After predicting an IPO bonanza in my new year’s day post in 2015, and being largely wrong about it for four years, we are finally seeing it happen.

I am not exactly sure what it is about this year, as opposed to any of the last five years, that has drawn all of these highly valued private companies into the public markets, but here we have it.

It does take a number of years for a privately held company to prepare to be a public company. They need to get their finance and legal houses in order, they need to beef up their teams in these areas, and they need to make sure they have a repeatable business that they can manage under the spotlight of the public markets.

Already we have seen S1s from Lyft, Pinterest, and Zoom. And we are likely to get them soon from Uber, Slack, Airbnb, and a host of others, in the coming months.

I see this as largely beneficial to the startup sector for the following reasons:

1/ We will have benchmarks from highly liquid markets in terms of what these high growth tech companies are worth. Until now, most of these benchmarks have come from illiquid private market auctions, which are not exactly the best price discovery mechanisms.

2/ Many employees, angels, seed investors, VCs, and growth investors will get liquidity from these investments and recycle it back into the startup sector. More capital means more startups and more innovation.

3/ Limited Partners, the providers of capital to venture capital and growth equity funds, will get large distributions which will give them more confidence in the startup sector and they will continue or perhaps step up their commitment to invest in early stage technology.

4/ These newly public companies will be able to accelerate their acquisition programs now that they have liquid stock and cash to fund those deals. That will further flow capital back into the startup sector.

Of course there will be negatives. It will be harder than ever to afford to live in the bay area. But tech folks from the bay area are certainly welcome in NYC, LA, and any number of other startup regions around the US. Get paid on your stock and move to a more affordable and liveable region!!!

And the monster funds that have been advocating staying private forever will have to argue why these IPOs are not what every other startup should be aiming for. And I think that argument is going to be harder and harder to make with this IPO bonanza under way.

All in all, I think the IPO bonanza that is under way in 2019 is a good thing. I have been expecting it and wanting it for years and I am pleased that it is now upon us.

We are now seeing a wave of longtime private companies coming public and with that we are getting data on usage, financial performance, and a host of other issues that is very useful market data.

I spent some time looking at Pinterest’s S1 today. They filed it a week or two ago.

