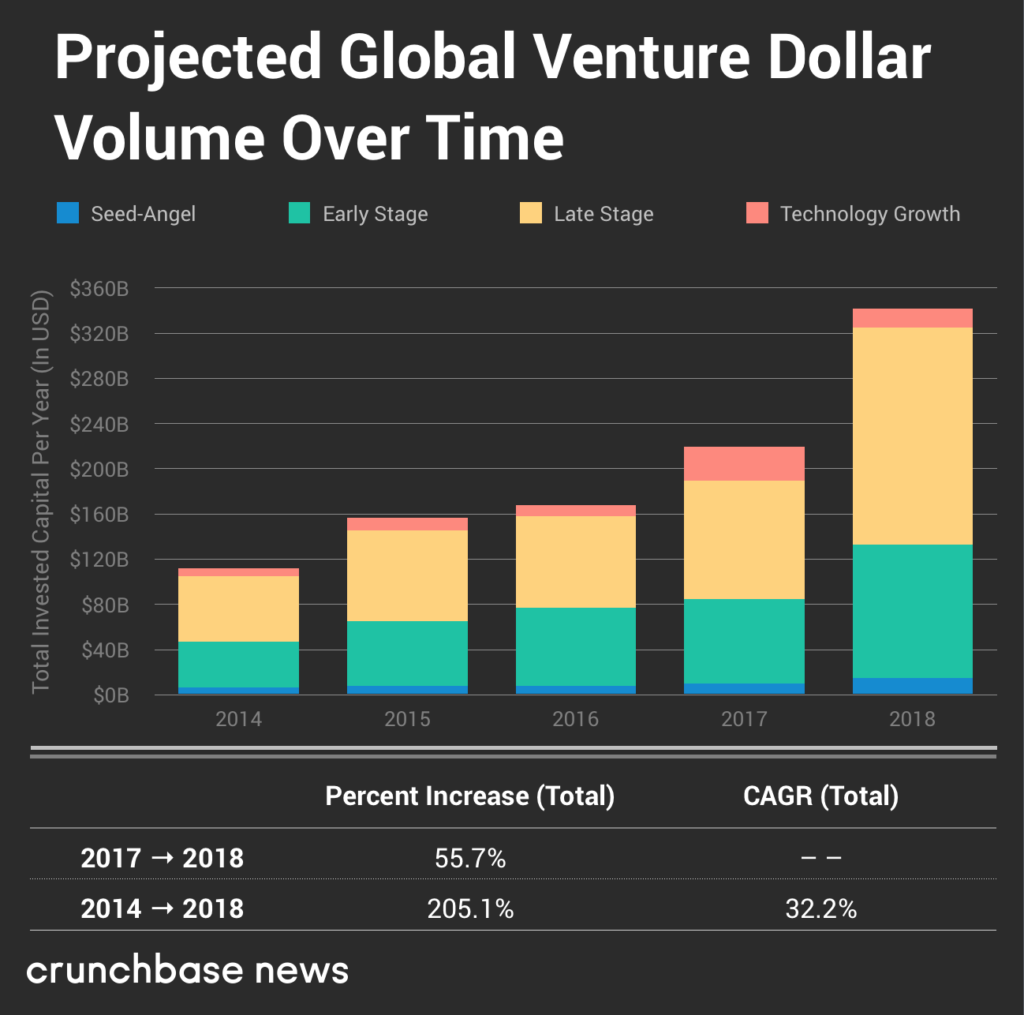

The Crunchbase numbers are much bigger, they report about $330bn of global deal volume.

But otherwise the trends are roughly the same. Flattening deal volumes and amounts raised in the early stage market with massive expansion in the late stage market.

Make no bones about it, there is a lot of money in the venture capital ecosystem right now.

In the wake of Erin Griffith’s piece in the NY Times suggesting that venture capital is toxic for some entrepreneurs, there has been a fair bit of debate about the causes of that situation.

