Trust is rising as a central issue in tech and the Internet. We spend a lot of time at USV thinking about trust and talking about trust. It is part of our current investment thesis.

Rachel Botsman is a writer who focuses on trust and her talk at DLD last month was quite good.

Ever since I got interested in crypto, I have looked at the emergence of the commercial Internet in the 90s as a roadmap for what to expect.

And while that has largely been useful as a frame of reference, I’ve struggled with the huge bubble of 2017 which felt to me like it came too early relative to the maturity of the sector.

Yesterday I read this post which has a great explanation for that:

The bubble came early because blockchain technology enabled liquidity earlier in its life cycle.

That makes a ton of sense to me and reframes the timelines in my mind.

Phew.

Some of you may have noticed that I waited until very late in the day today to post. I’m struggling a bit with adjusting to time zones, a head cold, and today was just one of those days where nothing went as planned.

I’m not planning on making early evening eastern time my regular routine.

Two weeks ago, my colleague Nick traveled to Hong Kong to attend a Blockstack event (Blockstack is a USV portfolio company) and deliver this talk, which covers some important questions/issues in the crypto sector.

This short tweetstorm sets up the video well, so I will start with that and follow with the video which is 17mins long.

In a nutshell: On the one hand, we have the "agile" approach to building apps: start small and iterate quickly. On the other hand, we have "immutable" decentralized systems, which are — by design — stable and hard to change.

This presents a challenge when trying to find product-market-fit. Being agile means prioritizing user experience, but retaining control. Being decentralized means prioritizing security and handing over control

Both at the application layer (e.g., cryptokitties, numerai, augur) and at the blockchain layer (bitcoin, ethereum, eos, etc), this tension is playing out, and it will be interesting to see what will ultimately become a new paradigm for developing platforms and apps take shape

A friend sent me this Kickstarter project earlier this week. I took a look and thought “wow, that’s so great. a digital piggybank for kids with its own cryptocurrency, a mobile app, and educational games teaching them to earn and save.” I backed it this morning and though I don’t normally take the rewards on Kickstarter, I did this time. I can’t wait to give this to a kid when I get it this summer.

For most companies and projects in the crypto sector, a big issue has been how to design their token and how to get it in the hands of users, validators/miners, and investors. As Joel explained in this post, you need all three stakeholders to create a well functioning crypto-token.

There is the Bitcoin approach, which is to allow anyone to mine the protocol and earn tokens.

There is the Ethereum approach, which is to do a pre-sale.

And there are many other approaches. The last time I looked there were over 2,000 crypto-tokens that are trading on various exchanges around the world and many more that are not yet trading.

There are plenty of considerations when you design a crypto-token but certainly one of them is figuring out how to avoid having it deemed to be a security in the US. Securities are highly regulated in the US, can only be traded on regulated exchanges, come with significant disclosure requirements (many of which make no sense for an open source project), and there are limits to whom you can sell them to and how.

Most token projects and companies look at Bitcoin and Ethereum and say “we want to be like them.”

So when William Hinman, director of the SEC’s Division of Corporation Finance gave a speech at the Yahoo Finance All Markets Summit on June 14, 2018 suggesting that Bitcoin and Ethereum were not securities and laid out an argument that they were sufficiently decentralized, it got a lot of people’s attention in the crypto sector.

The basic reasoning behind the decentralization framework is that if a project is truly decentralized and there is no central actor or actors, then there really is no “issuer” and there is no possibility that the central actor(s) can act on insider information or otherwise have information asymmetry.

The crypto industry has been pressing the SEC to codify this logic in a set of rules that projects and companies can follow. But the SEC has to date been unwilling to do so.

So the Blockchain Association has stepped in and taken a stab at codifying the Hinman Test. In a post they published today, they have laid out the basic arguments of Hinman’s Framework and then outlined how one could determine if a token project was sufficiently decentralized.

This is not as helpful as an SEC published set of guidelines, but until we get that (soon I hope), this will have to suffice.

