The IPO Price and the S1

In my What Is Going To Happen In 2019 post, I wrote:

I expect we will see IPOs from big names like Uber/Lyft/Slack, although I also expect those deals will get priced well below the lofty expectations they have in mind right now. Some of that will be because of weak equity markets in the US, but it is also true that most of the IPOs in 2018 also priced below the lofty “going in” expectations of founders, managers, boards, and their bankers. The public markets have been much more sanguine about value than the late stage private markets for a long time now.

And now we are starting to get the data from these IPOs. Lyft is on the road raising roughly $2bn at a post-deal valuation range of $16bn to $20bn ($62 to $68 per share).

When I see an IPO price range, I like to go look at the S1 that the issuer has filed with the SEC prior to the road show. Here is Lyft’s S1.

Here are the things I like to look for in a S1:

1/ The total shares outstanding. You can go to the table of contents of the S1 and look for the section called “Description Of Capital Stock”. In Lyft’s S1, it says there are ~240mm shares of Class A common stock plus some amount of Class B common that is not yet detailed. The Bloomberg article I linked to above says the company is going to sell 30.8mm shares at $62 to $68 per share. So there will be at least 270mm shares outstanding plus the Class B shares. The Bloomberg folks seem to be using a post deal share count of 288mm share so that is close enough. You get to fully diluted post deal valuation by multiplying the share count (288mm) by the range ($62/share to $68/share).

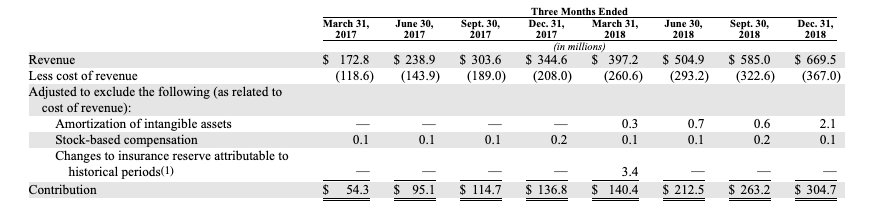

2/ Revenues and earnings/losses. You can go to the table of contents of the S1 and look for the section called “Selected Consolidated Financial And Other Data” and you will find the audited financial data. I like to find the quarterly numbers because that will give you a good idea of current growth rates. These are the numbers for Lyft:

As you can see the quarterly revenues are growing at roughly $80mm a quarter so a back of the envelope guess on revenues for 2019 are [$750mm, $830mm, $910mm, $990mm] for a total of ~$3.5bn, up from $2.1bn in 2018 (yoy growth of 65%).

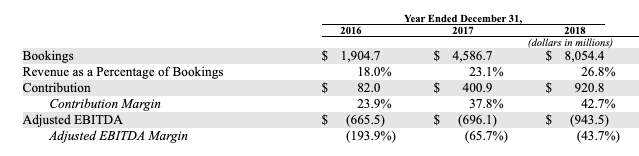

You can also see that the contribution (net of cost of goods sold) has been about 45% over the past few quarters so if that ratio holds in 2019, there would be contribution of roughly $1.6bn in 2019.

For the operating costs, you can look at the difference between contribution and EBITDA, which you can see here:

Lyft spent ~$1.85bn on opex in 2019 ($921mm of contribution plus $943mm of EBITDA losses). That number grew from $1.1bn in 2017. I would expect Lyft’s operating expenses to be at least $2.25bn to $2.5bn in 2019.

Which gets you to this possible P&L for 2019:

Revenues – $3.5bn

Gross Margin – $1.6bn

EBITDA (loss) – $600mm to $900mm

3/ Valuation Ratios:

At the mid-point of the offering range $18bn, the price to revenue multiple is roughly 5x (18/3.5) and the multiple of gross margin (what Lyft keeps after paying significant COGS) is roughly 11x (18/1.6).

4/ Time to cash flow breakeven. This is harder because you have to make some assumptions about growth rates beyond 2019 and opex growth rates. But if Lyft can grow revenues at 60% per annum for a few more years and keep opex growth rates to 25-30% per annum, then it could get profitable by sometime in 2021. This suggests that the $2bn it is raising may be sufficient to get profitable, but it will be close.

So what does this mean for other late stage high growth high flyers?

