USV is an investor in Multicoin Capital, one of the leading token funds. In late October I attended their Multicoin Summit and spent about 45mins on stage with Tushar Jain, one of the two managing partners at Multicoin.

It’s a pretty good wide ranging conversation about how we think about investing in crypto right now (although it is a couple months old now).

When capital markets change direction, to the upside or to the downside, they often go too far before finding the right balance. When they overshoot to the downside, you can find some real values.

Back in the financial crisis of 2008, I was blogging about that as it related to the big tech stocks (Apple, Amazon, Google). The market hated everything and you could buy the big three tech franchises at crazy low prices as it related to their fundamentals (revenues, profits, cash flow, etc). And so I did and a lot of other people did too. And when the market came back in 2009 and beyond, those who bought at those bargain prices were rewarded.

So, it may be time to start thinking this way in crypto land. The reason I say “may” instead of “is” has to do with the fact that really bad bear markets take a while to find their footing and start moving up again. I worry that it will take crypto a while before it can make a move upward again. I wrote about that in this post a few weeks ago.

But nevertheless, I think it is time to at least start looking for fundamental value in crypto land. Ethereum is trading below $10bn. There are some traditional businesses in the crypto sector that are valued at almost that level. And if you believe in the fat protocols thesis, as I do, that gets my attention.

But there are more rigorous ways to think about fundamental value in crypto and one of the best known fundamental value thinkers in crypto is Chris Burniske, a partner in Placeholder, a crypto venture firm that USV is an investor in and I am an investor in too.

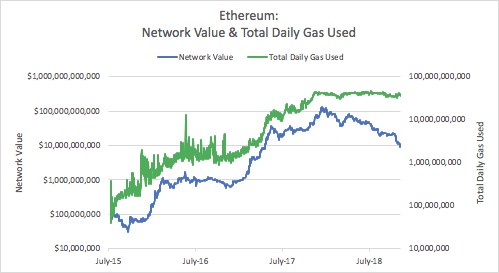

This chart from that post is the most telling in my view:

The green line is the use of gas to pay for smart contract execution on the Ethereum network. The blue line is the market cap of Ethereum. The growing gap between the green and blue lines represents, to me, the sign of market overshooting itself.

There remain some important fundamental questions about Ethereum so it is not like Apple, Google, and Amazon back in 2008. There is still existential risk in Ethereum. It could fail as a protocol and go to zero. So there are many reasons not to go all in on Ethereum right now.

But if you view Ethereum as a call option on the possibility that it will retain its role as the leading decentralized smart contract execution platform, then I think it is starting to look pretty compelling. And analysis like the work that Chris is doing is really helpful in determining things like that.

Decentralization is one of, if not the most, discussed features of the crypto tech stack. In a decentralized system, no single body controls the system. We have most certainly not reached the era fully decentralized systems, but that is what most of the world-class technologists working in the crypto sector are focused on getting us to and I believe we will get there in the not too distant future.

If you are a student of tech history, you will not be surprised that decentralization is also the right technology arriving at the right time to solve some of the most challenging policy problems facing the tech sector right now.

