There has been a fair bit of good news in the last 48 hours. Here is some more. I logged onto Twitter just now and saw this tweet from my colleague Matt:

Starting this week with as many open jobs as we did before the pandemic https://t.co/5WacYVR2yn

It has taken almost nine months, but our USV portfolio companies have as many open and unfilled jobs this morning as they did prior to the pandemic. That is approximately 1,500 open positions.

That’s very good news. If you want one of them, go here and check out our job board.

NYC’s Summer Youth Employment Program is the nation’s largest youth employment program, historically connecting NYC’s neediest young adults (between the ages of 14 and 24) with a paid work experience every summer. The COVID-19 pandemic threw a wrench into it this summer and it was canceled. In response, the City and State and over 50 nonprofits have come together to design the Summer Bridge program for summer 2020. Summer Bridge will provide low-income NYC students with City and State-funded professional workplace experiences in the tech industry and beyond.

Summer Bridge will provide summer internships to 35,000 young adults this summer. Student interns will participate in workplace challenge projects for 10-20 total hours (2-4 hours per week for 4 weeks.) The program begins on August 3rd and finishes on August 28th. Summer Bridge and its non-profit partners will match student interns with companies, compensate students with a stipend ($700-1000 for the summer), and manage day-to-day-student relationships.

We want the NYC tech sector to be a big part of Summer Bridge this summer. Please consider having your company involved. Here is our ask of your company:

Design a “workplace challenge” for students based on a real business need or problem in one of four areas: product, engineering, marketing, or design. Tech: NYC is providing templates for these challenges.

Recruit employee volunteers to meet weekly with small groups (15-20 students) for hour-long virtual interactions. Ideally, each volunteer would see 2-3 groups a week.

Offer feedback to students at a virtual final workplace challenge presentation.

We hope your company will participate in Summer Bridge this summer. If you would like to participate, go here and sign up.

I am confident this pandemic will end. At some point, we will have a vaccine, therapeutics, and/or broad based immunity. When that will happen is less clear to me. I believe that at some point, we will be able to resume living and working as we did prior to the pandemic.

However, I am also confident that we will not resume living and working exactly as we did prior to the pandemic because some of the things we have adopted to get through this will reveal themselves as comparable or better than what we were doing before.

One of the places this is happening is knowledge work which is a growing percentage of the workforce in the US. What we have seen in this pandemic is that knowledge workers have been able to be comparably productive working from home and that has caused many large (and small) employers to consider different work/location options.

Yesterday, Twitter told their employees that most of them can work from anywhere going forward:

News: Twitter will allow its employees to work from home forever. @jack just emailed the company about it. Details here: https://t.co/KvvozuQ8Qn

I can imagine large and small banks, law firms, accounting firms, media and entertainment companies, and other knowledge based businesses making similar decisions.

I am not saying that remote work is ideal. There is something very valuable about being able to be in the same physical space as your colleagues. USV will likely keep an office for exactly that reason.

But it is also true that USV is operating incredibly well during this pandemic and we have not (yet) missed a beat.

What this means for large cities where many companies that engage in knowledge work are centered is an interesting question.

I saw this chart this morning on Benedict Evans’ Twitter:

People have been calling the end of SF for long time, but it’s worth remembering just how much the price delta has opened up in the last decade. For many people it no longer matters how driven you are if you can’t afford a second bedroom pic.twitter.com/4suajjd1gS

That compares two of the most expensive cities in the US (and world) to each other. And as bad as NYC is on the affordability index, SF is way worse.

So when you combine these two situations; large knowledge work hubs getting prohibitively expensive and remote work normalizing, it would seem that we are in for a correction.

What is less clear is where knowledge workers who can increasingly work from anywhere will choose to live (and work). Will cities remain attractive for the quality of life they offer (arts, culture, nightlife, etc)? Or will the suburbs stand to gain? Or will more idyllic locations like the mountains or the beach become the location of choice? Or will second and third tier cities become more attractive? I do not have a crystal ball on this question. I suspect it will be some of all of the above.

But this may become a big deal. Like the “white flight” that happened in the 50, 60s and 70s in a number of large cities in the US. Wholesale movement of large groups of people can have profound changes on regions.

