The Hidden Cost Of Extending Option Exercise Periods

Many people in startup land believe that the answer to the challenges around forcing departing employees to exercise vested options is to simply extend the option exercise period to the maximum (ten years) allowed by the IRS.

It certainly is one of the techniques that are available to companies and one that a number of our portfolio companies have adopted. Another option, and one that I prefer, is for a market to develop around financing these option exercises (and the taxes owed) when employees depart.

However, if you are thinking about extending the option exercise period for departing employees, you should understand that it will cost your company something.

Here is why:

Options are worth more than the spread between the strike price (the exercise price) and what the stock is actually worth. They have additional value related to the potential for the stock price to appreciate more over the life of the term of the option.

There is a formula that options traders (and companies that issue options) use to value options. It is called the Black-Scholes formula.

If you click on that link, you will quickly realize that the math used in the Black-Scholes formula can be complicated. But fortunately, there is a neat little web app that I frequently use to estimate the value of an option. It is here.

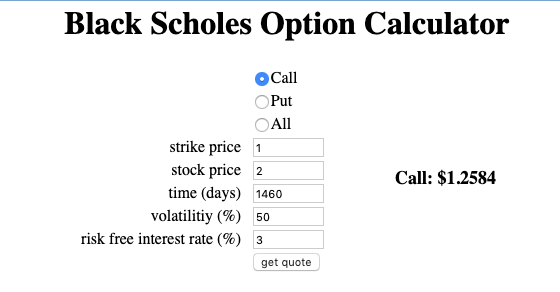

So let’s say that your company is issuing options at $1/share (your 409a) but your most recent financing was done at $2/share. Then a four year stock option is worth roughly $1.25/share.

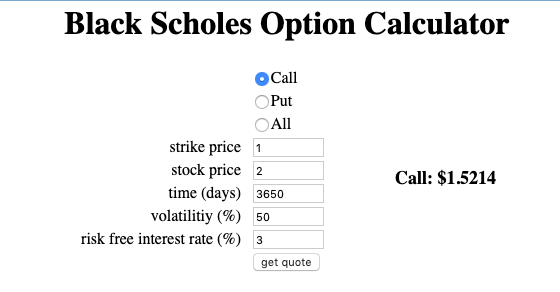

If, on the other hand, you offer a ten year option exercise period to your employees, the value of the option rises to $1.52/share, reflecting the longer period of time that the stock could appreciate over.

That is a 20% increase in the cost of issuing stock options. You could mitigate that by reducing the number of options you issue to incoming employees by 20% but that might make your equity comp offers less attractive to the “market” because incoming employees won’t value the longer exercise periods appropriately.

Stock based compensation costs are real costs even though many in startup land think of options as “free” because they don’t cost cash. The accounting profession has attempted to estimate these costs and companies do put stock based compensation costs on their income statements. If you go with ten year exercise periods instead of four year exercise periods, expect those expenses to go up significantly. Twenty percent is just the amount in my example. It could be larger, possibly as high as fifty percent (or more) if your exercise price is a lot closer to the current value of your stock.

This extra value of a ten year stock option versus a four year option is known as “overhang” by investors. It is the cost of carrying a group of people who have a call option on your stock but don’t have to pay for it for a long period of time. Generally speaking investors don’t like a lot of overhang in a stock.

All of that said, employees are the ones who create value for shareholders. They need to be compensated for that. And I am a fan of both cash compensation and stock based compensation. I like to see the employees of our portfolio companies well compensated in stock. That has a cost and everyone should be well aware of what it is. Longer exercise periods increase that cost. I would rather put more stock in the hands of the employees of our portfolio companies than give them longer exercise periods. But regardless of where one comes out on that tradeoff, it is important to recognize that it is a tradeoff. There are no free lunches, not even in stock option exercise periods.

Comments (Archived):

why not just use restricted stock units instead of options?

for reference, just looked up fred’s previous post on RSUs: https://avc.com/2010/11/emp…

They are generally more expensive for a unit of stock exposure than options.

