Startups are generally not funded by just one investor. They are usually funded by a collection of investors; the angel syndicate, followed by the seed syndicate, followed by the VC syndicate.

This gives the founder the opportunity to gain insights and advice from a group of people versus just one.

I was sitting next to a VC last night who brought up the age old question – operator vs investor? She is a successful early stage investor who has never been an operator.

My answer to her question was “both.”

Yes it is fantastic to have people in the syndicate who have been or maybe still are operators. They will be able to help you with all sorts of management issues.

But it is equally important to have the investor mindset in your syndicate. Investors tend to be very attuned to financial issues like burn rate, when to raise, from whom, etc. They also understand market positioning, strategy, and similar stuff very well.

While you are at it building a diverse investor syndicate, try to get women, minorities, and other forms of diversity into your syndicate.

Treat building an investor syndicate like building a management team. What you want is a lot of differing strengths not a bunch of the same strengths.

I get asked frequently whether it is better to back the team or the product (the “jockey or the horse”).

It is not that simple in my view.

When I think about the big wins we have had over the years, they almost all exhibited a combination of a large market, a great product, and a talented founding team.

Some investors feel that the team doesn’t matter. They believe that you can replace the team if everything else works out. But I don’t think everything else works out if you don’t have a talented founding team.

Some investors feel that product doesn’t matter. They believe that you can pivot into something else if you have a talented founding team. While that is certainly the case, pivots are expensive in terms of capital, time, and focus. I would not choose to go through one given the choice.

And large market is critical. You can build a nice business in a small market, but you can’t build a big business in a small market.

My point is you really need all three, market, product, and team, to get the big wins that the venture capital model requires.

And in terms of finding the best opportunities, I would start with large markets, go searching for teams working in them, and writing checks only when you find talented teams working in large markets who have built excellent products.

Many people in startup land believe that the answer to the challenges around forcing departing employees to exercise vested options is to simply extend the option exercise period to the maximum (ten years) allowed by the IRS.

It certainly is one of the techniques that are available to companies and one that a number of our portfolio companies have adopted. Another option, and one that I prefer, is for a market to develop around financing these option exercises (and the taxes owed) when employees depart.

However, if you are thinking about extending the option exercise period for departing employees, you should understand that it will cost your company something.

Here is why:

Options are worth more than the spread between the strike price (the exercise price) and what the stock is actually worth. They have additional value related to the potential for the stock price to appreciate more over the life of the term of the option.

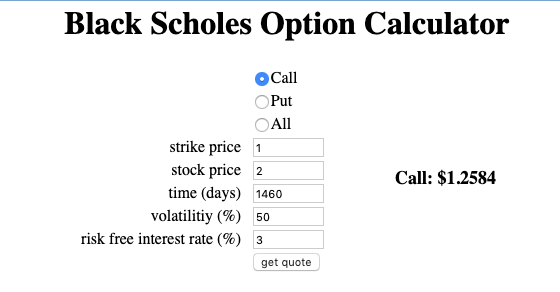

There is a formula that options traders (and companies that issue options) use to value options. It is called the Black-Scholes formula.

If you click on that link, you will quickly realize that the math used in the Black-Scholes formula can be complicated. But fortunately, there is a neat little web app that I frequently use to estimate the value of an option. It is here.

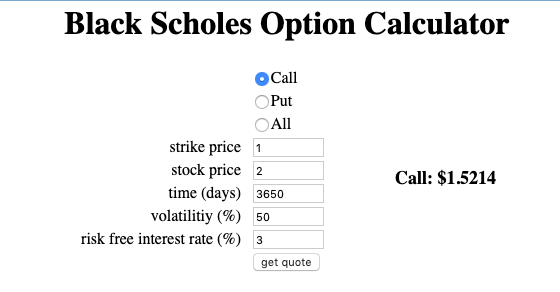

So let’s say that your company is issuing options at $1/share (your 409a) but your most recent financing was done at $2/share. Then a four year stock option is worth roughly $1.25/share.

If, on the other hand, you offer a ten year option exercise period to your employees, the value of the option rises to $1.52/share, reflecting the longer period of time that the stock could appreciate over.