To me it says if you have company focused on a big opportunity (like transportation) that is growing at north of 60% per year it is worth in the range of 10-12x net revenues to wall street right now. Because Lyft only keeps about 45% of its revenues after very high COGS, that works out to be 5x revenues.

Many late stage private companies are getting financed at valuation ratios in excess of this so they will have to grow into their eventual public market valuations. But that has been the case for quite a while now as the late stage private markets continue to pay higher prices for high growth companies than the public markets do.

Comments (Archived):

yup, always a moving target. Based on where we invest, I always look at multiples of top line revenue. It’s all over the map, and based on the demand for what the business is doing. Seen 3-5x, and seen 20x…crazy.I do think that Lyft was smart to go out. It’s going to set valuations for other private companies as you say in your post.

Here is an interesting “empirical” analysis from (caveat) my friends Prof Fader and McCarthy, interesting reading! They believe that if you run out the long term economics, these valuations make no sensehttps://www.thetaequity.com…

Useful–thanks Fred.I’m glad to see Lyft going out.

Master class in a nutshell, thank you.A question that instantly arises is who will exit through the IPO.What is the best place to look for an “exit map”?

Am curious why you are considering the Contribution margin as the Net Revenue.For instance, the numbers I am looking at for 2018:Bookings – $8.05 Billion.Revenue – $2.15 Billion.Contribution Margin – $920.8 Million.Isn’t the $2.15 Billion (assumed to grow to $3.5 Billion for 2019) the Net revenue ?

In most cases I’d agree with you. In this case, I view bookings as a fungible number because in many cases Uber/LYFT pays the driver more than the advertised cost of the fare. Bookings may be the retail equivalent of the markup to discount, or it may be a pass-through dollar amount. I have seen many rides where my app says the fare is X, I see the driver’s app which says the fare is Y, and Y > X. Lyft’s consolidated operating statement begins with Revenue so it looks like they view bookings in a similar manner (Bookings may be better related to number of rides as opposed to revenue).Further complication Rev -> Gross Profit is the note that Lyft shows rider incentives in S&M and not COGS (driver incentives are in COGS). Going by 2018’s numbers, the 42% gross profit (i.e. net revenue) is likely lower.

Edit: Maybe Fred can clarify.

I think we’re saying the same thing using different terms. I’m looking at F-4 from Lyft’s S-1 (link at end). The top line of Revenue is $2.15B. Your first comment pondered if $2.15B is Net Revenue. Maybe that was a typo since you then state it’s Revenue. The next line is cost of revenue (aka COGS), which is $1.2B. I calculate gross profit as Rev – COGS. Page 17 (Other Key Business and Non-GAAP Metrics) shows contribution margin, which is a % of Revenue, which is a % of Bookings. That’s a similar definition to Gross Profit and they caveat it based on the information below.Something interesting about Lyft’s definition of contribution (p. 85) is that they point out it excludes: (1) amortization of intangible assets; (2) stock-based compensation expense; and (3) changes to the insurance reserve attributable to historical period. The actual adjustments to GAAP are de minimis (p.86). Is Lyft’s use of Contribution due to them being in the taxi business? It’s not a metric I’m familiar with.Since the non-GAAP adjustments are < 1%, Contribution Margin is equivalent to Gross Margin.https://www.sec.gov/Archive…

Just saw the edit. TL:DR my comment below. I am not familiar with Contribution as a financial metric, and I read about it for the first time in Lyft’s S-1. In Lyft’s case, it’s virtually the same as Gross Profit.

Yup, “bookings” and “contribution” — undefined terminology for me!

Contribution margin has been around a few years. It is taking the allocation of fixed costs out of the COGS bucket, and adding back in the variable selling costs. It was supposed to help you get a better handle of unit economics.It is useful if you want to look at profitability by line of business or product line.Contribution margin quoted is usually a little better than gross margin.(doesn’t have to be, depends on variable selling cost you add back in).Bucketing questions arise. But if you do it correctly, it does let you identify instances of a product with negative gross margin but positive contribution margin (thereby helping in allocation of fixed cost on a larger base)

I tried to read the S1 and Fred’s summary: I ran into, in simple terms, undefined terminology. Good to see that some others don’t have good definitions for all the terminology either!

yes, you are correctrevenues are net of driver costsi wonder what is in the 55% COGS

It’s the massive insurance costs!

