So if these two measures behave differently, what is the more important number? For me, it is cash on cash. I care less about how quickly the money goes in and comes out of a fund and more about the total return of the fund. Our early-stage funds can often take 15-20 years to be fully liquidated but they can also produce much higher total returns.

I have found that patience is often rewarded in early-stage investing. If you want to make 5-10x on your money, you need to be prepared for long holding periods. That reduces the IRR but generates high cash on cash returns.

Rocky Mountain Power emailed me last week and offered us a “100% Solar Match” which means that we can “match” all of our energy consumption in our home in Utah with power from their 20 megawatt solar plant in Holden Utah.

This doesn’t mean our home will be now be operating with energy from that plant but it does mean that we have opted for 100% solar. If every Rocky Mountain Power customer opted for this match, they would have to build more solar plants and decommission carbon based energy facilities.

There is the question of how Rocky Mountain Power could operate an all solar grid (they can’t as far as I know) and whether most customers care enough to specify what kind of power they want to purchase.

But I found the experience simple and easy. One phone call and I was cut over. And now I feel better about the energy we consume in Utah.

It does feel like a bit of a gimmick but it’s a positive one in my book.

I’m going with something a bit different today on Funding Friday.

Longtime AVC reader Kirsten Lambertsen has created an email newsletter featuring creators and their projects across many different creator platforms. It is called Patron Hunt.

It looks like this:

I just signed up and you can do that too right here.

I have written about stablecoins in the past. I think they are a very important part of the crypto asset landscape. Two of the top ten crypto assets by market cap are stablecoins, Tether ($62bn) and USDC ($27bn). You don’t buy these assets to generate gains because they are price stabilized. You hold them like cash, to be able to move in and out of trades, purchase things, etc.

Countries around the world are looking at stablecoins and thinking “we should issue these assets via our central banks.” That is called a “central bank digital currency” or CBDC for short. China is the farthest along on a CBDC but many other countries around the world are thinking about CBDCs or building them.

Yesterday, SEC Commissioner Hester Pierce suggested that stablecoins are preferable to CBDCs.

Hester focused on the privacy concerns around CBDCs, and I agree with her that I would rather hold USDC than a Fed issued digital dollar.

But there is another more important reason to want stablecoins to win over CBDCs – competition.

When you have competition, you get innovation, new features, composability, and a host of other important benefits. When you have a monopoly, like the US Government or any government, pushing out the alternatives and forcing us to use their digital dollar, you lose all the value of competition. And that would be a terrible thing.

I am all for central banks issuing digital currencies. But they should compete for our usage with market-based stablecoins. Then we get the best of both worlds. I hope policymakers in the US and around the world understand the importance of competition and allow stablecoins to co-exist with CBDCs.

This morning I was sitting outside of my coffee shop, sipping on a cortado and reading the news on my phone while the NY Times, which I buy for The Gotham Gal every morning, sat folded up next to me. I gave up on mainstream news media two decades ago and have been relying on the Internet for news for a long time now. By “Internet”, I mean blogs, Twitter, and increasingly, email newsletters.

What I was reading this morning on the bench sipping coffee was News Items, an email newsletter by John Ellis. News Items is a subscriber-only newsletter, as opposed to the free stuff you can get on Axios. But you get what you pay for with John. His newsletter is smarter, edgier, and out in front of most anything else out there. The topics that interest John the most are technology (lots of biotech), geopolitics, and finance.

The way John describes it is:

Three baskets: (1) World in Disarray, (2) Financialization of Everything and (3) Advances in Science and Technology. Bonus basket: Electoral politics in the US and around the world. Six days a week, not Sundays.

I paid $3 for the New York Times at my coffee shop this morning. I pay $99 a year for News Items. And I get things every day from News Items that I never get from the New York Times. And I don’t have to read the nonsense that the New York Times churns out non-stop these days.

If you want more news and less nonsense, you might want to give News Items a try. You can do that here.