That is a 20% increase in the cost of issuing stock options. You could mitigate that by reducing the number of options you issue to incoming employees by 20% but that might make your equity comp offers less attractive to the “market” because incoming employees won’t value the longer exercise periods appropriately.

Stock based compensation costs are real costs even though many in startup land think of options as “free” because they don’t cost cash. The accounting profession has attempted to estimate these costs and companies do put stock based compensation costs on their income statements. If you go with ten year exercise periods instead of four year exercise periods, expect those expenses to go up significantly. Twenty percent is just the amount in my example. It could be larger, possibly as high as fifty percent (or more) if your exercise price is a lot closer to the current value of your stock.

This extra value of a ten year stock option versus a four year option is known as “overhang” by investors. It is the cost of carrying a group of people who have a call option on your stock but don’t have to pay for it for a long period of time. Generally speaking investors don’t like a lot of overhang in a stock.

All of that said, employees are the ones who create value for shareholders. They need to be compensated for that. And I am a fan of both cash compensation and stock based compensation. I like to see the employees of our portfolio companies well compensated in stock. That has a cost and everyone should be well aware of what it is. Longer exercise periods increase that cost. I would rather put more stock in the hands of the employees of our portfolio companies than give them longer exercise periods. But regardless of where one comes out on that tradeoff, it is important to recognize that it is a tradeoff. There are no free lunches, not even in stock option exercise periods.

Let me first say that I am sympathetic to Warren’s position. I particularly don’t like the way that Google, Apple, and Amazon use their market power in search and in their app stores to display their own products. The mobile app stores, in particular, have always seemed to me to be a constraint on innovation vs a contributor to it.

However, as you might imagine, I don’t love her proposal. I don’t think breaking up companies solves anything. And lots of rules on paper don’t either.

What we need is a competitive marketplace where new entrants have a chance to beat out old incumbents.

And I think we are on the cusp of that with crypto and the innovations in and around it.

This tweet exchange explains my high level view here:

we are on the cusp of a new architecture, based on a user's control of their own data, and monetized via protocol tokens, that will unseat all of these monopolies in time. the massive increase in ICO-based fundraising, largely outside of the US, is the counterweight to this.

What we need are policies that make it easier for startups to raise capital (like supporting ICOs instead of clamping down on them) and policies that open up the proprietary data assets of the big incumbents (like giving users control of their own data assets). Those sorts of things along with the never ending march of technology will do the trick I think.

I wrote a bit last Monday about the 60 Minutes piece last Sunday night about getting to gender equity in STEM education. My message in that blog post was that there are many innovators in this sector and not everyone will get the credit they are due.

Ayah Bdeir, who was left on the cutting room floor on that 60 Minutes piece, had a different message and one that I understand and appreciate.

Ayah is awesome and I want to shine a light on her and her work and there is no better way to do that than to repost her conversation with The Gotham Gal from last year.

I have always seen a lot of Gates in Zuck. They both have this incredible ability to see someone else’s product and realize that they need to build their own version of it.

But copying someone else’s product is a lot easier than copying someone else’s business model, particularly when you already have a fucking great one that makes you and your shareholders billions of dollars a year.

It will be interesting to watch Zuck do what Gates was ultimately unable to do – completely reboot the company’s business model to position itself to win the next wave in tech.

In the case of Gates, it was the pivot from paid software to free advertising supported software (aka – the attention economy that we are now paying for).

In the case of Zuck, it will be the pivot from monetizing attention to monetizing the protocol. The good thing is he is headed in the right direction, and surrounded some of the smartest people I know in crypto. The bad news is when you have this anchor called a legacy business model, it means making the right moves and making them quickly a lot harder.

Here is an example of one of those choices Facebook will need to make and make correctly:

If @facebook’s stablecoin goes the private blockchain route it will be to #crypto what @Microsoft’s Internet Explorer was to the Internet.

In any case, it is game on. Being on the verge of 60 years old means I have seen this game play out at least once before and so I have a frame of reference to observe it. That’s really great. It is an exciting time again in tech.