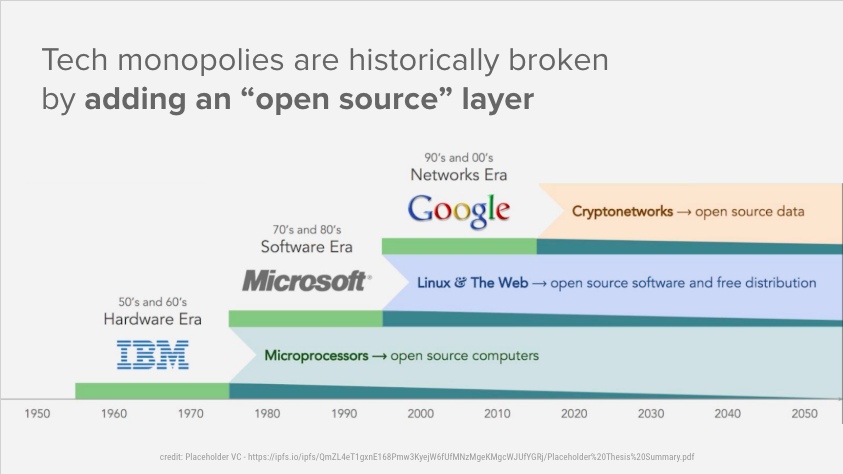

Before I elaborate on that, I want to show you a slide from my colleague Nick‘s deck on crypto that he uses to talk to policymakers and elected officials. I believe he borrowed it from our friends at Placeholder and they are credited at the bottom of this slide.

Here is my quick explanation of that slide.

IBM had a near monopoly on computing by virtue of their domination of the mainframe, mini-computer, and, it seemed, the PC computing platforms.

But the open PC hardware standard allowed Microsoft to develop an operating system that could run on any computer built to the PC hardware spec and they eventually unseated IBM, only to become a near monopoly themselves.

But just as we were wringing our hands about what to do about Microsoft’s monopoly, an open source operating system (Linux), the internet protocols, and the free distribution of the world wide web undid that monopoly and we got Google, Facebook, Amazon, and other big tech platforms.

And now we are wringing our hands about these near monopolies and their market power and the ability of bad actors to manipulate them. And around the same time, the technology to architect and scale a completely decentralized system emerges.

The other thing that is true of these moments of hand wringing is that just as the technology is emerging to unseat the near monopolies, regulators and elected officials try to put the genie back in the bottle using traditional regulatory techniques that often end up more deeply entrenching these near monopolies.

To give you an example of how this might happen, I am going to suggest you all go read my partner Albert’s post from yesterday on Twitter and how one might approach addressing some of the vexing problems that platform is dealing with right now.

That is how elected officials and regulators often think. They look backwards to find a model of regulation that has worked in the past and try to apply it to a new thing. But as Albert explains:

The idea that there could or should be a single central institution, let alone a commercial company, which as a benevolent dictator resolves all of these issues to everyone’s satisfaction is a complete non-starter.

Instead he proposes a few ideas that are steeped in decentralization:

my preferred go to answer is to shift more power to the network participants by requiring Twitter (and other scaled services) to have an API. That would allow endusers to programmatically create the best version of Twitter and would also make it easier to simultaneously use Twitter and new decentralized alternatives.

And

Twitter should significantly expand the features that let individuals and groups manage the visibility for tweets for themselves. There are already useful features such as muting a conversation or blocking an individual. These could be expanded in ways that allow for delegation. For instance, users should be able to say that they want to subscribe to mute and block lists from other individuals, groups or organizations they trust. One example of this might be that I could choose to automatically block anyone who is blocked by more than x% of the people I follow (where I can choose x). Ideally these features could be implemented at the tweet/conversation level and not just the account level.

So you can see that by decentralizing the power to the edges of the network INSTEAD of further concentrating it by requiring the network owner to further centralize power is the right answer, both from a technology perspective and a regulatory/policy perspective.

Sadly, I think we are in a race with ourselves in this centralization vs decentralization debate. We need the decentralized tech stack to evolve more quickly and show the world how decentralized technology works in a mainstream way at scale before policy makers and regulators force the tech sector to go the wrong way.

And, most disturbingly, the regulators and elected officials are taking actions, well intended of course, to slow the decentralized sector down, not speed it up.

Which is why we at USV have been spending a lot of time with public servants of all kinds, educating them, imploring them, and desperately trying to get them to understand where we are, why it is an important moment, and why we need to this new technology to succeed.

One of the big issues facing the crypto sector is the regulatory question, both in the US, where it looms largest, and elsewhere around the world. In the last few weeks we have seen the SEC reach settlements with several crypto projects and decentralized exchanges, all of which were the subject of enforcement actions or threatened enforcement actions. As I alluded to in this post last week, I fully expect to see the SEC continue to look hard at the crypto sector in an effort to rein in what it sees as violations of its rules on the offering and sale and trading of securities.