One thing that I think gets lost in the VC vs. non-VC discussion is that VCs don't need a company to become a "unicorn." At least not the early-stage VCs. They might want it, but unicorns weren't really a thing until a few years back, and VCs "settled" for much shorter home runs

I think the truth is somewhere in between. Ownership levels have been coming down in VC over the last thirty years. When I got into VC in the mid 80s it was very typical for a VC to want 25% of the company. Then it became 20%. Then 15%. Now we ask ourselves if we can get to 10%

It is tempting to look at what is going on in the startup/tech landscape and say that the growing amount of capital under management is the problem.

But the capital market for startups is a complex system and I don’t think it is as simple as that.

It may well be that as entrepreneurs have had more negotiating leverage over the last twenty+ years, they have pushed valuations up significantly and the capital markets (ie VCs) have reacted to that by accumulating more capital so that they can try to buy the same amount of ownership at the higher prices.

That hasn’t really worked and the VC industry typically owns a lot less of a company at exit and the founders and team own a lot more versus 25 years ago. We have seen that clearly in our own portfolios over the last fifteen years and I would assume that is true across the industry.

So while it is tempting to suggest that big bad VCs are the reason for all the problems in the startup sector, I would caution everyone from coming to that conclusion. Like all relationships, it takes two to tango, and both sides have had something to do with where we are right now.

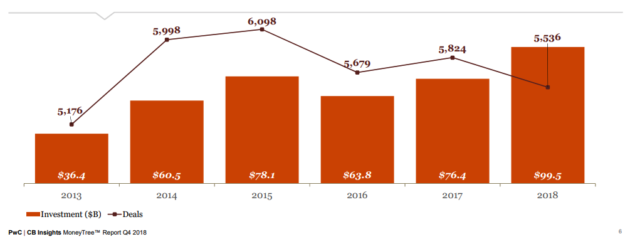

2018 saw the venture capital business moving to larger and larger deals. There were roughly 200 deals around the globe in 2018 where $100mm or more was raised.

And yet the number of total transactions declined slightly from 2017.

This trend is much more obvious if you look at the six years from 2013 to 2018. Total deal activity has increased less than 10% while total capital investment has almost tripled.

These trends are unsustainable. It is certainly attractive to de-risk by moving upstream to invest in more mature companies, larger rounds, etc. But if we don’t reseed our fields there won’t be as many of those mature companies in the future.

And that is why USV remains a small fund/firm which allows us to invest in Seed, Srs A, and Srs B rounds. It may not be fashionable to do that right now, but I am certain that it is and will continue to be profitable.

The Gotham Gal and I went through our (actually her) angel investments yesterday and figured out which ones went under in 2018 so we could take the tax write-offs on our 2018 returns.

It is an odd exercise. Kind of like reading the obituaries.

But it is an important exercise for several reasons.

First, taking the write-offs against the gains shelters the gains so they can be re-invested in full. Over her first six years of investing (2007-2012), she has realized a bit more than she invested and the losses have sheltered the gains so all of that capital can be reinvested. And the investments that remain unrealized from that cohort are all solid now and will likely produce another 2-3x on invested capital.

But it also a nice “post mortem” process to go through the ones that didn’t work and think a bit about what went wrong. We don’t obsess about the losses, but taking some time to run through them is helpful.

Sometimes failed investments turn into the “living dead” in which you end up a tiny investor in another company by virtue of an acqui-hire, a distressed sale, or some other such transaction. It is generally a smart idea to sell your stock back to the company or another shareholder or abandon your interest and take the loss on those kinds of investments. The tax loss is often worth more than the stock you own. A regular process of going through the losses will surface opportunities like that too.

The bottom line is that angel investing is risky business. Super early stage investing, like the kind the Gotham Gal does (she is most often the first check into the company), will produce loss ratios of 50% or higher. The winners eventually bail you out and super early stage investing ought to produce 3x on capital or better (or you shouldn’t be doing it). One nice advantage of this model is the losses come early and the wins come much later. Taking your losses, getting the write-offs, and sheltering your gains is an important part of the model and it is best to have a regular process to make sure you are taking the losses when you can.

Today, as is my custom on the first day of the new year, I am going to take a stab at what the year ahead will bring. I find it useful to think about what we are in for. It helps me invest and advise the companies we are invested in. Like our investing, I will get some of these right, and some wrong. But having a point of view, a foundation, is very helpful when operating in a world that is full of uncertainty.