You can also listen to John five days a week on our portfolio company Recount’s podcast network. He and his co-host Rebecca Darst cover the same news stories that John puts in his newsletter. Here are the most recent episodes:

Over the last 18 months, the early-stage financing market has seen dramatic changes characterized by these three things:

I believe that for the most part, these changes will be permanent.

And I believe that for the most part, these changes are good for early-stage company formation and innovation.

However, there will be some negative side effects from these changes and one that I worry about is the “bad marriage problem.” Unlike public markets, private market investments are held for many years, often a decade or more. If an investor and an entrepreneur find each other difficult to work with, there is no easy solution. There is no divorce court for startups. And so the result is likely to be entrepreneurs and investors getting stuck in bad marriages.

There are a few opportunities to address this issue. There is a vibrant secondary market for private investments and while it is mostly limited today to well-known later-stage companies, it could develop into a broader market as the capital seeking to get invested in early-stage innovation continues to grow unabated. It is unlikely that founders will be able to force investors out of their cap tables via the secondary markets, but a voluntary separation via the secondary market seems more likely to me.

I also think startup boards need to evolve. There should be many more independent directors and many fewer investor directors on startup boards. Investors should be more open to observer seats and founders should have more say in which investors sit on their boards. I am not arguing that founders should control their boards, but I am arguing that investors should not control the boards. I think independent control is the most sustainable solution.

We know that bad marriages are hurtful to everyone, not just the spouses. Companies that have dysfunctional founder/investor relationships suffer from them. And the shotgun marriage environment we are operating in right now (and for the foreseeable future) will likely create more of them. So we should be thinking about solutions to end these bad marriages and let everyone move on to better ones.