P. 95 of S-1 looks like as close as the S-1 gets to bracketing the costs. 2017 Compared to 2018 Cost of revenue increased $583.9 million, or 89%, in the year ended December 31, 2018 compared to the prior year. This increase was primarily due to an increase of $318.5 million in insurance costs, an increase of $109.6 million in payment processing fees and an increase of $74.9 million in hosting and platform-related technology costs, all of which were driven by significant growth in the number of Rides.

i updated the postthanks for correcting me

Thanks. As I mentioned in my comment to @TomLabus:disqus yesterday, I was looking at the revenue multiple in the context of Uber’s IPO.If Lyft’s net revenue multiple is ~ 5X (and not 10-12X), and since Uber’s revenue for 2018 is $11.3 billion (& if you back of envelope guess $14.X billion next year), Uber’s rumored target IPO valuation of $120 billion will be a challenge.Uber will argue that they are a different company and command a higher revenue multiple than Lyft. But, on the other hand, Uber’s growth is slowing (on a higher base) relative to Lyft. Full-year growth was 43%, but more front-ended last year..Q3 slowed to 38 % (y/y) and Q4 to 25% (y/y).Since both companies are losing a lot of money, the quarterly revenue growth trajectory will matter, and slowing revenue growth in a highly unprofitable business might challenge the revenue multiple premium that Uber will be able to get over Lyft.

I polled my network and read about Contribution. Total Rev – Var. Exp = Contribution. The devil’s in the details on this one as I can how you classify costs as fixed or variable depending on your view or how aggressively you may want to report your contribution margin. In Lyft’s case, they disclosed on p 92 that “rider incentives and refunds” are included in Sales & Marketing. That’s up for debate.Good article on Contribution below.https://hbr.org/2017/10/con…

Yup.

Wow. Thank you for the detailed analysis Fred. It’s appreciated.

Is this down to headline prices versus terms? So the late stage VCs are paying up for the headline figure, but with ratchets and liquidation preferences that protect some of their downside?

LYFT. I like this IPO. 39% market share. Labor costs and a difficult NYC market will make it hard to control costs which they “assume” for 2021 profit. Less noise than uber too! Will take a flyer.

You have to wonder how Uber will get to their rumored target valuation for their IPO. By my calculation, this Lyft valuation band is ~ 5X of net revenues, not the 10-12X of net revenue that Fred mentions (per my other comment).

The magic of banking!! Market can turn a blind eye when it wants to. I’ll wait a bit to see how their pubic reception goes.

“Magic of banking” reminds me that a characteristically witty description of this capitalization magic is in the 1972 book Supermoney by Adam Smith (George Goodman). That magic money is what he alludes to as “super”money.You might have read it, but in case you haven’t, highly recommend. I have two hard copies of it, plus a Kindle version 🙂

He was great!!! Talk about clarity of thought.

Fred, thank you for an outstanding analysis that I have shared with my class. I also think it is good to see Lyft going out as we will get more transparency into the market, the company and the validity of the assumptions being used to build the case for a lofty valuation. Having started in 2012, Lyft is a relative youngster in this space as compared to Uber which started in 2009. The big questions will be continued market growth and expansion and the CAC relative to the CLTV for both companies. As we have seen with other recent IPOs the air can easily get let out of the balloon if targets aren’t achieved and the public market’s trust in the team and the story of future profitability.

Great post. Always fun to see your back of the napkin snapshot.If their customers are the drivers, was there any break out on driver production curves?If they spend $2B chasing the long tail of low producing drivers, they are going broke FOUR SHORE as the say in Cap Pele.

No stock based compensation is baked into the numbers. This is not an inconsequential expense. Per the S-1: “If this offering had been completed on December 31, 2018, we would have recorded $684.8 million of cumulative stock-based compensation expense related to the RSUs on that date, and an additional $643.2 million of unrecognizedstock-based compensation expense related to the RSUs, net of estimated forfeitures.”With RSU compensation included, the company’s net loss would grow to 1.6B, a 75% increase over the stated 2018 net loss of 911M.