Like many disruptions, this is both bad and good. Affordability (or lack thereof) and gentrification have been a blight on our cities. If we can reverse that trend, much good will come of it. This may also be helpful in addressing the climate crisis which remains the number one risk to planet Earth. So there are reasons to be excited about this. But wholesale abandonment is terrible. We should do whatever we can to avoid that.

It is early days for this conversation. But it is one we are going to have all around the US, and possibly all around the world. So it is time to start thinking about it.

The tech sector is the fastest growing sector of the economy in NYC and around the US and around the world. The tech sector offers high paying jobs and a growing number of them.

But, as we all know, the tech sector lacks the gender and racial diversity that would allow everyone to benefit from this growing sector of the economy. Most of the studies that have looked at the lack of diversity point to a skills gap standing in the way.

So last year Tech:NYC (where I am co-chair) and a few large employers (Google, Verizon, Bloomberg LP) and the Robin Hood Learning and Technology Fund commissioned a study of the skills training programs in NYC to see where there are gaps and what must be done to close them so that tech jobs are available to everyone in NYC who wants one.

What the report reveals is that NYC has a rich and expanding ecosystem of tech skills training opportunities, including K-12 and adult education. But, as we all know, the quality is uneven and so are the outcomes.

The report makes twelve recommendations which are detailed here. They are:

1. Make a significant new public investment in expanding and improving New York City’s tech education and training ecosystem.

2. Set clear and ambitious goals to greatly expand the pipeline of New Yorkers into technology careers.

3. Prioritize long-term investments in K–12 computing education.

4. Scale up tech training with a focus on programs that develop in-depth, career-ready skills.

5. Build the pipeline of educators and facilitators serving both K–12 and career readiness efforts.

6. Close the geographic gaps in tech education and skills-building programs.

7. New York City’s tech sector should play a larger role in developing, recruiting, and retaining diverse talent.

8. Increase access to tech apprenticeships and paid STEM internships through industry partnerships, CS4All, and the city’s current Summer Youth Employment Program.

9. Expand efforts to market STEM programs to underrepresented students and their families.

10. Develop and fund links from the numerous computer literacy and basic digital skills-building programs to the in-depth programs that can lead to employment.

11. Expand the number of bridge programs to provide crucial new on-ramps to further tech education and training for New Yorkers with fundamental skills needs.

12. Develop major new supports for the non-tuition costs of adult workforce training.

I participated on the advisory board of this study and support all of these recommendations. Elected officials and policy makers in NYC (and really everywhere) should read and heed these recommendations.

The tech sector faces many headwinds in society right now for a host of reasons. Not all of them can be solved by an employee base that mirrors the planet. But many of them can be and we need to work to get there.

I want to thank the Center For An Urban Future, Tech:NYC, Robin Hood Learning and Technology Fund, Google, Verizon, and Bloomberg LP for giving us a roadmap on how to get there.

It’s 2020. Time to look forward to the decade that is upon us.

One of my favorite quotes, attributed to Bill Gates, is that people overestimate what will happen in a year and underestimate what will happen in a decade.

This is an important decade for mankind. It is a decade in which we will need to find answers to questions that hang over us like last night’s celebrations.

I am an optimist and believe in society’s ability to find the will to face our challenges and the intelligence to find solutions to them.

So, I am starting out 2020 in an optimistic mood and here are some predictions for the decade that we are now in.

1/ The looming climate crisis will be to this century what the two world wars were to the previous one. It will require countries and institutions to re-allocate capital from other endeavors to fight against a warming planet. This is the decade we will begin to see this re-allocation of capital. We will see carbon taxed like the vice that it is in most countries around the world this decade, including in the US. We will see real estate values collapse in some of the most affected regions and we will see real estate values increase in regions that benefit from the warming climate. We will see massive capital investments made in protecting critical regions and infrastructure. We will see nuclear power make a resurgence around the world, particularly smaller reactors that are easier to build and safer to operate. We will see installed solar power worldwide go from ~650GW currently to over 20,000GW by the end of this decade. All of these things and many more will cause the capital markets to focus on and fund the climate issue to the detriment of many other sectors.

2/ Automation will continue to take costs out of operating many of the services and systems that we rely on to live and be productive. The fight for who should have access to this massive consumer surplus will define the politics of the 2020s. We will see capitalism come under increasing scrutiny and experiments to reallocate wealth and income more equitably will produce a new generation of world leaders who ride this wave to popularity.