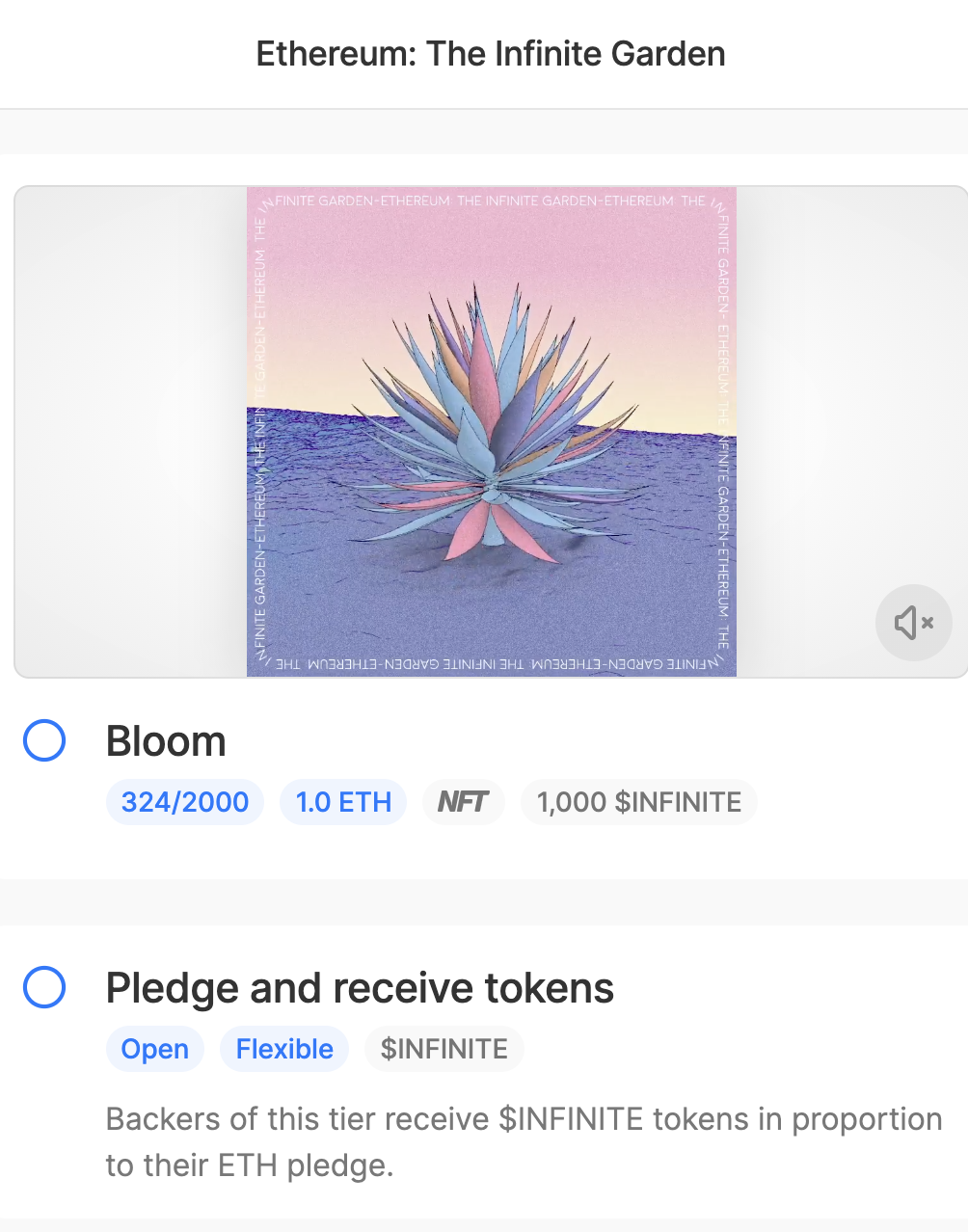

ETHEREUM: THE INFINITE GARDEN is a “feature-length documentary film that explores the innovative real-world applications of the Ethereum blockchain, the die-hard community of enthusiasts and developers, and its creator, Vitalik Buterin, whose vision for the internet has the potential to change the world.”

The film is being crowdfunded on the Ethereum blockchain and the campaign ends at 6pm eastern time today.

When you choose to back the project, you will have a choice to pledge one ETH and get an NFT from the film or pledge less and get a token recognizing your contribution.

I backed the film earlier this week and as of this morning, the film has raised 500 ETH of the 750 ETH goal.

You can back the film here.

My family has a history of irregular heartbeats, from PVCs to AFIBs. So when I saw my cardiologist recently, I asked him how I could track my beats. I have worn a Holter Monitor a few times and did not want to do that again unless it was absolutely necessary. He pointed me to this Kardia Mobile device which I purchased on Amazon a few weeks ago.

This Kardia Mobile 6L device is remarkable. It delivers a “6 lead” EKG reading into your smartphone by putting the device on your knee and pressing both thumbs on it. I realize that 6 leads is not the same as what you get with a Holter Monitor or an EKG in your doctor’s office. But it is really amazing because it is so easy to use in your own home. It is the size of an Apple TV remote, maybe even a tad smaller. I just email my cardiologist the result and he tells me what is going on without him having to take fifteen minutes or more to see me and without me having to visit his office.

This is just one example of the revolution underway in health care. Driven by advances in technology, a computer in everyone’s pocket, ongoing changes in the healthcare system accelerated by the pandemic, among other forcing functions, we are seeing more and more healthcare being accessed in our homes vs in the doctor’s office.

This does not mean that doctors are needed less. I think they are needed more. But they can focus their time and energy where it is most needed, in providing the care itself vs all of the other things that lead to the care.

This has the potential to both increase access to care and also reduce the cost of it. We will need other changes to the healthcare system for those things to be realized. We will need the healthcare system to move away from a business model based on the provision of care in favor of a business model based on outcomes. We will need the power of the payors to be reduced in favor of the power of the patients. Those changes must be driven by society/politics and they won’t come easy.

But the conditions are ripe for a reshaping of the healthcare system. Entrepreneurs (like the folks who made the Kardia Mobile device) and risk capital can and will be an important force in driving that change.