In the wake of all that, The New York Times hosted an event last week in which Andrew Ross Sorkin interviewed SEC Chairman Jay Clayton.

This is a recording of that interview. The conversation is about an hour long. You can/should fast forward to 11 1/2 minutes in to bypass all the introductions.

It’s hard to look at the price charts of the big crypto assets and not cringe.

But it helps to look back to an earlier time, when a new sector was emerging, and understand what can happen.

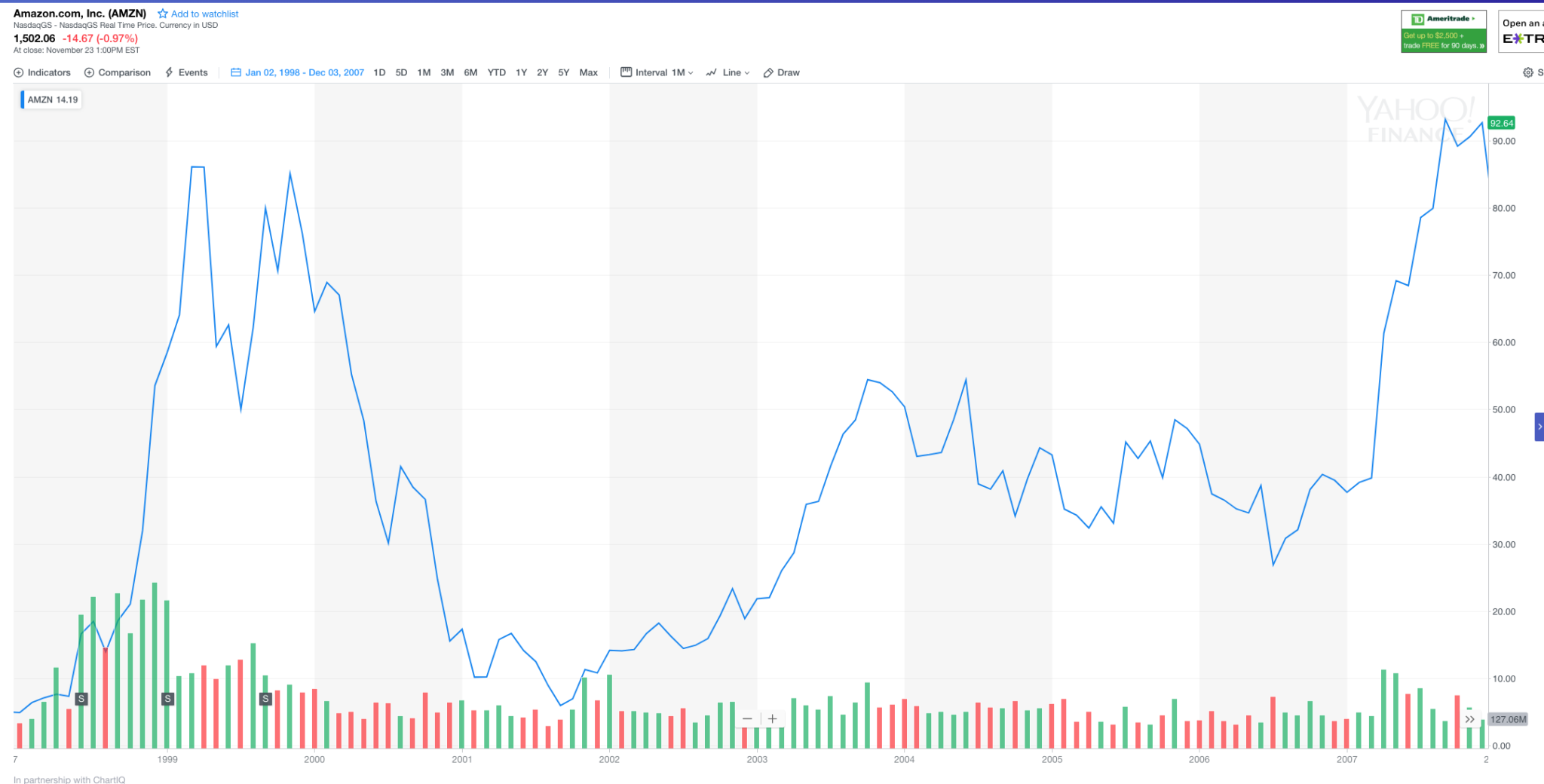

Amazon peaked in the Internet bubble in late 1999 at around $90/share.