3/ China will emerge as the world’s dominant global superpower leveraging its technical prowess and ability to adapt quickly to changing priorities (see #1). Conversely the US becomes increasingly internally focused and isolationist in its world view.

4/ Countries will create and promote digital/crypto versions of their fiat currencies, led by China who moves first and benefits the most from this move. The US will be hamstrung by regulatory restraints and will be slow to move, allowing other countries and regions to lead the crypto sector. Asian crypto exchanges, unchecked by cumbersome regulatory restraints in Europe and the US and leveraging decentralized finance technologies, will become the dominant capital markets for all types of financial instruments.

5/ A decentralized internet will emerge, led initially by decentralized infrastructure services like storage, bandwidth, compute, etc. The emergence of decentralized consumer applications will be slow to take hold and a killer decentralized consumer app will not emerge until the latter part of the decade.

6/ Plant based diets will dominate the world by the end of the decade. Eating meat will become a delicacy, much like eating caviar is today. Much of the world’s food production will move from farms to laboratories.

7/ The exploration and commercialization of space will be dominated by private companies as governments increasingly step back from these investments. The early years of this decade will produce a wave of hype and investment in the space business but returns will be slow to come and we will be in a trough of disillusionment on the space business as the decade comes to an end.

8/ Mass surveillance by governments and corporations will become normal and expected this decade and people will increasingly turn to new products and services to protect themselves from surveillance. The biggest consumer technology successes of this decade will be in the area of privacy.

9/ We will finally move on from the Baby Boomers dominating the conversation in the US and around the world and Millennials and Gen-Z will be running many institutions by the end of the decade. Age and experience will be less valued by shareholders, voters, and other stakeholders and vision and courage will be valued more.

10/ Continued advancements in genetics will produce massive wins this decade as cancer and other terminal illnesses become well understood and treatable. Fertility and reproduction will be profoundly changed. Genetics will also create new diseases and moral/ethical issues that will confound and confuse society. Balancing the gains and losses that come from genetics will be our greatest challenge in this decade.

That’s ten predictions, enough for now and enough for me. I hope I made you think as much as I made myself think writing this. That’s the goal. It is impossible to be right about all of this. But it is important to be thinking about it.

I know that comments here at AVC are broken at the moment and so I look forward to the conversation on email and Twitter and elsewhere.

I read last week that there are a growing number of regions around the country where there are labor shortages. Businesses literally cannot find the workers they need to operate their businesses.

Today is Labor Day, a day to celebrate the workers who built America and the labor movement that rose up to protect workers from abusive labor practices.

And so it is worth noting that we don’t have enough labor in our country right now. Some of this results from the strong economy which is ten+ years into an expansion. Some of this results from restrictive immigration policies.

But whatever the cause, we have an abundance of capital and a shortage of labor in the economy right now.

That makes it difficult to operate a business and even more difficult to expand. Automation can solve some of these issues and I expect we will see more automation in an environment where capital is available to fund investments in automation and labor is very tight.

But the other question is how much longer should we maintain a restrictive immigration policy. I believe we should have more legal immigration in the United States. We have labor shortages and many talented people who would like to come here and live and work.

It seems like a no brainer to me that we should expand legal immigration in the US right now.

Many people in startup land believe that the answer to the challenges around forcing departing employees to exercise vested options is to simply extend the option exercise period to the maximum (ten years) allowed by the IRS.

It certainly is one of the techniques that are available to companies and one that a number of our portfolio companies have adopted. Another option, and one that I prefer, is for a market to develop around financing these option exercises (and the taxes owed) when employees depart.

However, if you are thinking about extending the option exercise period for departing employees, you should understand that it will cost your company something.

Here is why:

Options are worth more than the spread between the strike price (the exercise price) and what the stock is actually worth. They have additional value related to the potential for the stock price to appreciate more over the life of the term of the option.

There is a formula that options traders (and companies that issue options) use to value options. It is called the Black-Scholes formula.

If you click on that link, you will quickly realize that the math used in the Black-Scholes formula can be complicated. But fortunately, there is a neat little web app that I frequently use to estimate the value of an option. It is here.