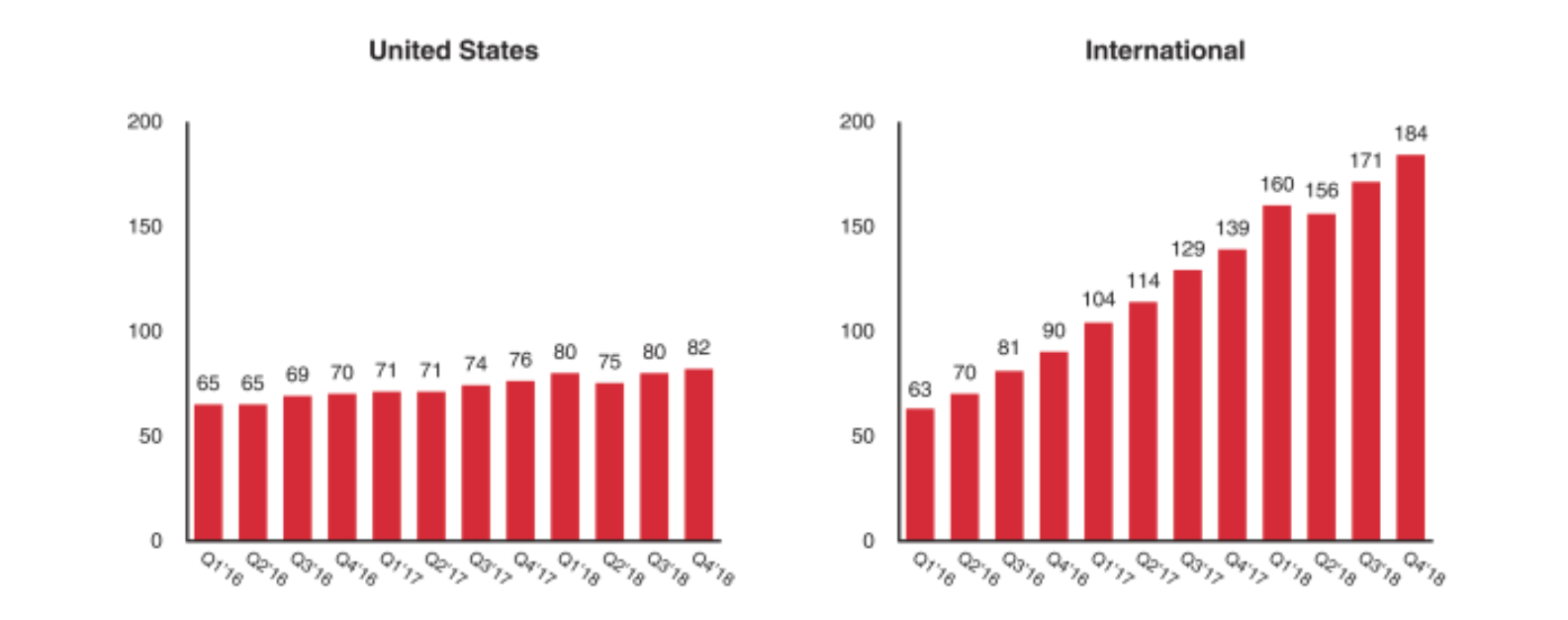

I found this chart of user growth quite interesting:

That shows monthly active users in the US and International over the last few years on a quarterly basis.

Pinterest is rapidly growing its user base outside of the US but usage in the US has stalled out.