TANSTAAFL (There ain’t no such thing as a free lunch) Time premium is everything with options. Longer dated options have more time premium built in.By the way, you can pick up dimes in front of a steam roller when you sell options premium. Works until you have a high vol day that blows up your position.

LTCM showed the fallibility of Black-Scholes and that volatility is sometimes a proxy but is not the same as risk. It’s risk that you want to model but can’t with Black-Scholes.

I couldn’t quite understand that calculation, would love to clarify:”So let’s say that your company is issuing options at $1/share (your 409a) but your most recent financing was done at $2/share. Then a four year stock option is worth roughly $1.25/share.”It’s always hard for an employee to really understand how to value an option but in the scenario described above is the implied value to the employee $1/option?If you were granting them 10,000 options then they would do the mental calculation that the value of those options is 10,000 x ($2 share value – $1 strike price) = $10,000 (assuming present day value). i.e. if they were foregoing salary in lieu of options they would mentally assume that those options are worth $10k.So let’s say they’re given a salary/options choice, the employee says “I can get $10k in cash or $10k-worth of shares (in the form of options) – do I want to make a bet on the company appreciating or take cash instead?”Is what you’re saying above that the Black-Scholes calculation shows that option to actually be worth 10,000 x ($1.25-$1) = $2.500 or (10,000 x $1.25) = $12,500?

$12,500. If you are issued an option today that you can exercise at $1 and the fair value of the stock is $2, it’s immediately worth $1, since you can exercise today for $1, and have stock worth $2.But you don’t have to exercise today. What if when you exercise it’s worth $3? Then you would have made $2, not $1.So black-scholes attempts to put a price on that optionality. With the example inputs Fred used, the options is worth $1.25. The extra 25 cents essentially represents the optionality value.

Thank you

How do you interpret a 50 vol, in layman’s terms?

Feels like another good reason for freely traded STOs.

Curious as to why this “market” for financing options hasn’t happened. If people like you and other VC firms see the value – wouldn’t you guys be the very ones funding such a startup market?Would this market be pure financing, or taking some financial stake in the options themselves? I apologize if you have already posted the details somewhere else. If it is purely fee-based financing it seems like a no-brainer.

These markets do exist but they’re small and disparate. A few people posted last week that they’re working on new companies to compete in this space. Secondary markets are typically available to high-net worth individuals through private wealth management companies or investment clubs. Because these are private and secondary transactions, financial reporting is scant. Caveat emptor. What could change this faster than a crypto-market? Someone who is close to the big tech companies on 2019/2020 IPO tract to launch a marketplace for secondary shares in those companies. That would presumably interest enough people that you could attain a minimum threshold to sustain the marketplace beyond the handful of name-brand private companies.A big BUT to the above is the financial reporting requirement. I saw a private offering for Uber through the high-net worth / private wealth management tract that contained no useful financial information. Further, WeWork invented a performance metric (community ebitda). You can’t just make the books available to solve financial disclosure issues. As another practical matter, the SEC has no ability to monitor this. They don’t have the manpower or the sophistication. This comes from personal experience.So, maybe the answer is that you have to create a blockchain market that NewCos issue stock on from the start so that you could enforce a standard of corporate reporting that would allow for this type of market.

I work for one of these companies that offer financing for options. We were started in 2012 because of this exact issue, however, the business is not easy and there are a lot of risks. We typically help employees exercise so that they own their shares. If the company fails, we take the loss. If the company succeeds, we share the upside. While later stage companies are less risky, common shareholders are the most at risk of getting nothing as the shares the VCs own get a liquidation preference for the lesser outcomes. I don’t believe the risk-reward trade-off works for a fixed fee-based financing as the underlying shares are extremely risky and illiquid.

That is exactly what I would have expected the structure to be. Makes sense and now I see the risk/reward issue. You essentially are a mutual-fund of shares in these various companies with dramatic downsides and upsides. If the preferred shareholders (like AVC) really want a market for this maybe they should help defer the risk in the interest of “the little guy.”

“…the shares the VCs own get a liquidation preference…”Exactly the kind of condition that threatens togetherness.