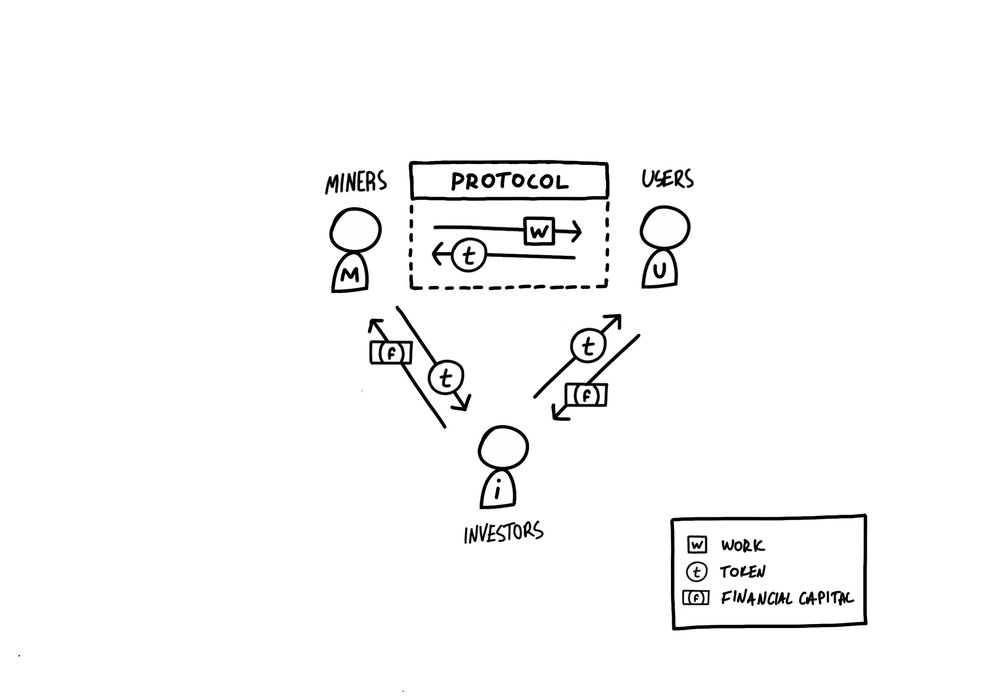

Joel Monegro, who is one of the Partners at Placeholder and a former USV analyst, has written an important post that outlines the relationships between the three primary stakeholders in a cryptonetwork; users, miners/validators, and investors.

Joel calls it the Cryptoeconomic Circle, although it sure looks like a triangle to me 🙂

The most important “aha” that this post generated for me was the role of capital/investors in a cryptonetwork.

Maybe because I come from the world of venture capital, where the role of capital is to fund the cost of developing the technology and business, I had always seen the role of capital in a cryptonetwork similarly.

But as Joel points out in his post, that is one of two roles of capital in a cryptonetwork. The other role is to support and sustain the network by supplying financial capital to the validators who do the work in the system.

As Joel explains in his post:

There are short-term investors (traders), and long term investors (holders). Traders create liquidity for the token so miners can cover operational costs, while holders capitalize the network for growth by supporting token prices. The former is a direct form of value transfer where miners sell earned tokens in the open market to cover their costs and reinvest profits, and the latter is an indirect transfer of value that shows up in miners’ balance sheets rather than their income statements.

Like Joel’s post on Fat Protocols two and a half years ago, I think this will be an important post in helping people understand how these networks actually operate and exchange/capture value. As Joel says at the end of the post:

it helped me see cryptonetworks as systems for exchanging labor for capital (vs. currency), the fundamental concepts of network capital, and what the different roles are for investors like us in the development of these new economies

Today, as is my custom on the first day of the new year, I am going to take a stab at what the year ahead will bring. I find it useful to think about what we are in for. It helps me invest and advise the companies we are invested in. Like our investing, I will get some of these right, and some wrong. But having a point of view, a foundation, is very helpful when operating in a world that is full of uncertainty.

I believe and have been telling those around me that I think 2019 will be a “doozy.” I think we will see major dislocations in the leadership of the United States, a bear market in stocks, a weakening economy, a number of issues with the global economy including a messy Brexit and a sluggish China. All of this will lead to a more cautious stance by investors in the startup economy. And crypto will not be a safe haven for any of this although there will be signs of life in crypto land in 2019.

Let’s take each of those in the order that I mentioned them.