Curious how many ride share users check Lyft vs. Uber pricing before ordering a car? I do pretty much every time (more out of curiousity than anything else). Ride share is a commodity biz. Loyalty isn’t strongly baked into the model, particularly when you have so many drivers working for both services. Lyft is aggressive w/ promo discounts for loyal users, which is a good thing, but it has to create some havoc w/ their margins.

I don’t check. I had too many Lyft rides where their map was completely off. Uber has been more consistent in showing the accurate pick up and drop off points.

Maybe we begin to see again that that taxicab business is nearly all just a LOCAL business. A taxi or motorcycle driver in Saigon can know the streets, hour by hour, “like the back of their hand” (a joke on an old NYC claim) even if the computers back at Uber/Lyft don’t.

Google maps displays this at a glance very clearly when you’re in a location that has both services, assuming your phone is set up correctly.Here in Southeast Asia, it’s displaying the local incumbents’ real-time offerings (which also include motorcycle transportation) along with waiting times, prices etc.

I see that now. Never realized you can do that directly from Google maps. Thx.

A16Z: “Hey, TK…F.U.”Go get em Lyft!!!

Thanks Fred for walking us through the logic of your analysis. With many of these late stage IPO’s, do you believe that much of the value is already priced into the offering and therefore we may see more negative or moderate price growth? “Many late stage private companies are getting financed at valuation ratios in excess of this so they will have to grow into their eventual public market valuations.”, and therefore future performance will be the deciding factor, e.g SNAP. Mark Cuban has advocated late stage IPO’s as hurting investors and the economy because so much of the value has already been taken out of the company before it becomes public. Is the move to IPO therefore simply about creating liquidity for existing investors?

Don’t overlook the balance sheet. Are they carrying debt? So few of these companies tested in a recession. Little pricing power.

That’s a LOT of company value and a lot of revenue but in every sense a LOT of losses. And in those losses there is a LOT of overhead, e.g., research and development, marketing and sales, and more.They are basically in the taxicab business: I know; I know; I just looked it up: They are in the ridesharing taxicab business.Q 1. Is there really any chance they could make money, that is, without charging more then traditional taxicabs?Q 2. Is there any chance they could make money against the “ridesharing” competition?Q 3. The situation smells like someone is all fired up about some great efficiencies from the “ridesharing”: Is there much evidence that the efficiencies both exist and are significant?Q 4. Doing well at the accepting of ride requests looks like an operations research problem, with a lot of discreteness, e.g., the little version of the traveling salesman problem, and a lot of probabilistic and statistical content.Q 5. Is the operations research the key to the dreamed of efficiencies? I can claim to have a good background in the math of operations research, but my experience is that US business does much better at finding hens’ teeth than finding good solutions to operations research problems. Are the ridesharing operations research people well qualified, e.g., know what they are doing? Have they gotten anything significant?Q 6. Uh, the ridesharing companies are not so totally brain dead stupid they try to do that work with computer science are they?Without a careful look, I couldn’t say that operations research could make much of a contribution. But: (A) Operations research (OR) has been a fairly serious field back to WWII. (B) The best of OR is some quite good stuff with some darned valuable applications done. (C) Most of the best of OR is some quite will done math, quite careful proofs. (D) In the good math of OR, there are some surprising results potentially very powerful in practice. (E) No way will people with just a computer science background, or physics, electronic engineering, etc. reinvent or quickly learn these results. (F) When can make a good applications of the more powerful results, can make a big BUNDLE of money and totally blow the doors off, totally blow out of the water, approaches with just computer science or other fields without the results. E.g., here’s one that might pay off: In accepting the current ride request, what is the probability of three more such requests in the next 15 seconds? How the heck to make any sense out of this? Collect a lot of empirical data, conditioned on city, part of the city, time of day, and build an empirical distribution? Or: The arrivals in the next 15 seconds are a continuous time, discrete valued stochastic process. Under shockingly mild assumptions, it’s exactly a Poisson process, and from that lots of super good information follows right away and needs only some quite simple arithmetic. So, get to play the odds, say, card counting at the blackjack table. That’s one — at the top of the stack, there are dozens more. Deeper, there are hundreds. Deeper still, can stir up more.The traveling salesman problem? Okay, but in Euclidean spaces? That’s different! There a special case is, sure, the plane, or just city streets. There’s some super cute, powerful stuff known, tough to discover, not easy to prove, but already known.Limitations on what can do, that is, constraints? Linear constraints are common in practice and often good approximations to non-linear constraints. What is known about linear constraints, that is powerful, is mind blowing stuff, with some just elegant proofs. Got to be pretty good and work hard to understand much of this; for one person to reinvent all this quickly or even at all? No hope. Not many people have much understanding of linear constraints or optimization subject to linear constraints: The pure math departments have some of the most important prerequisites but nearly never follow through — and just the prerequisites are not enough; to get the value, have to study the actual material. Really about the only place to get this material is some department of operations research, systems analysis, mathematical sciences, etc., and the number of good departments is SMALL.