Almost two years later, at the trough, you could briefly buy Amazon at $6/share.

And then it took until late 2007 for Amazon to trade above the highs it reached in 1999.

But of course, all of this is ancient history and if you look at Amazon’s chart today, all of that turbulence is hardly even visible.

But for those of us who were investing in tech and tech startups back in 1999-2002, that time will forever be etched in our minds. It was a brutal period during which our belief in the Internet and its potential was sorely tested. Many friends and colleagues left the sector and never returned.

So while crypto asset prices are down 80-95% in USD terms over the last year, they could and probably will go lower. Amazon was down 80% a year into the post-bubble bear market and it got cut in half again before it made a bottom almost two years after it peaked.

What we have yet to see in crypto land is when they kick you when you are down. And that is certainly coming. Regulators came after the Internet sector in a big way post the bubble and that seems likely to happen in the crypto sector too.

And most everyone in big companies wrote the Internet sector off, cancelling their Internet efforts as a fool’s errand. That seems likely to happen in crypto too.

And many talented people left the sector. That seems likely to happen in crypto as well.

But those who stayed were rewarded, although it took a long time for that to happen. We didn’t see meaningful paydays in the Internet sector until the 2007-2008 period and the big paydays didn’t start coming until 2010 and beyond.

The thing to look for in the downturn is signs of life. There were little projects that turned into big ones. Blogger was started in late 1999, almost shut down many times in the next few years, and was picked up by Google in 2003. Myspace, LinkedIn, and Facebook all emerged in the 2002-2004 period, as the Internet was finally coming to life again.

So that is my framework for thinking about where we are with crypto and where we are going.

I think some crypto asset (and possibly a number of crypto assets) will have a price chart like Amazon’s current one in 18 years. But we will have to do what Amazon did, hunker down and build value and survive, for quite a while to get there. And I think things will get worse before they get better.

I just watched Vitalik Buterin’s keynote at Devcon 4 in Prague last week, on Halloween and on the tenth anniversary of Satoshi’s whitepaper.

In this keynote, Vitalik explains what has taken so long in getting from Ethereum 1.0 to Ethereum 2.0, what Ethereum 2.0 will include, and how we are going to get there.

It is a bit geeky, I can’t say that I understood everything, but if you own Ethereum, or if you believe that a scaled decentralized smart contract platform is important, and I can say yes to both of those emphatically, then this is worth watching. It is 30 mins long.

Ever since the first cryptonetwork, Bitcoin, was created, investors have had the opportunity to earn returns by engaging in the network. In Bitcoin’s case, that was done by mining the network, effectively powering it.

As the sector has grown, investors have largely turned their attention to buying and holding cryptoassets, and not that many of us are actively engaging in them.

But that is likely going to change for several reasons.

First, in proof of stake networks, asset holders will want to stake their tokens and earn the rewards of doing that, or risk being diluted/inflated. Conversely, those who do stake will earn rewards that will feel a bit like collecting interest or dividends on a bond or stock.

This technique of turning an idle asset into an incoming producing asset by engaging in the network is part of the design of many cryptonetworks and investors are going to increasingly want to do these things (staking, validating, governing, etc) to earn the rewards of that engagement.

There is another aspect to this, outlined by Tushar Jain of Multicoin earlier this week on their blog.

Tushar points out that asset holders can act with their capital to help bootstrap the network by providing storage on the Filecoin network or transcoding on the LivePeer network or creating DAIs on the Maker network.