There are quite a few companies offering the startups funding options for their employees options. The problem currently is that those companies are very early and the process it time consuming for the startups. I would assume this will get worked out however.I too agree that this method is the best.But in the meantime, until these services become mature. Doing the right thing is better than leaving your employees / former employees out in the cold. They sacrificed.Recap.. the mechanisms are there to solve this problem today. Let’s do the right thing. As well as work with those funding companies to make the UX better for the founders of startups.

I’ve been trying to put together an article with a different methodology to value warrants/options on startups, using the fact that startup returns are typically more power-law than lognormal distributions. Still WIP, but thought was mildly relevant to the conversation here, and hopefully to get some early feedback from the interested community.Thanks a lot in advance!Best,Juanhttps://juanmontalvo.me/warrants_valuation_v1

Why use 50 as the vol?Is that like saying there’s a 50/50 chance the option will be in the money at expiration date? Any rules of thumbs you like to use for the vol? I’m not a finance guy, just looking for rule of thumb shortcuts and what vol means in simple simple terms.

There is the huge flaw in using the Black Scholes model in this case. Yes I aced Fin6 for those who know what that class is”Recent financing at $2/share”Now under Black Scholes this means that you in fact could sell your shares for $2.You are correct that if you had a separate market you could imply that value and volatility.But that financing at $2 a share had many conditions. There were terms, and there were a certain (large) number of shares sold. So that input $2 is completely incorrect because you cannot sell a small amount of shares for that number, same with the volatility which you can’t measure the Beta on because there are not thousands of points there are less than I can use one hand to count.So in Engineering terms you have to use significant figures meaning that your result cannot be more precise than the least precise number. This is a very common mistake people use when using tools like excel which allow you to calculate to the penny.Not arguing the overall point, but arguing the math.I would argue that there is also an implied contract when people take options that for that huge effort they put in the first year, and the risk they took changing jobs no matter what they should receive them. That is certainly not correct and not what the contract says, but I am telling you from talking to tons of people that have taken options and have had them not work out, and their bitterness it is the case.Right or wrong.

This is definitely a dumb question, but when you said “you cannot sell a small # of shares…”, wouldn’t the company being buying the shares, thus the # irrelevant?Is 50 a common vol to use when you have no friggin idea what the future holds for the option value?

There is an old saying – “All models are wrong, but some models are useful”.Black-Scholes makes many assumptions…besides the ones on efficient markets and no transaction costs on purchase, there are two key assumptions in the model which are not real – 1. That the vol is known and remains constant over the entire period and 2. The underlying asset returns follow a normal distribution.(Also, that the risk free rate remains constant during the period).Despite the above assumptions, one could find use for it in traded markets and real world traders say they use it only with tweaks. And used reversibly to calculate implied volatility.But I agree that it is a bridge too far to assume it for privately held options using the recent financing price as the market price. Those pesky little things called “terms”. And no historical volatility.