I believe and have been telling those around me that I think 2019 will be a “doozy.” I think we will see major dislocations in the leadership of the United States, a bear market in stocks, a weakening economy, a number of issues with the global economy including a messy Brexit and a sluggish China. All of this will lead to a more cautious stance by investors in the startup economy. And crypto will not be a safe haven for any of this although there will be signs of life in crypto land in 2019.

Let’s take each of those in the order that I mentioned them.

I believe that we will have a different President of the United States by the end of 2019. The catalyst for this change will be a devastating report issued by Robert Mueller that outlines a history of illegal activities by our President going back decades, including in his campaign for President.

The House will react to Mueller’s report by voting to impeach the President. Which will set up a trial in the Senate. That trial will go so badly for the President that he will, like Nixon before him, negotiate a resignation that will lead to him and those close to him being pardoned for all actions, and Mike Pence will become the President of the United States sometime in 2019.

I believe this drama will play out through most of 2019. I expect the Mueller report to be issued sometime in the late winter/early spring and I expect an impeachment vote by the House before the summer, leading to a trial in the Senate in the second half of the year.

The drama in Washington will have serious impacts to the economy in the United States starting with our capital markets.

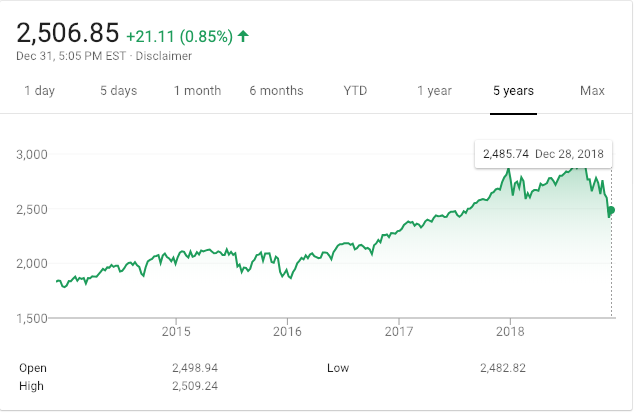

The US equity capital markets enter 2019 on shaky ground. Though the last week of the year brought us a relief rally, the markets are dealing with higher rates, some early indications of a weaker economy in 2019 (possibly due to higher rates), and, of course, the potential for the drama in Washington that we’ve already discussed. Here is a chart of the S&P 500 over the last five years:

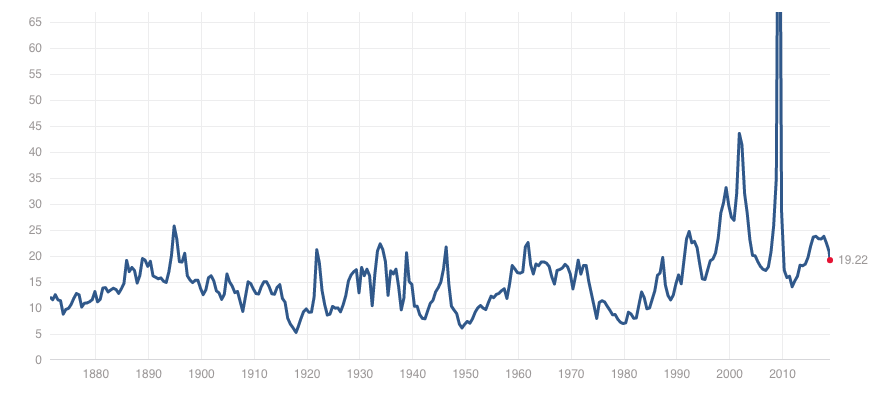

I expect the S&P 500 to visit 2,000 sometime in 2019 and then bounce around that bottom for much of the year. This would represent a decrease in the S&P’s trailing PE multiple to around 15x which feels like a bottom to me given the recent history of the equity markets in the US:

S&P PE Multiple (source http://www.multpl.com/)