I believe that we will have a different President of the United States by the end of 2019. The catalyst for this change will be a devastating report issued by Robert Mueller that outlines a history of illegal activities by our President going back decades, including in his campaign for President.

The House will react to Mueller’s report by voting to impeach the President. Which will set up a trial in the Senate. That trial will go so badly for the President that he will, like Nixon before him, negotiate a resignation that will lead to him and those close to him being pardoned for all actions, and Mike Pence will become the President of the United States sometime in 2019.

I believe this drama will play out through most of 2019. I expect the Mueller report to be issued sometime in the late winter/early spring and I expect an impeachment vote by the House before the summer, leading to a trial in the Senate in the second half of the year.

The drama in Washington will have serious impacts to the economy in the United States starting with our capital markets.

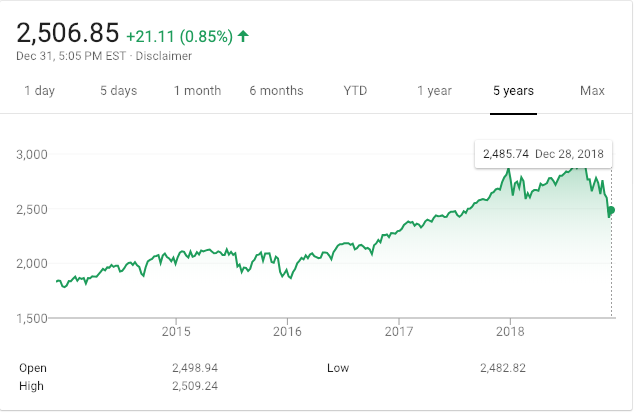

The US equity capital markets enter 2019 on shaky ground. Though the last week of the year brought us a relief rally, the markets are dealing with higher rates, some early indications of a weaker economy in 2019 (possibly due to higher rates), and, of course, the potential for the drama in Washington that we’ve already discussed. Here is a chart of the S&P 500 over the last five years:

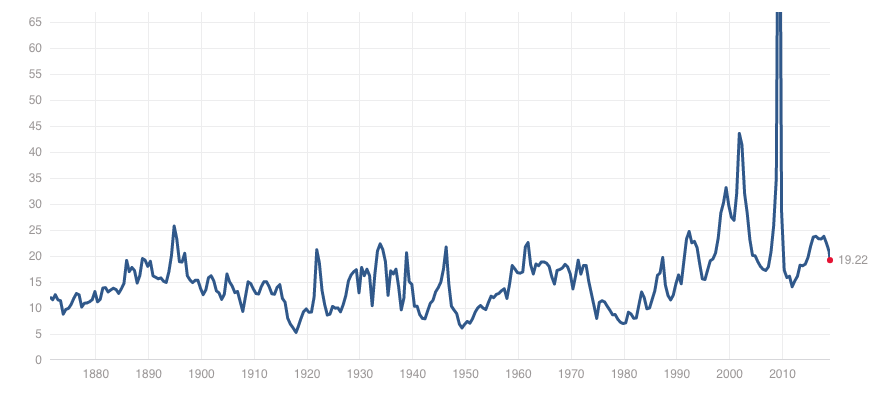

I expect the S&P 500 to visit 2,000 sometime in 2019 and then bounce around that bottom for much of the year. This would represent a decrease in the S&P’s trailing PE multiple to around 15x which feels like a bottom to me given the recent history of the equity markets in the US:

S&P PE Multiple (source http://www.multpl.com/)