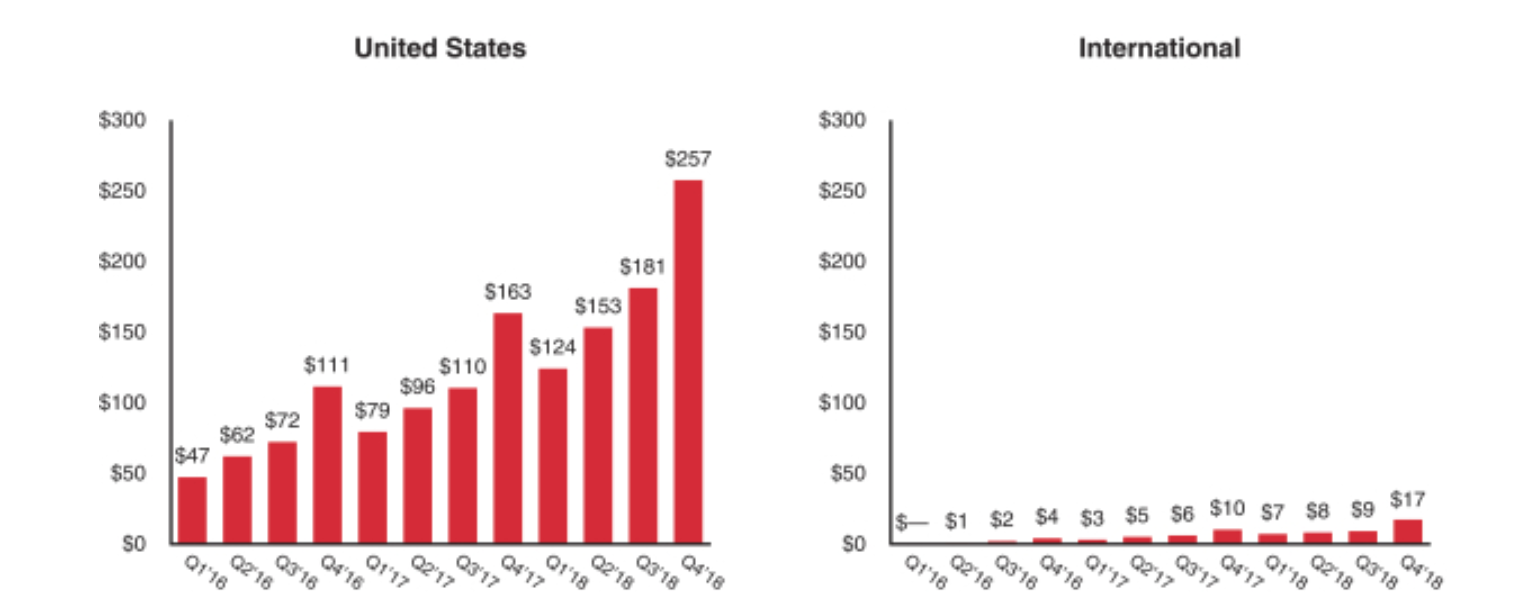

This chart, also from the S1, shows revenue growth in the US and Internationally:

So what you can see is that Pinterest has been growing its US revenues rapidly but not its US user base. And on the other hand, Pinterest has been growing its International user base but its International revenue is still nascent.

So the question is whether Pinterest will be able to monetize its rapidly expanding international user base.

That is the kind of insight you can get from reading these S1s. I find them fascinating and try to read them when they come out.

I don’t plan to buy Lyft or Pinterest when they come public. That’s not really my thing. And I don’t have an opinion on whether they are attractive investments or not. But I do think we can learn a lot about these businesses from reading S1s and that can help us with the investments we do have.

I expect we will see IPOs from big names like Uber/Lyft/Slack, although I also expect those deals will get priced well below the lofty expectations they have in mind right now. Some of that will be because of weak equity markets in the US, but it is also true that most of the IPOs in 2018 also priced below the lofty “going in” expectations of founders, managers, boards, and their bankers. The public markets have been much more sanguine about value than the late stage private markets for a long time now.

When I see an IPO price range, I like to go look at the S1 that the issuer has filed with the SEC prior to the road show. Here is Lyft’s S1.

Here are the things I like to look for in a S1:

1/ The total shares outstanding. You can go to the table of contents of the S1 and look for the section called “Description Of Capital Stock”. In Lyft’s S1, it says there are ~240mm shares of Class A common stock plus some amount of Class B common that is not yet detailed. The Bloomberg article I linked to above says the company is going to sell 30.8mm shares at $62 to $68 per share. So there will be at least 270mm shares outstanding plus the Class B shares. The Bloomberg folks seem to be using a post deal share count of 288mm share so that is close enough. You get to fully diluted post deal valuation by multiplying the share count (288mm) by the range ($62/share to $68/share).

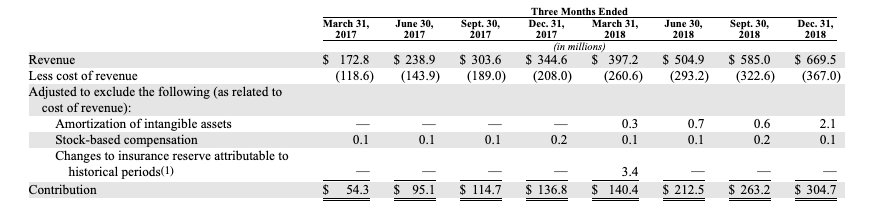

2/ Revenues and earnings/losses. You can go to the table of contents of the S1 and look for the section called “Selected Consolidated Financial And Other Data” and you will find the audited financial data. I like to find the quarterly numbers because that will give you a good idea of current growth rates. These are the numbers for Lyft:

As you can see the quarterly revenues are growing at roughly $80mm a quarter so a back of the envelope guess on revenues for 2019 are [$750mm, $830mm, $910mm, $990mm] for a total of ~$3.5bn, up from $2.1bn in 2018 (yoy growth of 65%).

You can also see that the contribution (net of cost of goods sold) has been about 45% over the past few quarters so if that ratio holds in 2019, there would be contribution of roughly $1.6bn in 2019.