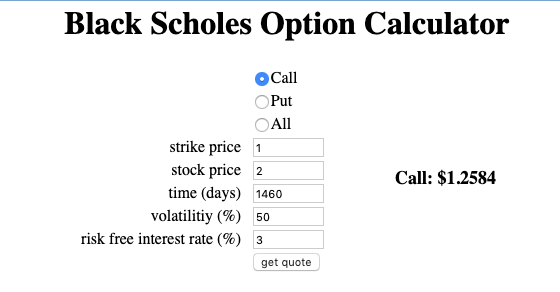

So let’s say that your company is issuing options at $1/share (your 409a) but your most recent financing was done at $2/share. Then a four year stock option is worth roughly $1.25/share.

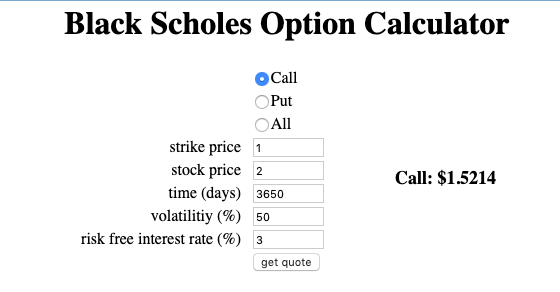

If, on the other hand, you offer a ten year option exercise period to your employees, the value of the option rises to $1.52/share, reflecting the longer period of time that the stock could appreciate over.

That is a 20% increase in the cost of issuing stock options. You could mitigate that by reducing the number of options you issue to incoming employees by 20% but that might make your equity comp offers less attractive to the “market” because incoming employees won’t value the longer exercise periods appropriately.

Stock based compensation costs are real costs even though many in startup land think of options as “free” because they don’t cost cash. The accounting profession has attempted to estimate these costs and companies do put stock based compensation costs on their income statements. If you go with ten year exercise periods instead of four year exercise periods, expect those expenses to go up significantly. Twenty percent is just the amount in my example. It could be larger, possibly as high as fifty percent (or more) if your exercise price is a lot closer to the current value of your stock.

This extra value of a ten year stock option versus a four year option is known as “overhang” by investors. It is the cost of carrying a group of people who have a call option on your stock but don’t have to pay for it for a long period of time. Generally speaking investors don’t like a lot of overhang in a stock.

All of that said, employees are the ones who create value for shareholders. They need to be compensated for that. And I am a fan of both cash compensation and stock based compensation. I like to see the employees of our portfolio companies well compensated in stock. That has a cost and everyone should be well aware of what it is. Longer exercise periods increase that cost. I would rather put more stock in the hands of the employees of our portfolio companies than give them longer exercise periods. But regardless of where one comes out on that tradeoff, it is important to recognize that it is a tradeoff. There are no free lunches, not even in stock option exercise periods.

Today, as is my custom on the first day of the new year, I am going to take a stab at what the year ahead will bring. I find it useful to think about what we are in for. It helps me invest and advise the companies we are invested in. Like our investing, I will get some of these right, and some wrong. But having a point of view, a foundation, is very helpful when operating in a world that is full of uncertainty.

I believe and have been telling those around me that I think 2019 will be a “doozy.” I think we will see major dislocations in the leadership of the United States, a bear market in stocks, a weakening economy, a number of issues with the global economy including a messy Brexit and a sluggish China. All of this will lead to a more cautious stance by investors in the startup economy. And crypto will not be a safe haven for any of this although there will be signs of life in crypto land in 2019.

Let’s take each of those in the order that I mentioned them.

I believe that we will have a different President of the United States by the end of 2019. The catalyst for this change will be a devastating report issued by Robert Mueller that outlines a history of illegal activities by our President going back decades, including in his campaign for President.

The House will react to Mueller’s report by voting to impeach the President. Which will set up a trial in the Senate. That trial will go so badly for the President that he will, like Nixon before him, negotiate a resignation that will lead to him and those close to him being pardoned for all actions, and Mike Pence will become the President of the United States sometime in 2019.

I believe this drama will play out through most of 2019. I expect the Mueller report to be issued sometime in the late winter/early spring and I expect an impeachment vote by the House before the summer, leading to a trial in the Senate in the second half of the year.