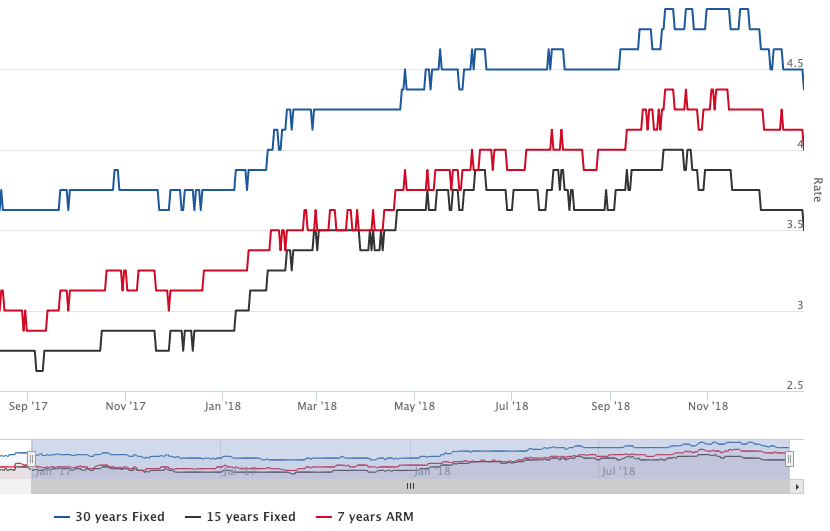

Interest rates have been rising gradually in the US for the last three years. The Fed has taken its Fed Funds rate from essentially zero three years ago to almost 2.5% today:

The rates that are available to consumers and businesses have followed and I expect that to continue in 2019. Here is a chart of the interest rates on the three most popular mortgage products in the US:

Source: https://www.amerisave.com/graphs/

When it gets more expensive to borrow, marginal projects don’t get funded. And what happens at the margin has a much larger impact on the economy than most people understand. No wonder the President wants to fire the Fed Chairman.

I expect the combination of higher rates, uncertainty in Washington, and storm clouds globally (which we will get to soon) will cause business leaders in the US to become more cautious on hiring and investment. Consumers will make essentially the same calculations. And that will lead to a weaker economy in the US in 2019.

The global picture is not much better. The eurozone is about to go through the most significant change in decades with some sort of departure of the UK from the EU (Brexit). It remains unclear exactly how this will happen, which in and of itself is creating a lot of uncertainty on the Continent. I don’t expect most businesses in Europe to do anything but play defense in 2019.

Probably the biggest unknown for the global economy is the resolution of the ongoing trade tensions between China and the US. It seems inevitable that China will make some concessions to the US to resolve these trade tensions. But, of course, what happens in Washington (first issue) may impact all of that. In the meantime, the uncertainty around trade and exports hangs over the Chinese economy. China’s GDP has been slowing in recent years as it achieved relative parity with the US and the Eurozone:

Source: https://tradingeconomics.com/china/gdp

Any significant trade concessions from China could impact its growth prospects in 2019 and beyond, which will take the most powerful engine of global growth off the table this year.

So all of that is a pessimistic take on the broader macro environment in 2019. How will all of this impact the startup/tech economy?

The startup/tech economy is somewhat immune to macro trends. Many startups and big tech companies were able to grow and expand their businesses during the last financial downturn in 2008 and 2009. Some very important tech companies were even started in those years.

The tech/startup economy is driven first and foremost by technical and creative (ie business model) innovation. And that is not impacted by the macro environment.

So I expect that we will continue to see big tech invest and grow their businesses and do well in 2019. I expect we will see IPOs from big names like Uber/Lyft/Slack, although I also expect those deals will get priced well below the lofty expectations they have in mind right now. Some of that will be because of weak equity markets in the US, but it is also true that most of the IPOs in 2018 also priced below the lofty “going in” expectations of founders, managers, boards, and their bankers. The public markets have been much more sanguine about value than the late stage private markets for a long time now.

However, I do think a difficult macro business and political environment in the US will lead investors to take a more cautious stance in 2019. It would not surprise me to see total venture capital investments in 2019 decline from 2018. And I think we will see financings take longer, diligence on new investments actually occur, and valuations to come under pressure for even the most attractive opportunities.

But all of that is going to happen at the margin. I expect 2019 to be another solid year for the tech/startup sector as we are in a possibly century-long conversion from an industrial economy to an information economy and the tailwinds for tech/startup vs the rest of the economy remain in place and strong.

Any set of predictions for 2019 from me on this blog would not be complete without some thoughts on crypto. So here is where my head is at on that topic.

I think we are in the process of finding the bottom on the large, liquid, and lasting crypto-tokens. But I think that process could take much of 2019 to play out. I expect we will see some bullish runs, followed by selling pressures taking us back to retest the lows. I think this bottoming out process will end sometime in 2019 and we will slowly enter a new bullish phase in crypto.