Ah can get the “normal”, i.e., Gaussian, distribution assumption from the central limit theorem and an assumption that have a suitable independent increments process, if believe in one of those! So, in particular can get the assumptions via a Brownian motion assumption! Some guys at a firm Long Term Capital Management believed in that stuff, believed that their highly leveraged position was safe, and shot much of the world financial market in the gut!Black-Scholes is an especially simple case of stochastic optimal control, the subject of my Ph.D. research, and is a exercise in stochastic differential equations, e.g., in the back of (with TeX markup to keep the German correct!)K. L. Chung and R. J. Williams, {it Introduction to Stochastic Integration, Second Edition,/} ISBN 0-8176-3386-3, Birkha”user, Boston, 1990. Ah, one of the prerequisites is a background in probability theory and stochastic processes based on measure theory, now long the only way the real pros do it!There is more for exotic options via the Brownian motion solution to the Dirichlet problem with lots of quite technical details in the now classic (with some more TeX markup — the way I keep it in my notes)Robert M. Blumenthal and Ronald K. Getoor, {it Markov Processes and Potential Theory,/} Dover Publications, ISBN-13: 978-0-486-46263-9, Mineola, New York, 1969.E.g., get a lot of practice with the strong Markov property — that it remains Markov even with stopping times, when to stop measurable with respect to the history of the process, i.e., adapted to the current of sigma algebras that is the history.What measure theory does with that material is astounding, and trying without measure theory is just hopeless.Disclosure: That pure math, as amazing as it is, is not the pure math foundation of my startup!Of course, stochastic optimal control is best decision making over time under uncertainty, that is, a case of optimization, and Black-Scholes is a special case looking for a stopping time of when to close out the position. I still have a nice letter from Black saying that he saw no opportunities for optimization on Wall Street!Using Black-Scholes in accounting? Formality over reality and not for the first time.Instead of struggling with all these options, vesting, exercising, accounting, etc. issues, it sounds to me like a person really deserving of stock options should just be founder and 100% owner of their own company. Get an ordinary job 9-5; do the startup on the side, i.e., have some good ideas and write the code; stay away from women; quit the job and be successful with the startup; and THEN find a GREAT girl and right away get her married, e.g., as in the fully traditional, near fantasy,https://www.youtube.com/wat…and pregnant, and maybe not in that order, and KEEP her having babies until she has several, is home schooling them, working hard on academic, artistic, athletic, creative, emotional, empathetic, entrepreneurial, ethical, mechanical, moral, psychological, quantitative, rational, religious, romantic, scientific, social, technical, verbal, etc. childhood development, and is 100% 24 x 7 wrapped up in love, home, family, and being good as a wife and mother. And try as best to keep her far away from anything like feminism.That’s what I started out doing, but too soon I met a girl sayingWomen don’t have just to be cared for. Women and do things, too. I want a career.She was brilliant: She and her family looked like something out of a Norman Rockwell painting of the ideal US Midwestern farm family.But we were both wrong, badly wrong. It did big damage to my career and life and was fatal for her.It wasn’t me: Later it became clear that the situation was quite similar for her mother and two sisters.At the beginning would have had to have been darned good at clinical psychology to have seen it.All four of those women, in their late teens, looked terrific, but they all had debilitating problems that, for three of them, did have some reproductive advantage.Men, what you would commonly think of as just debilitating to Darwin can look like reproductive advantage.Lesson to men: Do NOT bet on her career.Some men were lucky, found a really nice girl, pretty, healthy, nice, in three months got married, and did well with family, etc. for decades “’till death do we part”.But there are risks trying that.Where can I apply for a do-over?

See my point to Charlie. In the wrong hands people will use this with employees and say 50,000 share options are worth $65k today. Want to take a $50k pay cut for that?