The drama in Washington will have serious impacts to the economy in the United States starting with our capital markets.

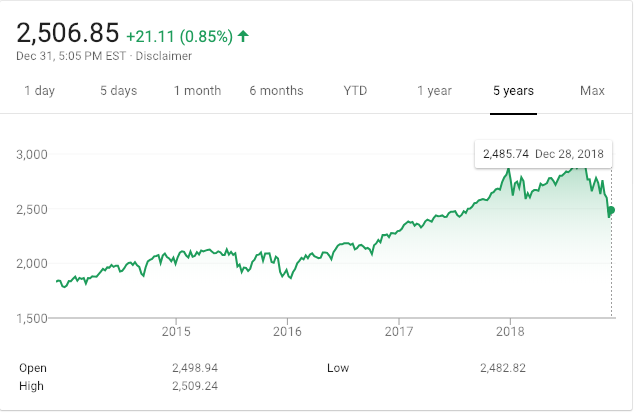

The US equity capital markets enter 2019 on shaky ground. Though the last week of the year brought us a relief rally, the markets are dealing with higher rates, some early indications of a weaker economy in 2019 (possibly due to higher rates), and, of course, the potential for the drama in Washington that we’ve already discussed. Here is a chart of the S&P 500 over the last five years:

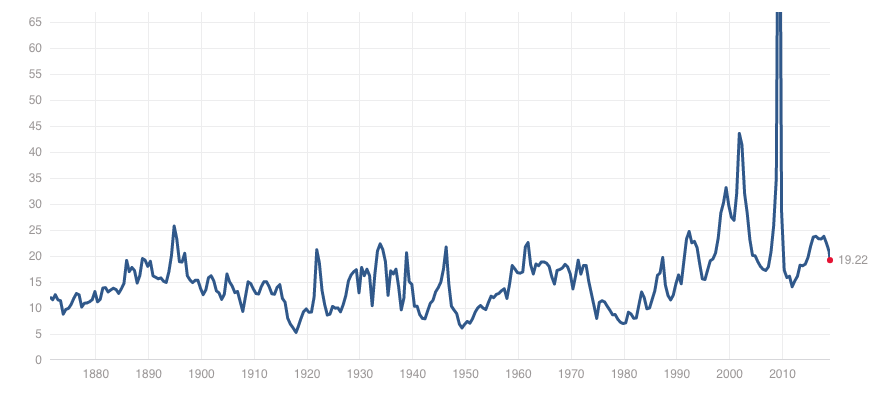

I expect the S&P 500 to visit 2,000 sometime in 2019 and then bounce around that bottom for much of the year. This would represent a decrease in the S&P’s trailing PE multiple to around 15x which feels like a bottom to me given the recent history of the equity markets in the US:

S&P PE Multiple (source http://www.multpl.com/)

Interest rates have been rising gradually in the US for the last three years. The Fed has taken its Fed Funds rate from essentially zero three years ago to almost 2.5% today:

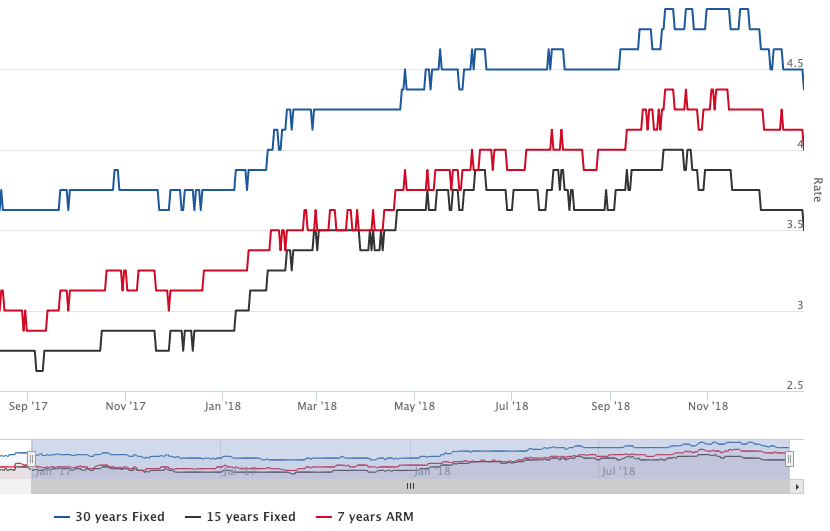

The rates that are available to consumers and businesses have followed and I expect that to continue in 2019. Here is a chart of the interest rates on the three most popular mortgage products in the US:

Source: https://www.amerisave.com/graphs/

When it gets more expensive to borrow, marginal projects don’t get funded. And what happens at the margin has a much larger impact on the economy than most people understand. No wonder the President wants to fire the Fed Chairman.