This IPO is an amazing story when you consider:1- Travis Kalanick had an opportunity to acquire Lyft at a cost of ~16% of Uber’s stock, if memory serves, but declined in favor of trying to put them out of business.2- His audacious bet was looking like it was going to pay off – Lyft was reportedly having trouble raising its next round of funding and reportedly were at risk of shutting down – when Uber’s incredible self-own happened, with the negative press around company culture etc, causing a resurgence in customer interest in Lyft. That was followed by Lyft signing an agreement with Google/Waymo, and suddently Lyft became the way to place a bet on a future of self-driving transportation services, and thereafter had no problems raising capital….leading us to today.

So, THAT’S part of the interest in Lyft: Artificial intelligence, Waymo, and self driving.Also pay with crypto tokens?Might the IRS eventually suspect that a lot of buying and selling with crypto is avoiding some taxes? So, maybe a driver gets paid with crypto, then pays his rent with crypto, buys groceries with crypto, and never reports the crypto he got paid as taxable income? The guy who receives the rent in crypto uses that crypto to buy groceries, taxi rides, washing machine repairs, exterior house painting, etc.? Then crypto is a substitute for the cash economy where maybe some people avoid taxes. IIRC the IRS tries to crack down on using lots of cash, e.g., bank deposits over $10,000 at a time, and might try the same for crypto.I know; I know; a stock is worth what can sell it for, that is, what a buyer will pay for it.Ah, once I read a book about the 1890s and the stock market: There was a lot of fluff there, some having to do with railroads, coal, coke, etc. Okay, we lived through that one!

Are the drivers actually making a sustainable living from such companies, or is the apparent viability of such companies hiding huge ‘churn’ in driver participation? The model looks suspect to me.

I always enjoy talking to the drivers and hearing about their business. One driver noted she had made 40k the previous year and really liked it versus working inside at a pharmacy. Yet she also noted she put 40,000 miles on her vehicle.So she got cash in- but after all is said and done (vehicle depreciation, etc.), what did she make?I think it’s a nice quick hit of cash for drivers- yet the cost hits them hard as time goes by and they are really not making much at all (and this won’t last).

I think so. At this stage Lyft (and Uber) are nothing without the drivers, but may become everything without the drivers further down the road. Deeply ironic.The IPO is either a quick flip proposition, or a long hold proposition, depending on how shallow or deep the trousering pockets are.

Good points. Quick flip will be popular on this one.

The late stage private funding sector is driven by bankers, late stage funds, ultra high net worth investors and greed, with expectations of flipping as soon as the stock is public. Some people make a lot of money in this weird phase that’s like a club to get access to.

All investment is driven by personal gain.Is that your definition of greed?

True, but this phase is weird because it’s all cooked and returns happen in a short time.

Yup, its a word that will never transcend the movie line it exists in forever, so I usually avoid it.Too much work to find an unattached meaning for it.See ya in NY in the Spring.

What was the old year 1999, VC, high first day pop, startup, stock market bubble comment? IIRC it went something like:Never be between a VC and the door when the lockup period is over.I didn’t just look this up to check it and might be wrong!!Big bucks in the taxicab business, who’d a thunk? I know; I know; the biggie difference from the old taxicab business is smartphones, good street maps, complete with traffic lights, hour by hour historical traffic densities, minute by minute data on traffic jams, terrific operations research (OR) work on which ride shares to accept, lots of communications back to a central server farm for the historical data, real time data, and OR solutions, etc. and with that can build a company worth tens of $billions?The revenue is significant and growing quickly, but the losses are huge. Yes, maybe the losses are growing slower, in billions per year, percent per year, and fraction of revenue, than the revenue so that after a few more years of big jumps in annual revenue the company will have juicy pre-tax earnings.Hmm ….All in the taxicab business???