@fredwilson Have you ever written about how to avoid "rest and vest" culture where there are employees who want to leave a company but are held down by golden handcuffs?

I don’t believe I have ever addressed this issue here on AVC but I certainly have seen it inside of our highly valued portfolio companies.

Here is the issue. Employees join a high growth company, are issued options which become valuable as the company’s equity appreciates, and if they leave they have to exercise the vested part (and pay taxes) and walk away from the unvested part. So they stay even though they may not be happy at work. Maybe they are not in a challenging role or maybe they find themselves in a problematic management situation. This leads to “resting and vesting.”

Here are some thoughts:

1/ A four year option grant is not a gift. It has to be earned via performance over time, not just time. If there is no performance, then the employee should understand the vesting is at risk. Companies should be very clear about this when they issue the options and on an ongoing basis. This is a cultural issue and needs to be treated as such.

2/ Companies need to have performance oriented cultures where there are frequent checkins between managers and team members, with feedback going both ways, and where non-performance results in changes. These changes could be restructuring of teams, changes in management, or departures of employees. Companies that do not actively manage performance are likely to have lower morale and toxic issues like resting and vesting.

3/ Managers and company leadership must do their part to take ownership of these issues. Employees will adapt to the environment they find themselves in. If you have a rest and vest culture in your company, look in the mirror to see the problem.

4/ I would like to see a market emerge for financing of option exercises. There are companies actively working on this. I believe that departing employees ought to be able to borrow against their valuable equity at no recourse to them, so that they can exercise and pay the taxes. This would solve part of the problem, where employees can’t leave because they can’t afford the taxes (and, in some cases, the exercise price).

5/ I do not believe that the option programs are the problem here. I do think the taxation at exercise is bad public policy and I wish the US government would move taxation to a liquidity event, but I also think we can use the capital markets to address this problem.

6/ I think in the vast majority of cases, the golden handcuff problem is a result of poor management and a leadership team that is unwilling to address this issue head on and make unpopular and difficult decisions about people.

So there you have it Daniel. That’s what I think about this issue. Thank you for asking me about it.

Howard has a great (and short!) post on how blogging publicly gives you a timeline on how you were thinking at a given time. He’s right, it is awesome to be able to go back and see what you were thinking and evaluate it in hindsight.

Sitting here two months and a few days into 2019, I could not have been more wrong about the first couple predications I made in that post.

The stock market has been on fire and the President is still firmly in charge.

Of course all of that could change.

It is still early days in 2019.

But going back and re-reading that post is super helpful in reminding me that my assumptions may be wrong and I need to re-evaluate the assumptions to make sure I am heading in the right direction.

And blogging (aka taking a stand publicly) is a great way to do that.

And while I completely agree with Rob that Reshma has built something amazing at Girls Who Code, I also feel that the results she and her organization are getting are what matters the most and so I responded with this:

What I have learned from watching my wife (@thegothamgal) work on gender equity in startups and my own work on equity in CS education is that you cannot worry about who gets the credit, you have to worry about the results. It makes it easier to stay focused and stay happy

Later today, a friend and fantastic entrepreneur sent me a private email arguing that credit is very important and that it is how organizations gain credibility, legitimacy, and support to keep going.

Of course she is right. Credit is important.

I also got an email from the folks I work with at the NYC public school system pointing out that the NYC public school profiled in the 60 Minutes piece was the beneficiary of the CS4All effort which I have been championing for almost a decade now and that was left entirely out of the story.

All of this is unfortunate. There is a very broad coalition of organizations doing incredible work making sure that we have gender and racial equity in STEM education. And we are starting to see the results of all of the work of these groups. It would have been nice to credit a much broader group of organizations and companies.

But this happens all the time. USV has been the seed and largest investor and a highly engaged board member in companies that are referred to in the press as an “Andreessen Horowitz backed company” or a “Sequoia backed company” or a some other such characterization. When I see that I flinch a bit but tell myself that it is the company, the founders, and the results that matters and not who invested in it.

Success has a thousand mothers and some will get more credit than others. That is the unfortunate truth of success. But if we focus on the success versus the credit then I think we will all be better off.