I expect the combination of higher rates, uncertainty in Washington, and storm clouds globally (which we will get to soon) will cause business leaders in the US to become more cautious on hiring and investment. Consumers will make essentially the same calculations. And that will lead to a weaker economy in the US in 2019.

The global picture is not much better. The eurozone is about to go through the most significant change in decades with some sort of departure of the UK from the EU (Brexit). It remains unclear exactly how this will happen, which in and of itself is creating a lot of uncertainty on the Continent. I don’t expect most businesses in Europe to do anything but play defense in 2019.

Probably the biggest unknown for the global economy is the resolution of the ongoing trade tensions between China and the US. It seems inevitable that China will make some concessions to the US to resolve these trade tensions. But, of course, what happens in Washington (first issue) may impact all of that. In the meantime, the uncertainty around trade and exports hangs over the Chinese economy. China’s GDP has been slowing in recent years as it achieved relative parity with the US and the Eurozone:

Source: https://tradingeconomics.com/china/gdp

Any significant trade concessions from China could impact its growth prospects in 2019 and beyond, which will take the most powerful engine of global growth off the table this year.

So all of that is a pessimistic take on the broader macro environment in 2019. How will all of this impact the startup/tech economy?

The startup/tech economy is somewhat immune to macro trends. Many startups and big tech companies were able to grow and expand their businesses during the last financial downturn in 2008 and 2009. Some very important tech companies were even started in those years.

The tech/startup economy is driven first and foremost by technical and creative (ie business model) innovation. And that is not impacted by the macro environment.

So I expect that we will continue to see big tech invest and grow their businesses and do well in 2019. I expect we will see IPOs from big names like Uber/Lyft/Slack, although I also expect those deals will get priced well below the lofty expectations they have in mind right now. Some of that will be because of weak equity markets in the US, but it is also true that most of the IPOs in 2018 also priced below the lofty “going in” expectations of founders, managers, boards, and their bankers. The public markets have been much more sanguine about value than the late stage private markets for a long time now.

However, I do think a difficult macro business and political environment in the US will lead investors to take a more cautious stance in 2019. It would not surprise me to see total venture capital investments in 2019 decline from 2018. And I think we will see financings take longer, diligence on new investments actually occur, and valuations to come under pressure for even the most attractive opportunities.

But all of that is going to happen at the margin. I expect 2019 to be another solid year for the tech/startup sector as we are in a possibly century-long conversion from an industrial economy to an information economy and the tailwinds for tech/startup vs the rest of the economy remain in place and strong.

Any set of predictions for 2019 from me on this blog would not be complete without some thoughts on crypto. So here is where my head is at on that topic.

I think we are in the process of finding the bottom on the large, liquid, and lasting crypto-tokens. But I think that process could take much of 2019 to play out. I expect we will see some bullish runs, followed by selling pressures taking us back to retest the lows. I think this bottoming out process will end sometime in 2019 and we will slowly enter a new bullish phase in crypto.

I think the catalyst for the next bullish phase will come as the result of some of the many promises made in 2017 coming to fruition in 2019. Specifically, I think we will see some big name projects ship, like the Filecoin project from our portfolio company Protocol Labs, and the Algorand project from our portfolio company Algorand. I think we will see a number of “next gen” smart contract platforms ship and challenge Ethereum for leadership in this super important area of the crypto sector. I also expect the Ethereum open source community to ship a number of important improvements to its system in 2019 and defend their leadership in the smart contract space.

Other areas of crypto where I expect to see meaningful progress and consumer adoption happen in 2019 are stablecoins, NFT/cryptoassets/cryptogaming, and earn/spending opportunities, particularly in the developing world.