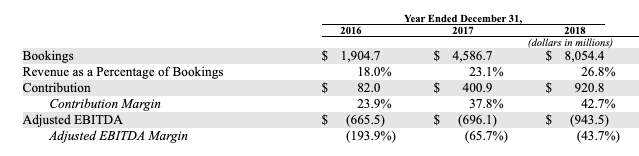

For the operating costs, you can look at the difference between contribution and EBITDA, which you can see here:

Lyft spent ~$1.85bn on opex in 2019 ($921mm of contribution plus $943mm of EBITDA losses). That number grew from $1.1bn in 2017. I would expect Lyft’s operating expenses to be at least $2.25bn to $2.5bn in 2019.

Which gets you to this possible P&L for 2019:

Revenues – $3.5bn

Gross Margin – $1.6bn

EBITDA (loss) – $600mm to $900mm

3/ Valuation Ratios:

At the mid-point of the offering range $18bn, the price to revenue multiple is roughly 5x (18/3.5) and the multiple of gross margin (what Lyft keeps after paying significant COGS) is roughly 11x (18/1.6).

4/ Time to cash flow breakeven. This is harder because you have to make some assumptions about growth rates beyond 2019 and opex growth rates. But if Lyft can grow revenues at 60% per annum for a few more years and keep opex growth rates to 25-30% per annum, then it could get profitable by sometime in 2021. This suggests that the $2bn it is raising may be sufficient to get profitable, but it will be close.

So what does this mean for other late stage high growth high flyers?

To me it says if you have company focused on a big opportunity (like transportation) that is growing at north of 60% per year it is worth in the range of 10-12x net revenues to wall street right now. Because Lyft only keeps about 45% of its revenues after very high COGS, that works out to be 5x revenues.

Many late stage private companies are getting financed at valuation ratios in excess of this so they will have to grow into their eventual public market valuations. But that has been the case for quite a while now as the late stage private markets continue to pay higher prices for high growth companies than the public markets do.

Today, as is my custom on the first day of the new year, I am going to take a stab at what the year ahead will bring. I find it useful to think about what we are in for. It helps me invest and advise the companies we are invested in. Like our investing, I will get some of these right, and some wrong. But having a point of view, a foundation, is very helpful when operating in a world that is full of uncertainty.

I believe and have been telling those around me that I think 2019 will be a “doozy.” I think we will see major dislocations in the leadership of the United States, a bear market in stocks, a weakening economy, a number of issues with the global economy including a messy Brexit and a sluggish China. All of this will lead to a more cautious stance by investors in the startup economy. And crypto will not be a safe haven for any of this although there will be signs of life in crypto land in 2019.

Let’s take each of those in the order that I mentioned them.

I believe that we will have a different President of the United States by the end of 2019. The catalyst for this change will be a devastating report issued by Robert Mueller that outlines a history of illegal activities by our President going back decades, including in his campaign for President.

The House will react to Mueller’s report by voting to impeach the President. Which will set up a trial in the Senate. That trial will go so badly for the President that he will, like Nixon before him, negotiate a resignation that will lead to him and those close to him being pardoned for all actions, and Mike Pence will become the President of the United States sometime in 2019.

I believe this drama will play out through most of 2019. I expect the Mueller report to be issued sometime in the late winter/early spring and I expect an impeachment vote by the House before the summer, leading to a trial in the Senate in the second half of the year.

The drama in Washington will have serious impacts to the economy in the United States starting with our capital markets.

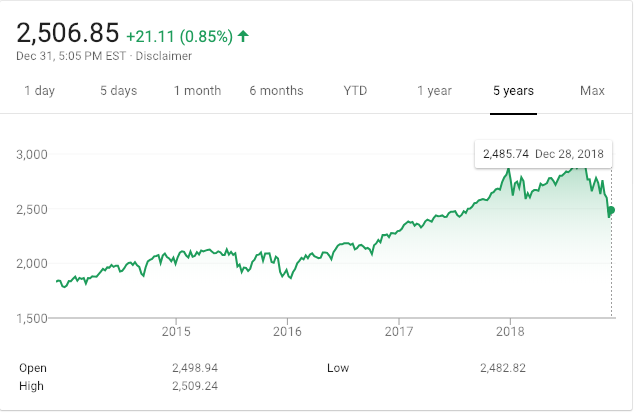

The US equity capital markets enter 2019 on shaky ground. Though the last week of the year brought us a relief rally, the markets are dealing with higher rates, some early indications of a weaker economy in 2019 (possibly due to higher rates), and, of course, the potential for the drama in Washington that we’ve already discussed. Here is a chart of the S&P 500 over the last five years:

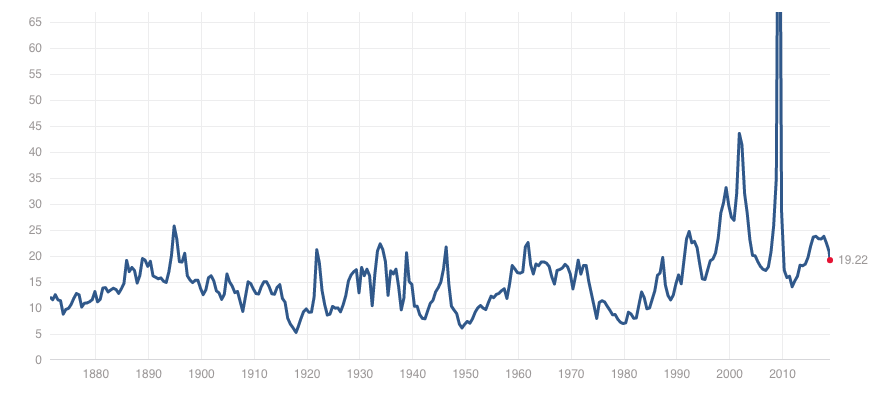

I expect the S&P 500 to visit 2,000 sometime in 2019 and then bounce around that bottom for much of the year. This would represent a decrease in the S&P’s trailing PE multiple to around 15x which feels like a bottom to me given the recent history of the equity markets in the US:

S&P PE Multiple (source http://www.multpl.com/)

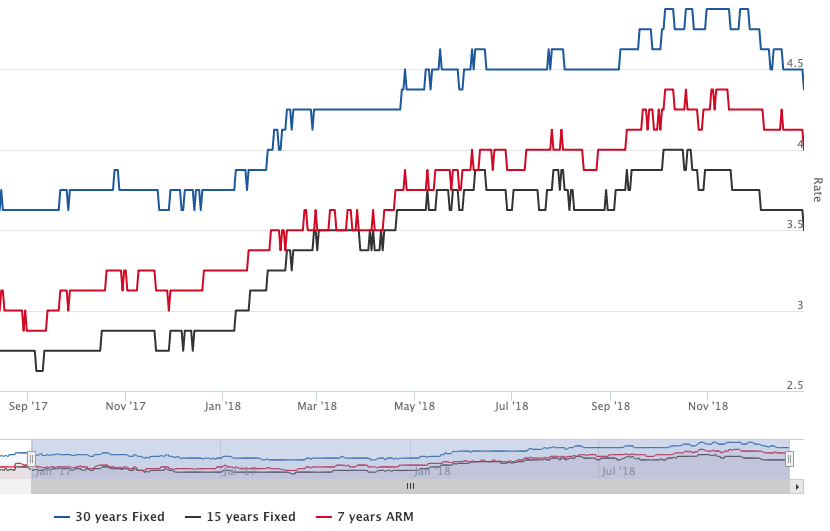

Interest rates have been rising gradually in the US for the last three years. The Fed has taken its Fed Funds rate from essentially zero three years ago to almost 2.5% today:

The rates that are available to consumers and businesses have followed and I expect that to continue in 2019. Here is a chart of the interest rates on the three most popular mortgage products in the US:

Source: https://www.amerisave.com/graphs/

When it gets more expensive to borrow, marginal projects don’t get funded. And what happens at the margin has a much larger impact on the economy than most people understand. No wonder the President wants to fire the Fed Chairman.