The good news for investors is that there are a whole bunch of entrepreneurs setting up shop right now to help us do these things without each and every one of us becoming super technical about the ins and outs of each of these cryptonetworks. We will see (and are seeing) staking as a service, nodes as a service, and the like. These third parties will be like the proxy companies are in the stock markets.

I expect the custodians, like our portfolio company Coinbase, to offer many of these services, either as the provider themselves or the gateway to the third party provider, thereby making it even easier for us to engage in these networks.

It’s an exciting time to be a cryptoinvestor. A host of new cryptonetworks are starting to go live. The next 18 months will see many dreams come to fruition and with those dreams will come demands on the investors to engage instead of just hold. I am looking forward to doing that.

Fortune recently did a big profile on Brian Armstrong, founder and CEO of our portfolio company Coinbase and in concert with that, they made this video featuring Brian and Emilie Choi, who leads corp dev, M&A, and a few other strategic efforts at Coinbase.

It’s a short video, less than five mins, and does a nice job of explaining the company’s mission and strategy.

When someone asks you how much of a company you own, the answer could be two very different numbers. You might own 10,000 shares and there might be 1mm shares issued and outstanding. That would suggest you own 1% of the company. And that would be correct, as of right now.

What is often not calculated in these sorts of numbers is future dilution, particularly dilution that is visible if you look closely. The most common form of future dilution that is visible are outstanding options and warrants to issue stock that have not been exercised.

Let’s say this fictional company that has 1mm shares outstanding also has a 20% unissued option pool (so 200,000 options in it), and lenders have warrants to purchase 50,000 shares.

That would be another 250,000 shares that are not issued, but will be at some point, making the “fully diluted shares outstanding” equal to 1.25mm, and your 10,000 shares now represent 0.8% of the company. That is your “fully diluted ownership.”

Nowhere is this issue more important than the crypto token sector. There are many crypto tokens trading in the market that have a relatively small amount of their total supply outstanding and the market value numbers on many of the sites that track this market are a bit misleading.

For this reason, I like the concept of “year 2050 market cap” that the site OnChainFx reports.

Take Numeraire, a token issued by our portfolio company Numerai, and a token that USV owns some of (that is a disclosure if anyone is confused).

But by 2050, there will be a lot more Numeraire out there and as OnChainFX reports, the 2050 Market Cap is more like $110mm. It would take more like $1mm to purchase 1% of Numeraire’s total supply.

This concept of a market cap that includes future dilution is called a “Fully Diluted Market Value” and it is something investors need to be focused on when thinking about value, upside, and dilution.

My view has been, and is, that we are in the “infrastructure phase” of the crypto market development cycle.

To elaborate, I believe that we need better infrastructure (e.g. better base chains, better interchain interoperability, better clients, wallets and browsers) before we can see a robust application development environment and so I have stated many times that right now is a time to focus on building (and investing in) that infrastructure. That view has been the prevailing wisdom inside of USV for quite a while now.

Well a couple of our colleagues at USV decided to poke holes in that argument and spent a few weeks doing research and then writing this post.

I have a feeling that this post may be headed to similar territory as Joel‘s now famous Fat Protocols post because, like that one, it takes a conventional wisdom and turns it on its head.

Dani and Nick argue that there are no distinct phases but in fact, a virtuous cycle of apps>infrastructure>apps>infrastructure that brings a new market/technology into its own.

Read the post, as this argument is well researched and well made.

However, as much as I agree with their arguments, I continue to believe that for investors, the best bets right now are infrastructure bets. It remains too hard, too expensive, and too frustrating, to build decentralized apps and the big value unlock will come when that changes. I think the returns on investment on infrastructure will be higher in the phase we are in right now. There will come a time when apps development will have a better ROI, but I do not think we are there right now.

USV has made investments in decentralized apps, like OB1 and CryptoKitties, and we will continue to do that. But our primary focus is on infrastructure right now.