I think this post somewhat oversimplifies the accounting (and business) questions related to stock option exercise periods.Almost every stock option issued by a startup has a full 10-year exercise period. I’m sure there are exceptions but I think they’re quite rare.Most stock option agreements have a clause stating that, if continuous service ends for the employee, *at that point* they have 90 days to exercise or else they forfeit the options. I strongly suspect the historical reason for this common provision is the tax code – this acceleration of the exercise period upon termination is one of the requirements for an option to qualify as an ISO instead of an NQSO.Stock option agreements also of course contain vesting provisions, separate from exercise provisions, which determine what you have to do to actually earn the option (regardless of whether you go on to exercise it). The most common vesting provisions are, say, “the options vest 25% after one year, and monthly thereafter through the four year anniversary of the grant.”The accounting rules for stock options require you to make adjustments for anticipated forfeiture rates and exercise periods, which are a function of how many employees you expect will leave before they vest, and how many employees will forfeit options rather than exercising them. The accounting cost (“black scholes value”) of compensation expense for a stock option grant is driven by these assumptions – lower forfeiture rates will result in longer expected duration and higher expense.The solution Fred is referring to as “extending exercise periods” really doesn’t mean changing the exercise period of the option – as I’ve said, in the vast majority of cases the contractual exercise period is 10 years so long as you’re employed. Rather it involves removing the contractual 90 day forfeiture provision upon termination of continuous service, *for vested options only.*This means that for many options there’s no change in what happens – if you leave before you vest into an option it’s forfeited regardless, for example.A typical assumption about an option with normal exercise restrictions and vesting (ten-year term, four year vesting, 90 day termination) might be accounted for with a black scholes duration of 6.25 years, for example – less than 10 because of various expected forfeitures. Whether a modification of the option to eliminate the 90-day termination provision would change this assumption is a question for your auditors – and depends on whether the original estimate was dominated by forfeiture of unvested options or by forfeiture of vested but unexercised options post termination. I believe in many cases there is no modification to SBC expense from making this change, but it will vary circumstance by circumstance.A few other points are worth noting:- In general, SBC expense is accounted for at the time of vesting. So a black scholes calculation is made at the time of grant, and the expense is smoothed out over four years (for a normal option on the terms above). Even for forfeited options later you may not “get back” the expense, so you may not actually from an accounting perspective ‘benefit’ from the post-termination forfeiture/expiration of vested options.- Economically, I am not sure an investor is actually any better off if there’s a secondary private market for employee exercises vs. an exercise period extension. Depending on how the marketplace works, in either case the employee will eventually exercise the option, converting it to a share that dilutes other investors. So I’m not sure practically there *should* be any accounting difference between these scenarios – if you knew the market for post-termination exercises was liquid your black scholes duration estimate should change in approximately the same way.None of this is to say what’s best for attracting or retaining employees – I don’t know whether the average employee would prefer to be forced to exercise into a secondary market on termination, or be able to wait and hold the option for a longer duration. It sort of depends on the nature of secondary market and your best guess for where the share price is headed…

This is truly an amazing comment and gets to the heart of the problem:The industry has built up a valuation model that is based on the hidden assumption that many vested options will be forfeited. From first principles it is hard to justify that forfeiture, so when people try to suggest fixing it the only way to oppose that is to obfuscate.

I guess I’m not 100% sure that’s how I’d look at it. The options have some value in the world, and any employee needs to determine for themselves what that equity is worth – probably not by using Black Scholes, but by thinking critically about the business and what’s realistic.The accounting standards, including the assumptions that go into Black Scholes, are designed to most accurately reflect “what will happen” with these options. The idea is that companies have to report – to their investors, to the tax authorities, etc – how much they spend on stock based compensation, and “how much you spend on stock based compensation” is actually a complicated and subjective question. So Black Scholes is a sort of “do the best we can” standard model for getting there, and incorporates our best estimates about actual forfeitures in the real world.It’s probably clear from my post I am generally an advocate for having long exercise periods after termination for vested options specifically, but I think Fred’s solution (a marketplace) might serve a similar purpose.It’s also worth noting that in many cases people exercise their options much earlier, even before they vest, because it can be tax beneficial to do so – and obviously those people are under no obligation to “use it or lost it” with respect to their vested equity when they leave. Nor are recipients of two-trigger RSUs who have satisfied the time-based vesting conditions, nor are recipients of restricted stock (most of whom will have taken 83b elections and covered their tax bill early).

Is it usual or possible that an employee exercise his/her vested options before the full vesting period? Are vested options transferable?

Ask the CEO and the employees what the “Greeks” are? If they come back with with answer about immigration and asymmilation, you’ve got a problem.

I agree it’s good to understand the added cost to the company, but this has always seemed besides the point to me if ultimately employees see stock as being earned for their work put in upon vesting, not after some add’l step when they have to make a decision to ‘for realz’ buy their stock in some arbitrary time window. I’ve always disliked that companies effectively use an IRS quirk to force employees to make that decision within 90 days. Using the full 10 year life isnt perfect but better, and if that means the BS-value goes up a bit, it seems like that should just be accounted for ahead of time. In your example, I believe most employees intuitively feel that shares they earn should be worth the full $2 (which is why its definitely important to explain exercise/strike price upfront). So comparing to that, $1.52 is still a significant discount, and it would be nice if investors looked at it from that perspective instead of fretting about things like overhang that wouldnt even be relevant if the IRS had its shit together on how they treat stock based comp. I get why they do, esp when big numbers involved, but it all just seems like cap table space that shouldn’t even come back into play anyway if the system weren’t screwed up. Tell me what I’ve gotten wrong?