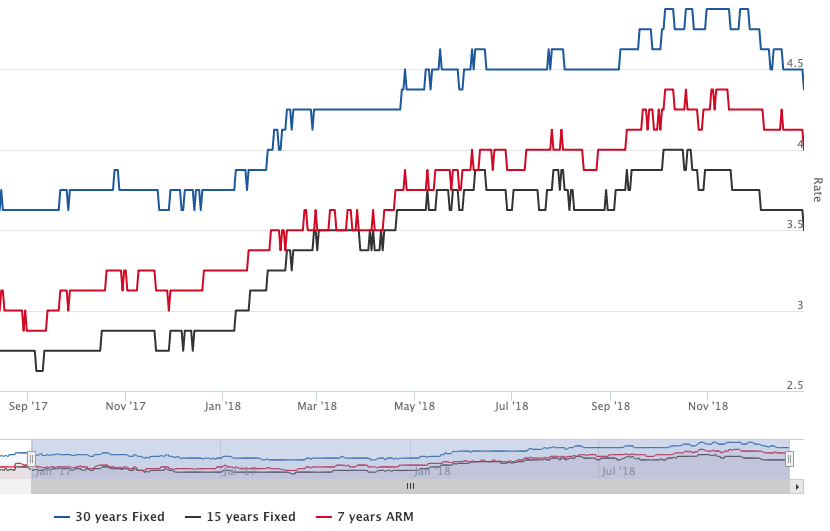

Interest rates have been rising gradually in the US for the last three years. The Fed has taken its Fed Funds rate from essentially zero three years ago to almost 2.5% today:

The rates that are available to consumers and businesses have followed and I expect that to continue in 2019. Here is a chart of the interest rates on the three most popular mortgage products in the US:

Source: https://www.amerisave.com/graphs/

When it gets more expensive to borrow, marginal projects don’t get funded. And what happens at the margin has a much larger impact on the economy than most people understand. No wonder the President wants to fire the Fed Chairman.

I expect the combination of higher rates, uncertainty in Washington, and storm clouds globally (which we will get to soon) will cause business leaders in the US to become more cautious on hiring and investment. Consumers will make essentially the same calculations. And that will lead to a weaker economy in the US in 2019.

The global picture is not much better. The eurozone is about to go through the most significant change in decades with some sort of departure of the UK from the EU (Brexit). It remains unclear exactly how this will happen, which in and of itself is creating a lot of uncertainty on the Continent. I don’t expect most businesses in Europe to do anything but play defense in 2019.

Probably the biggest unknown for the global economy is the resolution of the ongoing trade tensions between China and the US. It seems inevitable that China will make some concessions to the US to resolve these trade tensions. But, of course, what happens in Washington (first issue) may impact all of that. In the meantime, the uncertainty around trade and exports hangs over the Chinese economy. China’s GDP has been slowing in recent years as it achieved relative parity with the US and the Eurozone:

Source: https://tradingeconomics.com/china/gdp

Any significant trade concessions from China could impact its growth prospects in 2019 and beyond, which will take the most powerful engine of global growth off the table this year.

So all of that is a pessimistic take on the broader macro environment in 2019. How will all of this impact the startup/tech economy?

The startup/tech economy is somewhat immune to macro trends. Many startups and big tech companies were able to grow and expand their businesses during the last financial downturn in 2008 and 2009. Some very important tech companies were even started in those years.

The tech/startup economy is driven first and foremost by technical and creative (ie business model) innovation. And that is not impacted by the macro environment.

So I expect that we will continue to see big tech invest and grow their businesses and do well in 2019. I expect we will see IPOs from big names like Uber/Lyft/Slack, although I also expect those deals will get priced well below the lofty expectations they have in mind right now. Some of that will be because of weak equity markets in the US, but it is also true that most of the IPOs in 2018 also priced below the lofty “going in” expectations of founders, managers, boards, and their bankers. The public markets have been much more sanguine about value than the late stage private markets for a long time now.

However, I do think a difficult macro business and political environment in the US will lead investors to take a more cautious stance in 2019. It would not surprise me to see total venture capital investments in 2019 decline from 2018. And I think we will see financings take longer, diligence on new investments actually occur, and valuations to come under pressure for even the most attractive opportunities.