Thanks for sharing this analysis. I predicted back in December when the private S-1 came out that the unit economics of Lyft might end up looking much better than those of Uber (due to higher marketplace liquidity in the US and less noise from geographic expansion). I made this short video about the topic back then (https://youtu.be/Wa9uzVYA4K8). The gist was that network effects had been oversold.Now one thing that’s interesting for me to look at is how the P/S multiple fares compared to FAANG and other public marketplacesAs mentioned, Lyft is at c. 5x top line (at mid pricing range).FAANGFB: c. 8.5xAlphabet: 6.5xAmazon: 3.7xApple: 3.5xNetflix: 10xMarketplaces:Grubhub: 7xEtsy: 14xAlthough sales means something very different when you look at the different business, I prefer to look at P/S ratios over P/E, because top line is a metric that is less susceptible to accounting treatment

I suspect the unit economics vary dramatically by geo based on age and scale.This applies to all the on-demand startups (Uber, Postmates, Wag, etc) and likely makes them look better from the inside than the outside.From the inside, you can likely see very strong unit economics in good geos and you can see investment in newer/smaller geos.Most importantly, you can probably see that a business like Lyft has more control over burn then the overall picture implies as they could dial down investment in weaker geos and see the overall picture improve significantly.While dialing down in poor geos might hurt growth, it’s a safe bet that even mature geos have plenty of growth left as we are in early innings of urban folks selling cars and doing other things to boost their usage.I’m not saying Lyft deserves to be valued for a particularly high multiple of revenue, but I’m sure there will be plenty of naysayers knocking their valuation who don’t consider the underlying geo dynamics.FWIW, I sold my car 6 months ago and can only imagine I’m a very attractive LTV user.

Hey Fred, I agree with your shares outstanding and your post-money valuation and even the S-1 says 288M shares outstanding “after the offering” (post-money). Everyone from WSJ to CNBC keeps quoting $23B post-money valuation and even goes on to say “equates to 62-68 share price. This would equate to 338M shares outstanding? Really bad reporting or are we missing something?

This was insightful, thanks.

I am ishwar singh and I create Awesome webistes ! visit http://www.ishwarsinghpanwa… if you are seriously looking for a website desinger for your business website !!

I say it’s screws up the IPO market after it massively underperforms.Someone pays the piper for Pros going into late private rounds hot on FOMO.It’s always retail.My guess is that drivers are like realtors. The top 2% drive ( no pun intended ) 50% of transactions & the top 20% are 80% of market activity.A bad bet if they are well past having the top 20% of drivers……

Novice question perhaps: Why does an IPO have to pop? The implication if it does is that the company left available capital on the table, no?

In order to keep growing so fast….I’m curious where rideshare is in gaining new riders: we’re past the early adopters it seems. What stage do you think it’s at.Then there’s the making a profit part….

Imagine you’re coaching Lyft CEO after the IPO. The lockup period is over, exits completed, cash for 18 months (again).He says – So, Jeff.. what shall we do now? Should we call Philip Sugar?

Good intuition. You’re right. There’s a conflict of interest between the bankers and their client (Lyft). The bankers want the IPO priced lower for two reasons. The first is that if a company is cheaper, more people are willing to buy it and it is easier to oversubscribe an offering (subscription to an IPO is it’s own topic and it is a reason retail investors should not participate in IPOs). The second is that the bankers “guarantee” an offering price by supporting the price through owning shares and potentially buying shares to increase demand. If the IPO is oversubscribed and the price is low enough, the demand will “pop” the price, which allows the bankers to profit on the shares they hold and everyone’s happy that the share price increased. Lyft may feel that the bankers screwed them by setting a low price so the client typically pushes for the highest price. Lyft should be a premiere IPO so the bankers will be competitive.

Much appreciated. Misinterpreted “meaningful pop” for closer to 50-100% as opposed to ~15%.All of this makes sense. Thank you.

Not a finance guy but if Lyft controls 28% of the market at a valuation of $18B then maybe Uber is roughly only worth $54B?

Uber valuation explains their timing. Not trusting Lyft to perform.