I have to say I never understand the thinking behind carrying the cost of options on a startup’s books. First, there is no reasonable way to quantitatively estimate the risks of a startup. Second, dilutive equity issuance results in reduced earnings per share, and hence per share price. In a way, its cost is already reflected. I understand that accounting principles are supposed to reflect all costs associated with providing/manufacturing/managing a business. But there has to be a limit to it. When the compensation comes out of the company’s pocket, it should be recorded. When it comes out of the shareholder’s pocket, it is captured else where (i.e. stock price). I don’t see the point of trying to build all-encompassing accounting principles which only make things so complicated. The end result is people start using adjusted earnings/EBITDA instead of looking at the reported net income.

Quick practical experience as a twice early startup employee: options have yielded zero wealth for me. Only work for fully vested shares in lieu of income or cash unless you are a founder, in which case you are working for fully vested shares.In one case investors with preferred shares and a lower end exit zeroed my options out.In the other case paying for the options and paying taxes on the options for a quickly growing startup would have cost me several years of earnings and it was out of my reach and risk zone.

Another reason to exercise an ISO is to more quickly meet the holding period requirements needed for long term capital gains treatment. https://www.mystockoptions…. “For all capital gains at sale to be taxed at favorable long-term rates, you must hold your ISO shares for at least two years from the date of your option grant and at least one year from the date of option exercise. The full gain over the exercise price is then all capital gain.”

And even another reason for “early exercise” (exercise when granted, with a buyback provision of any unvested shares when you leave) of your unvested ISOs is to avoid being exposed to AMT on the spread because the exercise price = FMV on the grant day.I know that early exercise is not that common, probably only available to exec hires if it is even offered, and of course, this means betting the ISOs will be in the money when you can finally sell them.

I think another way of looking at it is, a company generates a set amount of “value” at exit. If you offer an open exercise period, you’re giving them a higher chance of getting a piece of that “value” at exit. However, at exit, it is a 0 sum game where if an earlier employee who no longer works at the company gets a portion, the other shareholders get less. While I agree that early employees earned the options, by extending the exercise period, you’re giving them more value which is what Fred Wilson is trying to quantify.

I am with you.The cost appears to be slightly annoyed future financiers.

My comment seems to have been marked as “spam.” I’m not sure why. Ahh well…

Not just Myron Scholes, they had Robert Merton as well who had shared the Nobel prize with Scholes in 1997…only 1 year before LTCM’s collapse (Fisher Black had died and was not eligible for the Nobel).There is a telling episode in Lowenstein’s book, When Genius Failed. Meriwether is trying to raise money as LTCM is unravelling and visits an old friend who was his first contact at Bear Stearns – ““Where are you?” Mattone asked bluntly. “We’re down by half,” Meriwether said. “”You’re finished,” Mattone replied, as if this conclusion needed no explanation.For the first time, Meriwether sounded worried. “What are you talking about? We still have two billion. We have half—we have Soros.” Mattone smiled sadly. “When you’re down by half, people figure you can go down all the way. They’re going to push the market against you. They’re not going to roll [refinance] your trades.You’re finished.””

I mentioned LTCM precisely because Scholes was a principal. Roger Lowenstein’s account of LTCM is a canonical book in mis understanding risk and management style drift.

The comment to which you responded. I didn’t think it was particularly spammy…

Completely agree! Fred’s point though is the same option package with different exercise periods are actually worth different amounts. As he notes, the value difference could be quite large from 20-50% and employees would balk if the options package was reduced by 20-50% in order to make the “value” of the option packages the same.

I still have a nice letter from Black saying that he saw no role for optimization on Wall Street! I wonder if James Simons would go along with that!

My point is simply this. People will use this to calculate the value of their options and that is wrong. I don’t disagree with the direction. Longer time equals more value. Although again in the case of venture many/most go to zero.

Yup!