But all of that is going to happen at the margin. I expect 2019 to be another solid year for the tech/startup sector as we are in a possibly century-long conversion from an industrial economy to an information economy and the tailwinds for tech/startup vs the rest of the economy remain in place and strong.

Any set of predictions for 2019 from me on this blog would not be complete without some thoughts on crypto. So here is where my head is at on that topic.

I think we are in the process of finding the bottom on the large, liquid, and lasting crypto-tokens. But I think that process could take much of 2019 to play out. I expect we will see some bullish runs, followed by selling pressures taking us back to retest the lows. I think this bottoming out process will end sometime in 2019 and we will slowly enter a new bullish phase in crypto.

I think the catalyst for the next bullish phase will come as the result of some of the many promises made in 2017 coming to fruition in 2019. Specifically, I think we will see some big name projects ship, like the Filecoin project from our portfolio company Protocol Labs, and the Algorand project from our portfolio company Algorand. I think we will see a number of “next gen” smart contract platforms ship and challenge Ethereum for leadership in this super important area of the crypto sector. I also expect the Ethereum open source community to ship a number of important improvements to its system in 2019 and defend their leadership in the smart contract space.

Other areas of crypto where I expect to see meaningful progress and consumer adoption happen in 2019 are stablecoins, NFT/cryptoassets/cryptogaming, and earn/spending opportunities, particularly in the developing world.

There will also be pressure on the crypto sector in 2019. The area I am most concerned about are actions brought by misguided regulators who will take aim at high quality projects and harm them. And we will continue to see all sorts of failures, from scams, hacks, failed projects, and losing investments be a drag on the sector. But that is always the case with a new emerging technology that allows anyone to set up shop and get going. Permissionless innovation produces the greatest gains over time but also comes with the inevitable bad actors and actions.

So that’s where my head is at on 2019. Do I sound pessimistic? I suspect I do, but I am not. I am incredibly optimistic, like my partner Albert and can’t wait to get going and make things happen in this new year. It is going to be a doozy.

We made the classic mistake that all investors make. We focused too much on what they were doing at the time and not enough on what they could do, would do, and did do.

I used to try explaining that $20 stock certificates were an entry point into something bigger. It never worked.

Same issue. Most investors looked at the business of selling $20 electronically issued stock certificates and missed that it was simply the entry point to moving the entire private securities market to the cloud.

Investors have figured that out now and Carta is one of the fastest growing SAAS companies out there.

But missing the forest through the trees is a common mistake that early stage investors make. I make it. We make it. Everyone makes it.

My partner Brad Burnham has the best framework for thinking about this issue that I know of. He calls it “finding the narrow point of the wedge.” The analogy is trying to hammer a piece of metal into a block of wood. If the metal is large and flat, you can’t do it. But if it is narrow and thin, you can. And, of course, once you get the narrow point of the wedge into the block of wood, you can hammer it all the way in.

So, that’s what we all have to think about. Is there a large market out there that can be fundamentally changed with technology (like moving the private securities market to the cloud, or turning empty real estate into places to stay when you travel)? And what is the simplest and easiest way to get into it (like selling $20 electronic stock certs or putting air mattresses on living room floors)?

We try to keep Brad’s framework in our heads at USV, but we forget it frequently. And it is often the costliest mistake we make in the VC business. Because high impact companies do not come along that often, and when they do, we have to find a way to say yes.

I had an interesting conversation with a friend who operates a traditional business (not tech, not venture backed, not “growth”) last week. He buys a lot of software from tech companies and he observed that not one of them operates profitably. And that makes him a bit uncomfortable as he has always operated his businesses profitably. He mentioned to me that when he has taken capital from investors he has paid them back in full in less than a year each time, from the profits that the business is generating.

It got me thinking that there is something about tech, particularly venture capital-backed tech, that allows us to operate for what seems like forever without a need to generate self sustaining profits.

This can be a fantastic way to generate value when the opportunity is large enough (Google, Amazon, Facebook, Twitter, etc). But it is not a fantastic way to generate value when the opportunity is constrained, either by a smallish market size (TAM) or by a ton of competitors (little to no barriers to entry) or a number of other factors.