There will also be pressure on the crypto sector in 2019. The area I am most concerned about are actions brought by misguided regulators who will take aim at high quality projects and harm them. And we will continue to see all sorts of failures, from scams, hacks, failed projects, and losing investments be a drag on the sector. But that is always the case with a new emerging technology that allows anyone to set up shop and get going. Permissionless innovation produces the greatest gains over time but also comes with the inevitable bad actors and actions.

So that’s where my head is at on 2019. Do I sound pessimistic? I suspect I do, but I am not. I am incredibly optimistic, like my partner Albert and can’t wait to get going and make things happen in this new year. It is going to be a doozy.

I heard about a cool program that helps NYC tech companies build more diverse teams. It is called Winternships.

The program is run by a group called WiTNY (Women in Tech and Entrepreneurship in NY) which is a three year-old collaboration between Cornell Tech and CUNY to drive more female students into tech majors or minors, and into the NYC tech ecosystem.

It works like this:

A Winternship is a paid, three-week internship experience during the January academic recess for freshman and sophomore women in tech. Participating companies design an ‘immersion’ experience in their business – students sit in on meetings, meet executives, go on site visits — and they work together on a challenge project that they pitch on the last day. WiTNY identifies students based on a match between your needs and their skills. Their team will even help you craft the Wintern experience if you want.

Here are some stats on the program:

Last January, 46 companies raised their hand and welcomed 177 CUNY women into their companies. Amazingly, 54% of these young women were able to parlay that experience into a paid summer tech internship somewhere in the city.

And here is the demographic of the CUNY student body:

CUNY is among the largest and most diverse universities in the country, with 250,000 undergrads and approximately 85% students of color.

If your team is trying to figure out how to diversify your internship and entry level hires, or just want to open your doors to transform the lives of young New Yorkers, considering hiring a Wintern team this January. And if you’re a small startup or a non-profit, WiTNY will even pay the student stipends for you.

Sounds great, right? If you want to host a Winternship at your company this January, you can get started here.

WorkMarket has been a big part of my personal portfolio for almost eight years.

USV and Spark seeded WorkMarket in June 2010, backing two serial entrepreneurs Jeff Leventhal and Jeff Wald.

The idea was to create a cloud based SAAS application to allow enterprises to manage their contingent workforces which were growing in size and complexity. It seemed like a timely opportunity at the time and it was. Eight years later the SAAS contingent workforce management market is in the hundreds of millions of dollars annually and WorkMarket is the creator and leader of it.

But like all startups, the WorkMarket story has a number of twists and turns. The market was a bit slower to develop than we had initially hoped and it wasn’t until the last few years that big companies started to include contingent workforce management in their SAAS budgets.

We also lost one of the two founders, Jeff Leventhal, when he stepped aside at the end of 2014 and was replaced as CEO by Stephen DeWitt who was recruited to the opportunity by Jordan Levy, who has been everything you could ask for in a co-investor.

The last few years at WorkMarket have been amazing. The senior team that Stephen and Jeff Wald built is among the best that I have had the opportunity to work with. And the contingent workforce market really exploded in 2016 and 2017.

But like all exploding markets, the expanding opportunity brought a lot of new entrants and buyers interested in getting into it. And one of those big companies, ADP, made us an offer we could not refuse, both in terms of the financial opportunity and the fit with their business. ADP has been helping enterprises, large and small, with human capital management solutions for decades and has the customer base, market knowledge, and capital to lean into this opportunity in a way that a venture backed startup never could.

So WorkMarket is now part of ADP and I am pleased with that outcome. Jeff Wald will take over leading WorkMarket for its next phase and he is well suited and deserving of that role. He has been the one constant for the eight years that I have worked on WorkMarket. Everyone else who was there at the start has come and gone. But Jeff and I saw it through from start to finish and I appreciate that very much.

I also want to acknowledge Stephen and the senior team of Grady Leno, Jim Chou, Marcy Shinder, and Tom Benton. As I said, this is an amazing team and it has been a pleasure to watch them build the product, market, and customer base. They are all superstars in my book.

This is the way of the VC business. You get inspired by an idea and a couple founders. You spend a lot of time helping them build something. You give a piece of yourself to the business. And one day, you are done. That day, for me and WorkMarket, is today and I have enjoyed the ride very much.