I expect the combination of higher rates, uncertainty in Washington, and storm clouds globally (which we will get to soon) will cause business leaders in the US to become more cautious on hiring and investment. Consumers will make essentially the same calculations. And that will lead to a weaker economy in the US in 2019.

The global picture is not much better. The eurozone is about to go through the most significant change in decades with some sort of departure of the UK from the EU (Brexit). It remains unclear exactly how this will happen, which in and of itself is creating a lot of uncertainty on the Continent. I don’t expect most businesses in Europe to do anything but play defense in 2019.

Probably the biggest unknown for the global economy is the resolution of the ongoing trade tensions between China and the US. It seems inevitable that China will make some concessions to the US to resolve these trade tensions. But, of course, what happens in Washington (first issue) may impact all of that. In the meantime, the uncertainty around trade and exports hangs over the Chinese economy. China’s GDP has been slowing in recent years as it achieved relative parity with the US and the Eurozone:

Source: https://tradingeconomics.com/china/gdp

Any significant trade concessions from China could impact its growth prospects in 2019 and beyond, which will take the most powerful engine of global growth off the table this year.

So all of that is a pessimistic take on the broader macro environment in 2019. How will all of this impact the startup/tech economy?

The startup/tech economy is somewhat immune to macro trends. Many startups and big tech companies were able to grow and expand their businesses during the last financial downturn in 2008 and 2009. Some very important tech companies were even started in those years.

The tech/startup economy is driven first and foremost by technical and creative (ie business model) innovation. And that is not impacted by the macro environment.

So I expect that we will continue to see big tech invest and grow their businesses and do well in 2019. I expect we will see IPOs from big names like Uber/Lyft/Slack, although I also expect those deals will get priced well below the lofty expectations they have in mind right now. Some of that will be because of weak equity markets in the US, but it is also true that most of the IPOs in 2018 also priced below the lofty “going in” expectations of founders, managers, boards, and their bankers. The public markets have been much more sanguine about value than the late stage private markets for a long time now.

However, I do think a difficult macro business and political environment in the US will lead investors to take a more cautious stance in 2019. It would not surprise me to see total venture capital investments in 2019 decline from 2018. And I think we will see financings take longer, diligence on new investments actually occur, and valuations to come under pressure for even the most attractive opportunities.

But all of that is going to happen at the margin. I expect 2019 to be another solid year for the tech/startup sector as we are in a possibly century-long conversion from an industrial economy to an information economy and the tailwinds for tech/startup vs the rest of the economy remain in place and strong.

Any set of predictions for 2019 from me on this blog would not be complete without some thoughts on crypto. So here is where my head is at on that topic.

I think we are in the process of finding the bottom on the large, liquid, and lasting crypto-tokens. But I think that process could take much of 2019 to play out. I expect we will see some bullish runs, followed by selling pressures taking us back to retest the lows. I think this bottoming out process will end sometime in 2019 and we will slowly enter a new bullish phase in crypto.

I think the catalyst for the next bullish phase will come as the result of some of the many promises made in 2017 coming to fruition in 2019. Specifically, I think we will see some big name projects ship, like the Filecoin project from our portfolio company Protocol Labs, and the Algorand project from our portfolio company Algorand. I think we will see a number of “next gen” smart contract platforms ship and challenge Ethereum for leadership in this super important area of the crypto sector. I also expect the Ethereum open source community to ship a number of important improvements to its system in 2019 and defend their leadership in the smart contract space.

Other areas of crypto where I expect to see meaningful progress and consumer adoption happen in 2019 are stablecoins, NFT/cryptoassets/cryptogaming, and earn/spending opportunities, particularly in the developing world.

There will also be pressure on the crypto sector in 2019. The area I am most concerned about are actions brought by misguided regulators who will take aim at high quality projects and harm them. And we will continue to see all sorts of failures, from scams, hacks, failed projects, and losing investments be a drag on the sector. But that is always the case with a new emerging technology that allows anyone to set up shop and get going. Permissionless innovation produces the greatest gains over time but also comes with the inevitable bad actors and actions.