Value is generated when the capital required to get a business to sustainability (usually positive cash flow, but I will include exits here) is meaningfully less than what the business is worth when sustainability is reached.

As the capital requirements go up, because of sustained losses year after year after year, the business needs to become worth ever more money at sustainability.

The mistake I think we make in the startup/tech/VC sector is that we look at things like Google/Amazon/Facebook/Twitter, or more recently Uber/Airbnb/Slack, and we think that every business can execute the same playbook. The sad truth is that not every business can execute that playbook and, as a result, many startups consume way too much capital on the way to sustainability and value is lost, not created.

The never ending question that founders and management teams and boards face is whether to invest for growth (aka lose a ton of money) or work towards profitability (but constrain the growth of the business). It seems like every board I am on and every company in our portfolio is always asking this question.

Where I come out on this issue, and always have, is that the growth has to be responsible (positive unit economics on growth spend) and that the path to profitability needs to be well in sight. I would add to those two constraints that a management team ought to be able to get a business profitable in a pinch without killing the business, if necessary. Clearly these “rules” should not apply to very early stage companies. They become relevant and possible once a business has a growing customer base and revenue stream.

I think very few companies in our portfolio and any VC firm’s portfolio will pass these tests right now. Some do but not many. We have a few companies in our portfolio that are operating profitably. We have a few more that are in operating with profitability well in sight and could get there in a pinch without hurting the business too much. But the vast majority are burning money like its water and there is plenty more where it came from.

Perhaps it is true that there will always be money to fund burn. Or perhaps it isn’t. But even if there is endless capital, many founders and teams will wake up one day and realize that all of that burn they accumulated is now a hurdle they have to overcome. And many won’t overcome it.

The profit motive is what makes capitalism work. Businesses are ultimately valued as a discounted set of future cash flows. Positive cash flows. If you can’t generate profits in the future, your business will not be worth anything. So profits are key. And yet we don’t seem to value them in the tech/VC/startup world very much. Maybe we should.

I believe that negotiating is more of an art than a science. There are certainly strategies and skills that one can develop that make for better outcomes.

But the art comes into play in figuring out what the person or people on the other side are optimizing for and adopting a strategy that reflects that.

I have found that a single style and strategy rarely works well for every situation.

Let’s take the important question of whether you should make a “take it or leave it” offer and then draw a hard line on that offer or whether you should make an offer that has a fair bit of negotiating cushion in it.

Some people like to negotiate and expect to negotiate. If you make a hard line offer and refuse to negotiate with them, they will be frustrated with you and may seek out other offers. Or if they do end up transacting with you, they will feel burned by the negotiating process and you will be starting off the relationship on the wrong foot

If you make an offer that has a lot of room for negotiating, they may actually enjoy the experience and come away feeling like they got a good deal from you.

I like to shake hands at the end of a negotiation with both parties pleased with where they ended up. That is particularly important when you are entering a long term relationship like a venture capital investment.

It is also critical to know what your “must haves” are going into a negotiation and what you can give on.

Another form of negotiating art is how you reveal your must haves and where you are flexible. I have found that it is not helpful to a negotiation to lay all of that out at the start. There is a lot of value in a discovery process. It is a bit like dating. Each side reveals a bit about themselves to the other and that is also very helpful at the start of what might be a long relationship.

All that said, there are times when drawing a hard line is appropriate. If the other side has all of the leverage then it is often best to make your best offer and say take it or leave it. If, for example, the other side has used a process to drive price discovery and possibly discovery around other key terms and has multiple offers, you are not going to win the deal with the low ball offer with negotiating room. You have to give it your best shot and then walk if you can’t win on that basis.

Like most art, it takes some time to learn all of this. You can take a class or a workshop on negotiating tactics and learn the fundamentals. I would strongly recommend that for young folks just getting started in business.

But when it comes to learning how to size up the other party, well that takes time. You have to mess up some negotiations, lose some deals, and possibly win some on terms you later regret.

It is that last bit, living with the terms you negotiate, where the greatest learnings come. I have found that a very powerful argument in a difficult negotiation is when you say “I did that once, I deeply regret it, and I’m never doing it again.”