I think the catalyst for the next bullish phase will come as the result of some of the many promises made in 2017 coming to fruition in 2019. Specifically, I think we will see some big name projects ship, like the Filecoin project from our portfolio company Protocol Labs, and the Algorand project from our portfolio company Algorand. I think we will see a number of “next gen” smart contract platforms ship and challenge Ethereum for leadership in this super important area of the crypto sector. I also expect the Ethereum open source community to ship a number of important improvements to its system in 2019 and defend their leadership in the smart contract space.

Other areas of crypto where I expect to see meaningful progress and consumer adoption happen in 2019 are stablecoins, NFT/cryptoassets/cryptogaming, and earn/spending opportunities, particularly in the developing world.

There will also be pressure on the crypto sector in 2019. The area I am most concerned about are actions brought by misguided regulators who will take aim at high quality projects and harm them. And we will continue to see all sorts of failures, from scams, hacks, failed projects, and losing investments be a drag on the sector. But that is always the case with a new emerging technology that allows anyone to set up shop and get going. Permissionless innovation produces the greatest gains over time but also comes with the inevitable bad actors and actions.

So that’s where my head is at on 2019. Do I sound pessimistic? I suspect I do, but I am not. I am incredibly optimistic, like my partner Albert and can’t wait to get going and make things happen in this new year. It is going to be a doozy.

Brian Armstrong, founder and CEO of USV portfolio company Coinbase, sat down with Coinbase Board Member Chris Dixon and talked about how Brian started Coinbase, how the company grew, and where crypto is today.

It’s about 40mins and it’s a great conversation to listen into.

USV is an investor in Multicoin Capital, one of the leading token funds. In late October I attended their Multicoin Summit and spent about 45mins on stage with Tushar Jain, one of the two managing partners at Multicoin.

It’s a pretty good wide ranging conversation about how we think about investing in crypto right now (although it is a couple months old now).

When capital markets change direction, to the upside or to the downside, they often go too far before finding the right balance. When they overshoot to the downside, you can find some real values.

Back in the financial crisis of 2008, I was blogging about that as it related to the big tech stocks (Apple, Amazon, Google). The market hated everything and you could buy the big three tech franchises at crazy low prices as it related to their fundamentals (revenues, profits, cash flow, etc). And so I did and a lot of other people did too. And when the market came back in 2009 and beyond, those who bought at those bargain prices were rewarded.

So, it may be time to start thinking this way in crypto land. The reason I say “may” instead of “is” has to do with the fact that really bad bear markets take a while to find their footing and start moving up again. I worry that it will take crypto a while before it can make a move upward again. I wrote about that in this post a few weeks ago.

But nevertheless, I think it is time to at least start looking for fundamental value in crypto land. Ethereum is trading below $10bn. There are some traditional businesses in the crypto sector that are valued at almost that level. And if you believe in the fat protocols thesis, as I do, that gets my attention.

But there are more rigorous ways to think about fundamental value in crypto and one of the best known fundamental value thinkers in crypto is Chris Burniske, a partner in Placeholder, a crypto venture firm that USV is an investor in and I am an investor in too.

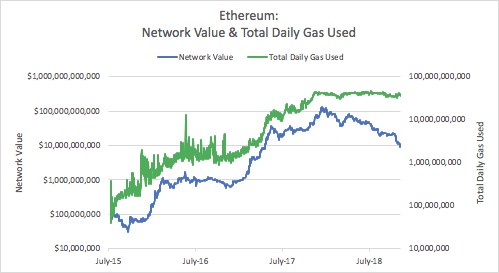

This chart from that post is the most telling in my view:

The green line is the use of gas to pay for smart contract execution on the Ethereum network. The blue line is the market cap of Ethereum. The growing gap between the green and blue lines represents, to me, the sign of market overshooting itself.

There remain some important fundamental questions about Ethereum so it is not like Apple, Google, and Amazon back in 2008. There is still existential risk in Ethereum. It could fail as a protocol and go to zero. So there are many reasons not to go all in on Ethereum right now.

But if you view Ethereum as a call option on the possibility that it will retain its role as the leading decentralized smart contract execution platform, then I think it is starting to look pretty compelling. And analysis like the work that Chris is doing is really helpful in determining things like that.