So that’s where my head is at on 2019. Do I sound pessimistic? I suspect I do, but I am not. I am incredibly optimistic, like my partner Albert and can’t wait to get going and make things happen in this new year. It is going to be a doozy.

The Nasdaq is down almost 15% from its labor day highs.

Apple is down almost 25% in the last two months.

Facebook is down about 40% since July.

Bitcoin is down about 80% from its highs last December.

Ethereum is down about 90% from its highs in January.

All of those are examples of bleeding, if you happen to own any of them.

So what do you do?

Close out your position?

Buy the dip?

Sit on your hands?

It all depends on your fundamental views on these various investments.

Here are mine.

Apple is the easiest one for me. They aren’t going anywhere, although growth is slowing as they are close to saturating the high end of the mobile phone market. It will be a value stock at $120/share. If it gets there, load up on it.

Facebook is harder. They own some incredible assets like Instagram but the outlook there is cloudier given likely regulation and it won’t be a value stock for another $100 of losses.

The Nasdaq is even harder. Are we in a bear market now? Or just a painful correction? A bull market that is almost ten years old feels long in the tooth and I can see the arguments for a bear market more clearly than a correction.

Bitcoin will form a bottom at some point and is a buy when it does. But where is that bottom? Probably not $4500.

Ethereum feels like the easiest one to make a bull case for right now. It is hated. Everyone has lost their shirt on it by now. Nobody other than developers want to know about it. It feels like time to start nibbling on it but not loading up on it.

But the thing to understand more broadly about what is going on right now is that big sophisticated investors are reducing their risk exposure across all asset classes and have been doing that for some time. The pace of the “risk off” trade is accelerating. Which means a flight to safety is going on. And when that is happening, you really need conviction to be buying.

Our portfolio company Stash, which offers a super simple mobile investing app and has roughly 2.5mm users, did some analysis on male and female users to see if there was a material difference in risk tolerance between men and women on their service.

The conventional wisdom is that men are risk takers and women are more conservative.

Stash found that there really isn’t much difference between male and female users of their service when it comes to risk tolerance.

And they found that women are more tolerant of the highs and lows that come with being an investor.

The back and forth that Elon Musk did over the last few weeks about being public begs the question about whether the challenges of operating a public company outweigh the benefits.

As a public company, we are subject to wild swings in our stock price that can be a major distraction for everyone working at Tesla, all of whom are shareholders. Being public also subjects us to the quarterly earnings cycle that puts enormous pressure on Tesla to make decisions that may be right for a given quarter, but not necessarily right for the long-term. Finally, as the most shorted stock in the history of the stock market, being public means that there are large numbers of people who have the incentive to attack the company.

I fundamentally believe that we are at our best when everyone is focused on executing, when we can remain focused on our long-term mission, and when there are not perverse incentives for people to try to harm what we’re all trying to achieve.

After considering all of these factors, I met with Tesla’s Board of Directors yesterday and let them know that I believe the better path is for Tesla to remain public. The Board indicated that they agree.

So which is it?

I strongly believe that being public is the best form of shareholder ownership for the vast majority of companies and advocate for that path to the companies in the USV portfolio that have the opportunity to be a public company.

The pressure of quarter to quarter execution is hard on a team. But running a company is hard. And the accountability that comes from this quarterly reporting is a good thing too. If you have problems in your business, you can’t hide them. You have to come clean about them, deal with the implications of them, and fix them.

The long-term vs short-term thing is the critique I hear most often. But I don’t buy it. The best run public companies manage to think and act with a long-term focus while being public. I think it comes down to leadership, courage, and foresight more than whether you are public or not.

Stock price volatility is a factor no matter if you are public or not. At least when you are public, everyone knows when your valuation is going down. Private companies are able to hide that from their employees, the media, and others. Which is just kicking the can down the road and that always ends badly. I prefer the transparency of being public on this one.

And the short seller argument is nonsense. People are always working against you. Your competitors are working against you. The media may be working against you. The regulators may be working against you. Short sellers are just another group that wants to see you fail. But they are not the only ones and you can make them pay by executing against your commitments and guidance.

For me, it just comes down to leadership, courage, execution, and setting and meeting expectations. All good companies must have those in place. If you do, being public is not only manageable but preferable.

And I am pleased to see more and more high growth tech companies coming to this conclusion and taking the plunge.

I’ve been Chairman of two public companies in my career and the leaders of those two companies sat down and talked yesterday.

I enjoyed watching that very much and hope you do too.

In this nine-minute video, Jim Cramer talks to Josh Silverman, CEO of Etsy, about what makes Etsy “special” and how being special allows them to compete and win against Amazon.

There are few investors I have more respect for than Warren Buffett and Charlie Munger. So much of what I believe as an investor has come from watching them conduct themselves over the last thirty-five years (that’s as long as I have been paying attention to investing as a discipline). I believe in fundamental value, I believe in buying when others are selling, I believe in holding positions you find attractive over very long periods of time, and I believe in a lot more that they have espoused and done.

“If you buy something like a farm, an apartment house, or an interest in a business… You can do that on a private basis… And it’s a perfectly satisfactory investment. You look at the investment itself to deliver the return to you. Now, if you buy something like bitcoin or some cryptocurrency, you don’t really have anything that has produced anything. You’re just hoping the next guy pays more.”

When you buy cryptocurrency, Buffett continues, “You aren’t investing when you do that. You’re speculating. There’s nothing wrong with it. If you wanna gamble somebody else will come along and pay more money tomorrow, that’s one kind of game. That is not investing.”

It is clear from those words that Buffett sees crypto assets like a baseball trading card or some other form of collectible. And if that were true of Bitcoin, Ethereum, EOS, Zcash, or many other popular crypto assets, I would agree with him.

But what these crypto tokens are is entirely something else. They are the fuel that powers a new form of technology infrastructure that is being built on top of the foundational internet protocols. Ethereum and EOS are smart contract platforms that allow developers to create decentralized applications (Dapps in the vernacular of crypto). Bitcoin and Zcash are stores of value that allow users to participate in this decentralized application space without the need for fiat currencies.

This is the key phrase of Buffet’s that I feel is incorrect “if you buy something like bitcoin or some cryptocurrency, you don’t really have anything that has produced anything.”

Crypto-assets produce decentralized infrastructure. Bitcoin has produced a transaction processing infrastructure that looks a lot like Amazon Web Services (something I am sure Buffett would agree is extremely valuable). Ethereum has produced a similar transaction processing infrastructure which is also able to run smart contracts. I believe smart contracts are the most important innovation we have yet seen in crypto.

What Buffett and Munger may also be saying is that they don’t know how to value this “fuel” that powers the creation of this decentralized infrastructure. If they are saying that, then I agree with them. I don’t know how to value this fuel either. We cannot use discounted cash flow because this decentralized infrastructure may not produce a lot of cash flow. It is designed to create hypercompetitive networks that are self-commoditizing.

It is much more likely that these crypto assets will trade and be valued like currencies that underpin economies. There has been a lot of research and writing on that. I have recommended Chris Burniske’s Cryptoassets book here before and I will do so again. Chris outlines much of this thinking in that book.

I doubt Warren and Charlie will read this post. But if they do, the one thing I would hope they take from it is that instead of disparaging crypto assets with words like rat poison and dementia, they take a little bit of time to understand that what we are seeing here is the creation of a new internet, built upon protocols that allow for decentralized networks to form and tokens that allow people and companies to be compensated for that formation. And that cryptoassets are the fuel that power and compensate for that formation. And that purchasing these cryptoassets is very much a form of investing. And that this investing is the first time that anyone in the world, independent of wealth and domicile, can participate in venture capital style investing in the next big wave of technology.